Imagine you are standing in a casino with your life savings in your pocket. A man in a suit approaches you and says, “I can give you a way to win more often, but here’s the catch: it also makes it much harder for you to lose everything.”

In the world of gambling, that’s a scam. But in the world of professional finance, it’s a mathematical reality.

Most people jump into the stock market like they’re throwing darts at a board—blindfolded. They buy a “hot stock” because a friend mentioned it, or they panic-sell when the news turns red. If you want to build a “Money Cornucopia” that lasts for decades, you don’t need luck. You need the Architecture of Wealth. This begins with the only “Free Lunch” in the financial world: Asset Allocation and Diversification.

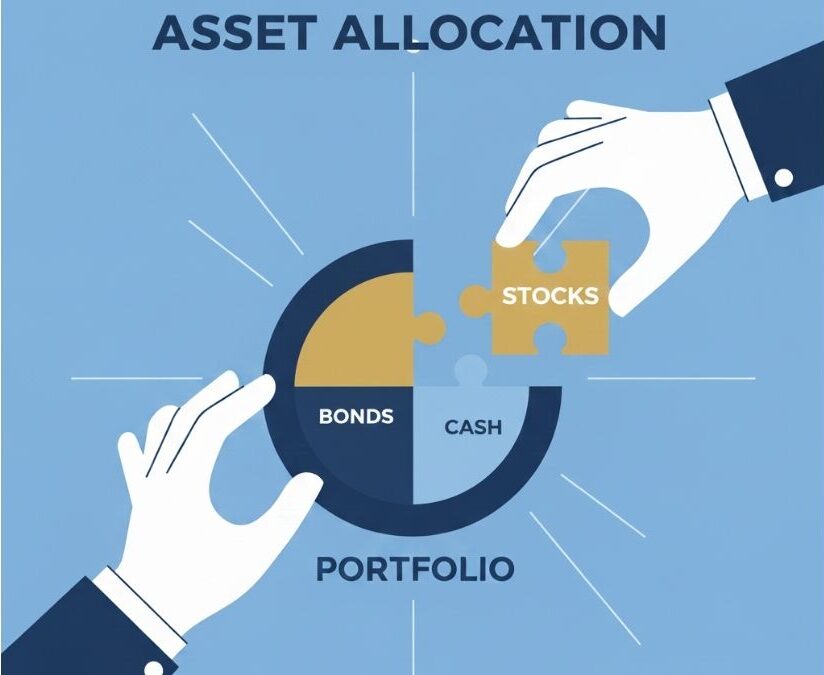

The Blueprint: What is Asset Allocation?

Before you pick a single stock or buy a single bond, you have to decide on the Blueprint. Asset Allocation is the high-level decision of how you divide your “Investment Pie.” It isn’t about which specific company you buy; it’s about what category of assets you own. Think of your portfolio like a sports team:

- Stocks (Equities) are your Offense: They go out and score points (growth). They are fast and exciting, but they can leave you vulnerable if the market turns aggressive.

- Bonds (Fixed Income) are your Defense: They aren’t there to score; they are there to protect your lead. They provide steady, smaller returns to keep the game stable when things get rough.

- Cash is your Bench: It’s ready to play when you need a timeout or when a sudden “sale” happens in the market.

The Golden Rule: Studies show that your Asset Allocation—how much “Offense” vs. how much “Defense” you have—determines over 90% of your long-term investment results. It is the most important decision you will ever make as an investor.

Diversification: The “Eggs in a Basket” Strategy

If Asset Allocation is choosing the right baskets (Stocks, Bonds, Real Estate), then Diversification is making sure you don’t put all your eggs in just one of them.

Imagine you invest all your “Offense” money into a single technology company. If that company succeeds, you’re a hero. But if that specific company goes bankrupt or faces a scandal, your entire “Offense” is wiped out.

Diversification solves this by spreading your money across hundreds of different companies, industries, and even countries.

- By Sector: Don’t just own Tech; own Healthcare, Energy, and Consumer Goods.

- By Geography: Don’t just own U.S. companies; own pieces of the economy in Europe, Asia, and Emerging Markets.

When you are diversified, you stop cheering for a single “player” to win the game. Instead, you are cheering for the entire world economy to grow over time. Even if one company fails, the other 499 in your portfolio keep moving forward.

The Spectrum of Risk vs. Reward

In the world of investing, there is a fundamental law: To get higher returns, you must be willing to accept higher risk.

Understanding where you sit on this spectrum is the secret to staying invested when things get “scary.” If you take on too much risk, you’ll panic-sell during a market dip. If you take on too little, your money won’t grow fast enough to beat Inflation.

| Asset Type | Potential Reward | Risk Level | The “Vibe” |

| Stocks | High | High | The Rollercoaster: Thrilling but bumpy. |

| Bonds | Moderate | Low | The Escalator: Slow, steady, and predictable. |

| Cash/Savings | Very Low | Minimal | The Couch: Very safe, but doesn’t go anywhere. |

To keep this post SEO-friendly, we will use clear subheadings (H2 and H3 tags), bold key terms, and focus on the “Search Intent” of someone looking for a strategy they can actually use.

Here is the next section on balancing Risk vs. Reward.

How to Find Your Perfect Balance

Your “ideal” Asset Allocation isn’t a random guess. It is usually determined by two things: Your Time Horizon and Your Risk Tolerance.

1. Your Time Horizon

How soon do you need the money?

- Long Term (10+ years): You can afford to have more “Offense” (Stocks) because you have time to wait out the market’s bad days.

- Short Term (1-3 years): You need more “defense” (bonds/cash) because you can’t afford a market dip right before you need to spend the money.

For those with a long-term horizon, the goal is to harness Compound Interest. By choosing a higher stock allocation, you give your ‘money tree’ more room to grow over decades.

2. Your Risk Tolerance

This is a “gut check.” How would you feel if you opened your account tomorrow and saw it was down 20%?

- If you would be calm and see it as a “sale” to buy more, you have a High Risk Tolerance.

- If you would lose sleep or want to sell everything, you have a Low Risk Tolerance.

The Rebalancing Act: Keeping the Blueprint Intact

Over time, your “Investment Pie” will change on its own. If stocks have a great year, they might grow from 60% of your portfolio to 80%. This makes your portfolio riskier than you intended.

Rebalancing is the process of selling a bit of what has grown too large and buying more of what has lagged behind. This forces you into the most successful habit in investing: Buying Low and Selling High.

Overview: The Architecture Summary

- Asset Allocation is your big-picture blueprint (e.g., 70% Stocks, 30% Bonds).

- Diversification is spreading the risk within those categories (not just one stock, but hundreds).

- Risk vs. Reward is the balance you choose based on your goals and your “gut.”

- Rebalancing is how you maintain your blueprint over time.

Frequently Asked Questions (FAQs)

Is diversification just for rich people?

Not anymore. Thanks to “Index Funds” and “ETFs,” you can own a diversified piece of the entire global economy with as little as $1.

What is the “standard” asset allocation?

A classic starting point for many is the “60/40 Portfolio” (60% Stocks, 40% Bonds). However, younger investors often lean toward 80% or 90% stocks for more growth.

Does diversification guarantee I won’t lose money?

No. Diversification protects you from the failure of a single company, but it cannot protect you from a general market decline. However, it ensures that when the market recovers, you are still in the game.

How does Asset Allocation fit with the Time Value of Money (TVM)?

Asset allocation ensures that your ‘future dollars’ have the best chance of outgrowing your ‘today dollars’ by balancing risk and return.”

Conclusion: Your Financial Fortress

By mastering Asset Allocation and Diversification, you have moved from “guessing” to “architecting.” You are no longer betting on a single horse; you are betting on the track itself. You have built a fortress that can withstand market storms while still capturing the growth of the global economy.

Now that you have your blueprint, it’s time to look at the actual tools we use to build it.

Leave a Reply