Asset allocation is the strategy of dividing your investment portfolio across different asset categories like stocks, bonds, and cash. Diversification is spreading your money within those categories across many different companies, industries, and countries. Together, they form the foundation of how experienced investors manage risk and grow wealth over time.

If that already makes sense, you are ahead of most people.

Most beginners jump into investing by buying a single stock because a friend mentioned it or because they saw it trending on social media. When that one stock drops, they panic, sell at a loss, and decide that investing “doesn’t work.”

The problem was never investing itself. The problem was putting everything into one place without a plan. Asset allocation and diversification are the plan. They are not complicated, they do not require a finance degree, and they work whether you are investing $100 or $100,000.

This guide explains both concepts in plain language, shows how they are different, how they work together, and how you can start using them even if you are a complete beginner.

Table of Contents

What Is Asset Allocation?

Asset allocation is the big picture decision of how you divide your money across different types of investments.

Before you pick a single stock or buy a single bond, you need to decide on the overall structure. How much of your money goes into stocks? How much into bonds? How much stays in cash? That decision is your asset allocation.

Think of it like building a meal. Before you choose specific ingredients, you decide the overall balance: how much protein, how many vegetables, how many carbs. The specific ingredients come later. The balance comes first.

The three main asset categories are:

| Asset category | Role in your portfolio | What to know |

|---|---|---|

| Stocks | Growth engine | Highest potential return over long periods but most volatile. Can rise 20% or drop 30% in a single year. Historically averaged roughly 7% annual growth over 10 to 20-year periods |

| Bonds | Stability layer | Smaller, steadier returns that hold value better when stocks drop. The part of your portfolio that lets you sleep at night during market turbulence |

| Cash and equivalents | Safety net | Emergency funds and short-term savings you may need within 1 to 2 years. Does not grow meaningfully but does not disappear either |

The split you choose between these three categories determines the overall risk and reward profile of your portfolio. This decision alone accounts for the vast majority of your long-term investment results, which is why financial professionals consider it the single most important choice an investor makes.

If you want to understand why that balance matters, I wrote a detailed breakdown in what is the risk return tradeoff that explains how risk and reward are connected.

What Is Diversification?

Diversification is spreading your money within each category so that no single investment can wipe you out.

If asset allocation is deciding how much of your money goes into stocks versus bonds versus cash, diversification is what happens inside each of those buckets.

For example, say you decide that 70% of your money should go into stocks. Diversification means you do not put all of that 70% into a single company. Instead, you spread it across many companies, many industries, and many countries.

Here is why that matters. Imagine putting all your stock money into one technology company. If that company has a great year, you do well. But if that company faces a scandal, a lawsuit, or simply makes a bad product decision, your entire stock portfolio is damaged.

Now imagine spreading that same money across 500 different companies in technology, healthcare, energy, finance, and consumer goods, across the United States, Europe, and Asia. If one company fails, the other 499 keep going. Your portfolio absorbs the loss and keeps growing.

Diversification works across several dimensions:

| Dimension | What it means in practice |

|---|---|

| By sector | Do not only own technology stocks. Spread across healthcare, energy, consumer goods, financials, and other industries so one sector’s decline does not drag your whole portfolio |

| By geography | Do not only own companies in one country. Own pieces of the economy across the United States, Europe, Asia, and other regions to reduce country-specific risk |

| By company size | Own a mix of large established companies for stability and smaller growing ones for higher potential upside over time |

| By asset type | Diversify even within bonds by mixing government bonds with corporate bonds of different terms and credit ratings to reduce interest rate and default risk |

The SEC describes diversification as the practice of spreading money among different investments to reduce risk. It is one of the oldest and most widely supported principles in finance.

Asset Allocation vs Diversification: What Is the Difference?

Asset allocation is choosing the baskets. Diversification is spreading the eggs within each basket.

This distinction confuses many beginners because the two concepts work together so closely that they can seem like the same thing. They are not.

Here is the simplest way to think about the difference:

| Concept | What it decides | Example |

|---|---|---|

| Asset allocation | How much goes into each asset category | 70% stocks, 25% bonds, 5% cash |

| Diversification | How you spread within each category | Those 70% stocks split across 500 companies in 10 sectors across 20 countries |

Asset allocation is the strategic, top-level decision. It sets the overall risk and return profile of your portfolio. It answers the question “how much risk am I comfortable with?”

Diversification is the tactical, ground-level execution. It reduces the impact of any single investment failing. It answers the question “what if one of my investments goes wrong?”

You need both. Asset allocation without diversification means you have the right balance of stocks and bonds, but you might have all your stock money in one company. Diversification without proper asset allocation means you own many different investments, but you might have 95% of your money in stocks, which is too risky for most people.

Together, they create a portfolio that is both balanced at the top level and protected at the individual investment level.

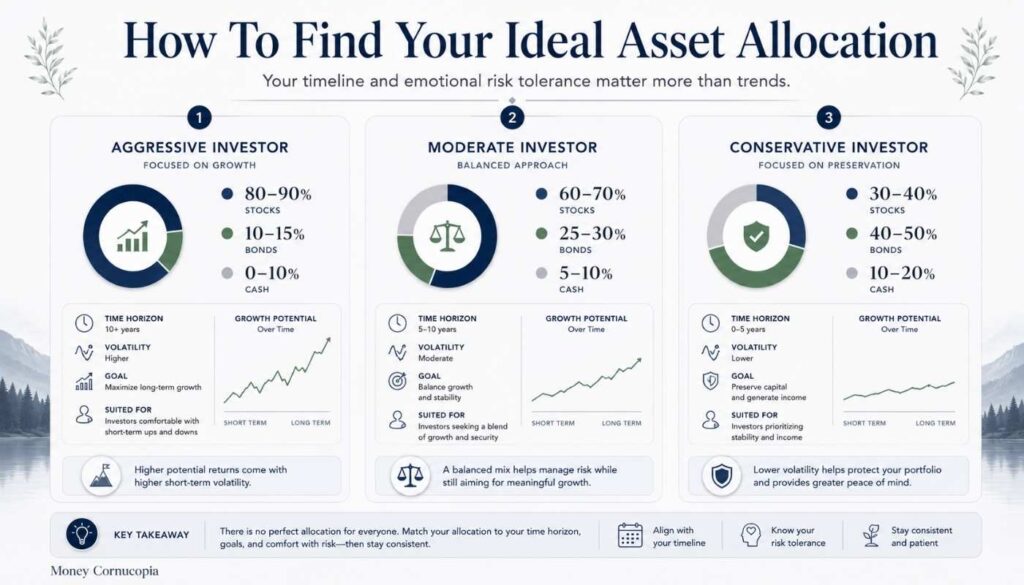

How to Find Your Ideal Asset Allocation

Your ideal allocation depends on two things: how long you are investing and how much risk you can handle emotionally.

Your Time Horizon

How many years before you need the money?

If you are investing for 10 years or more, you can afford to have a larger share in stocks because you have time to recover from market downturns. Stocks are volatile in the short term but have historically grown over long periods. This is where compound interest does its best work, quietly turning small, consistent investments into significant wealth over decades.

If you need the money within 1 to 3 years, you should lean more heavily toward bonds and cash. A market dip right before you need the money could force you to sell at a loss.

Your Risk Tolerance

This is the emotional side of investing. How would you feel if your portfolio dropped 20% in a single month?

If you would see it as a buying opportunity and stay calm, you would have a higher risk tolerance and can hold more stocks. If you would lose sleep, check your account constantly, and feel the urge to sell everything, you need more bonds and cash in your mix.

There is no wrong answer. The best asset allocation is the one you can actually stick with during bad times. A 90% stock portfolio is mathematically aggressive, but it is worthless if you panic and sell during the first downturn.

A Simple Starting Framework

Here is a common starting framework based on time horizon:

| Investor type | Stocks | Bonds | Cash | Best for |

|---|---|---|---|---|

| Aggressive | 80 to 90% | 10 to 15% | 0 to 5% | Young investors with 20+ years ahead |

| Moderate | 60 to 70% | 25 to 30% | 5 to 10% | Mid-career investors balancing growth and stability |

| Conservative | 30 to 40% | 40 to 50% | 10 to 20% | Investors nearing retirement or with short-term goals |

These are starting points, not rules. Your personal situation might call for something different. The important thing is having a deliberate allocation rather than randomly buying whatever feels exciting at the moment.

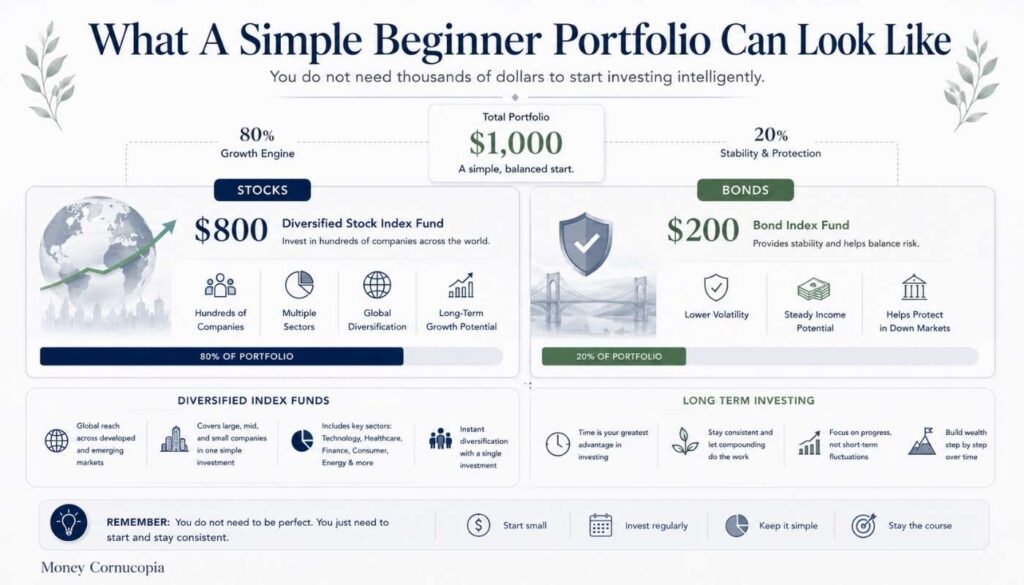

A Practical Example: What This Looks Like With $1,000

Theory is useful. Seeing real numbers is better.

Say you are a 25-year-old beginner with $1,000 to invest and a 20+ year time horizon. You decide on an 80/20 allocation: 80% stocks, 20% bonds.

Here is how that might look in practice:

A practical 80/20 portfolio with $1,000

25-year-old beginner. 20+ year time horizon. Two funds. Done.

| Amount | Where it goes | What you get |

|---|---|---|

| $800 (80%) | Total stock market index fund | Instant diversification across hundreds of companies, dozens of sectors, and multiple countries with a single purchase |

| $200 (20%) | Bond index fund | A mix of government and corporate bonds across different terms — adds stability and reduces overall portfolio volatility |

That is it. Two funds. One allocation decision. Instantly diversified across thousands of individual securities.

You do not need to pick individual stocks. You do not need to research 500 companies. Index funds do the diversification for you. This is why they are the most recommended starting point for beginners.

If you are wondering whether $1,000 or even $100 is enough to start, I covered that in detail in how to start investing with $100. The short answer is yes.

Use this free Compound Interest Calculator to estimate how your allocated money could grow over time.

The Rebalancing Habit: Keeping Your Plan Intact

Over time, your allocation will drift. Rebalancing brings it back.

If you start with 80% stocks and 20% bonds and the stock market has a great year, your portfolio might shift to 85% stocks and 15% bonds. That means you are now taking more risk than you planned.

Rebalancing is the process of selling some of what has grown too large and buying more of what has fallen behind. This brings your portfolio back to your target allocation.

It also forces you into the most powerful habit in investing: buying low and selling high. When you rebalance, you are automatically trimming the asset that has gotten expensive and adding to the one that has gotten cheap.

Most financial advisors recommend rebalancing once or twice a year, or whenever your allocation drifts more than 5% from your target.

How Asset Allocation Connects to Everything Else You Need to Know

Asset allocation does not exist in isolation. It connects to every other fundamental concept in personal finance.

If inflation is running higher than the return on your cash and bonds, your purchasing power is shrinking. That is why most long-term investors need some exposure to stocks, which have historically outpaced inflation.

The choice between stocks and bonds is the most fundamental asset allocation decision. Understanding how each one works helps you decide the right balance for your situation.

The time value of money explains why starting earlier with even a small, well-allocated portfolio beats starting later with a larger one. The earlier your money is invested in the right allocation, the longer compound interest has to work.

And Michael Saylor’s story of turning $250 million into $59 billion is ultimately a story about one extreme asset allocation decision, moving everything from cash (a melting ice cube) into a single scarce asset. That strategy worked for him, but it is the opposite of diversification. For most beginners, the lesson is not to copy his exact move but to understand the principle: where you allocate your money matters more than almost any other financial decision.

Frequently Asked Questions

What is the difference between asset allocation and diversification?

Asset allocation is the decision of how much of your portfolio goes into broad categories like stocks, bonds, and cash. Diversification is spreading your investments within each of those categories across many different companies, industries, and geographic regions. Asset allocation sets the big picture balance. Diversification protects you from the failure of any single investment within that balance.

Is diversification only for rich people?

No. Thanks to index funds and ETFs, you can own a diversified piece of the entire global economy with as little as $1. A single total stock market index fund holds hundreds or thousands of companies. You do not need to be wealthy to be diversified.

What is a good asset allocation for a beginner?

A common starting point for younger investors with a long time horizon is 80% stocks and 20% bonds using low-cost index funds. More conservative investors or those closer to retirement might choose 60% stocks and 40% bonds. The right allocation depends on your time horizon, risk tolerance, and financial goals.

Can I start investing with just $100 using asset allocation?

Yes. Many brokerages allow fractional share purchases, meaning you can buy a portion of an index fund for as little as $1. With $100, you can split your money across a stock index fund and a bond index fund to create a properly allocated and diversified portfolio from day one.

How often should I rebalance my portfolio?

Most financial advisors recommend rebalancing once or twice per year, or whenever your allocation drifts more than 5 percentage points from your target. Rebalancing too frequently can generate unnecessary transaction costs, while rebalancing too rarely can leave your portfolio riskier than intended.

Does diversification guarantee I will not lose money?

No. Diversification protects you from the failure of a single company or sector, but it cannot protect you from a general market decline. During a broad market crash, most investments drop together. However, diversification ensures that when the market recovers, your portfolio recovers with it because you are not dependent on any single investment to bounce back.

How does inflation affect my asset allocation?

If inflation runs higher than the return on your cash and bonds, your purchasing power shrinks over time. This is why most long-term investors allocate a significant portion of their portfolio to stocks, which have historically outpaced inflation over 10 to 20-year periods.

Final Thoughts

Asset allocation and diversification are not advanced strategies for professional investors. They are the starting point for anyone who wants to grow their money without gambling on a single stock or timing the market.

The core idea is simple. Decide how much risk you are comfortable with. Split your money accordingly across stocks, bonds, and cash. Then spread your investments within each category so that no single company, sector, or country can derail your plan.

You do not need to be rich to do this. You do not need to understand complex financial math. You need a plan, a couple of low-cost index funds, and the patience to let time and compounding do the heavy lifting.

If you are just starting out, begin with one decision: what percentage of your money goes into stocks versus bonds? Everything else follows from there.

Leave a Reply