I still remember staring at my savings account statement:

$0.14 in monthly interest… on $1,200.

That’s when it hit me.

My money wasn’t growing; it was sitting idle while the bank used it for free.

So I started searching for something better:

real compound interest investments that actually grow your money.

Not textbook examples. Not theory.

Real accounts and assets where you can see your money multiply over time.

In this guide, you’ll discover:

- The best compound interest investments you can start today

- What I’d do with just $100 in 2026

- And how to turn small savings into real growth

No fluff. No hype. Just what actually works.

Before diving into the investments, use this free Compound Interest Calculator to see how your $100 could grow over time.

What Is Compound Interest, Really? (And Why It’s The Closest Thing to a Financial Cheat Code)

Before we get to the list, let me make sure we’re speaking the same language, because “compound interest” gets thrown around a lot without anyone explaining why it actually matters.

Here’s the simple version: with regular (simple) interest, you earn returns only on your original deposit. With compound interest, you earn returns on your original deposit plus all the interest you’ve already earned.

It’s the difference between a snowball that melts a little every day and one that picks up more snow as it rolls downhill.

A quick example that hits differently when you see the math:

- You invest $5,000 at 7% annual return.

- Year 1: You earn $350. Balance: $5,350.

- Year 2: You earn 7% on $5,350 — that’s $374. Balance: $5,724.

- Year 10: Your balance is over $9,800 — without touching it.

- Year 30: Your original $5,000 has grown to nearly $38,000.

You didn’t put in a single extra dollar after year one. Time did the work.

This is why starting early matters more than starting big. A 25-year-old investing $200/month will almost always end up richer than a 40-year-old investing $600/month — simply because compound interest needs time as its fuel.

Table of Contents

The Best Compound Interest Investments (Ranked From Beginner-Friendly to Advanced)

I’ve organized these by accessibility and risk so you can find your starting point quickly. If you’re new to investing, start with Section 1. If you already have the basics covered, scroll to Section 2.

Section 1: Best Compound Interest Accounts for Beginners (Start With What You Have)

1. High-Yield Savings Accounts (HYSAs)

Best for: Anyone with cash sitting in a regular bank account earning next to nothing.

This is where most people should start — and where I started.

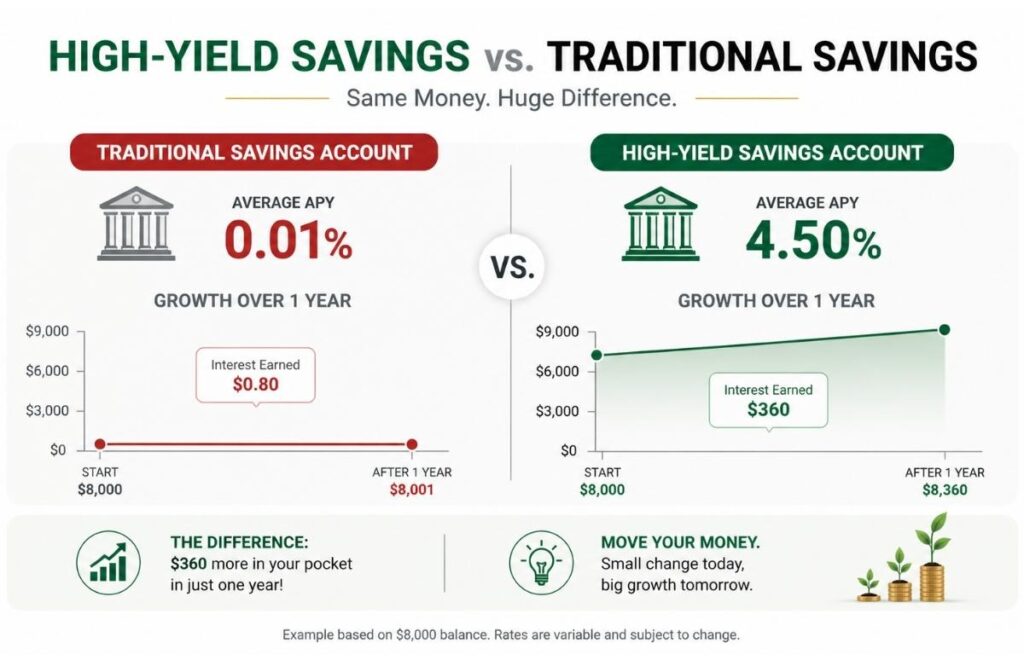

When I switched from a traditional bank savings account (earning 0.01% APY) to a high-yield savings account, my monthly interest went from pennies to real, meaningful dollars. In 2024, the best HYSAs were paying 4.5% to 5.0% APY — a staggering difference from what most big banks offer.

What makes them compound: Interest is calculated daily and added to your balance monthly. So every month, you’re earning interest on a slightly higher number than the month before.

Realistic case study: My friend Tariq kept $8,000 in a Chase savings account for two years, earning roughly $16 total. When he moved it to a high-yield account at 4.75% APY, he earned over $760 in the first year alone. Same money. Completely different result.

What to look for in a HYSA:

- APY of 4.0% or higher (as of 2026)

- No monthly fees or minimum balance requirements

- FDIC insured (up to $250,000)

- Easy online access and fast transfers

Quick note: Rates fluctuate with the Federal Reserve’s decisions. When the Fed cuts rates, HYSA rates typically follow. Don’t chase the single highest rate — look for a consistently competitive institution with no gotcha fees.

2. Certificates of Deposit (CDs)

Best for: Money you won’t need for 6 months to 5 years that you want to grow at a guaranteed rate.

CDs are essentially a deal you make with a bank: you promise to leave your money alone for a set period, and in return, they offer you a higher interest rate than a regular savings account.

The compounding here works the same way as HYSAs, but the rate is locked in — which can be great when rates are high and frustrating when they drop.

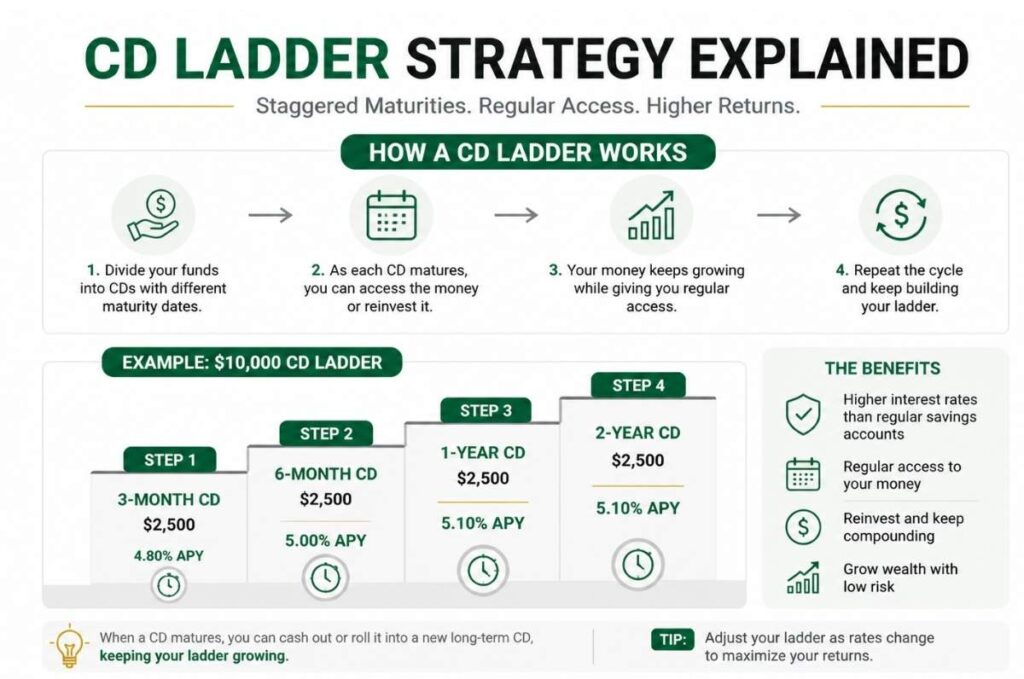

What I’d actually do: Consider a “CD ladder” — splitting your money across CDs with different maturity dates (3 months, 6 months, 1 year, 2 years). This gives you regular access to your money while still benefiting from higher rates on longer-term CDs.

Case Study — The $10,000 CD Ladder: A reader of mine (she asked to stay anonymous, so I’ll call her Priya) had $10,000 she wanted to keep safe but growing. She split it:

- $2,500 in a 3-month CD at 4.8% APY

- $2,500 in a 6-month CD at 5.0% APY

- $2,500 in a 1-year CD at 5.1% APY

- $2,500 in a 2-year CD at 4.9% APY

By the end of year one, she had earned approximately $482 in interest — and had access to her money in rolling 3-month windows. She felt none of the anxiety of having her savings “locked away” while still outperforming a regular savings account by a mile.

3. Money Market Accounts

Best for: People who want HYSA-level returns but with check-writing or debit access.

Money market accounts sit between a checking account and a savings account. They typically offer competitive interest rates with slightly more flexibility than a CD. The compounding works daily or monthly, depending on the institution.

They’re not dramatically better than HYSAs in most cases, but if you want to keep emergency funds accessible while still compounding them, a money market account is a sensible choice.

Section 2: Intermediate Compound Interest Investments (Where Real Wealth Is Built)

4. Index Funds and ETFs (The Compound Interest Powerhouse Most People Overlook)

Best for: Long-term investors who can leave money alone for 10+ years.

This is where the real compounding magic lives — and it’s also where most people make the mistake of looking for “better” options when this one is right in front of them.

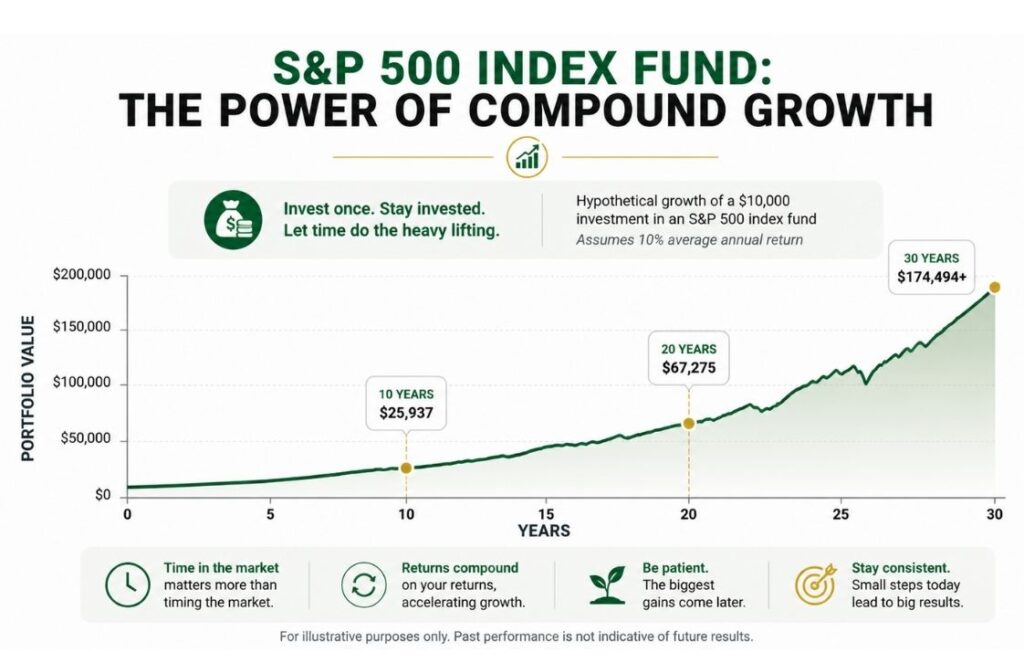

An S&P 500 index fund — like those offered by Vanguard, Fidelity, or Schwab — tracks the 500 largest US companies. Historically, the S&P 500 has returned about 10% annually on average (roughly 7% after inflation).

That might not sound dramatic. Until you compound it.

$10,000 invested in an S&P 500 index fund:

- After 10 years at 10% avg return: ~$25,937

- After 20 years: ~$67,275

- After 30 years: ~$174,494

Your original $10,000 becomes nearly $175,000 — without adding another cent.

Now add $200/month in contributions:

- After 30 years: over $430,000.

This is not a hypothetical. This is the mathematical reality of compound growth over time.

My personal experience: I started investing in index funds in my mid-20s with $150/month. Not because I had a lot of money, but because I finally understood that waiting until I had “enough” to invest was the biggest mistake I could make. The time I’d lose by waiting was irreplaceable.

What makes this “compound interest”? Technically it’s compound growth (since stocks don’t pay a fixed interest rate), but the mechanism is identical — returns are reinvested, and you earn returns on your returns. Dividend reinvestment especially creates this compounding snowball effect.

Key point for beginners: Use a tax-advantaged account. Maxing out a Roth IRA ($7,000/year in 2026) before investing in a taxable brokerage account is almost always the right move. Growth inside a Roth IRA is 100% tax-free in retirement.

5. Dividend Reinvestment (DRIP)

Best for: Investors who own dividend-paying stocks or ETFs and want their income to work harder automatically.

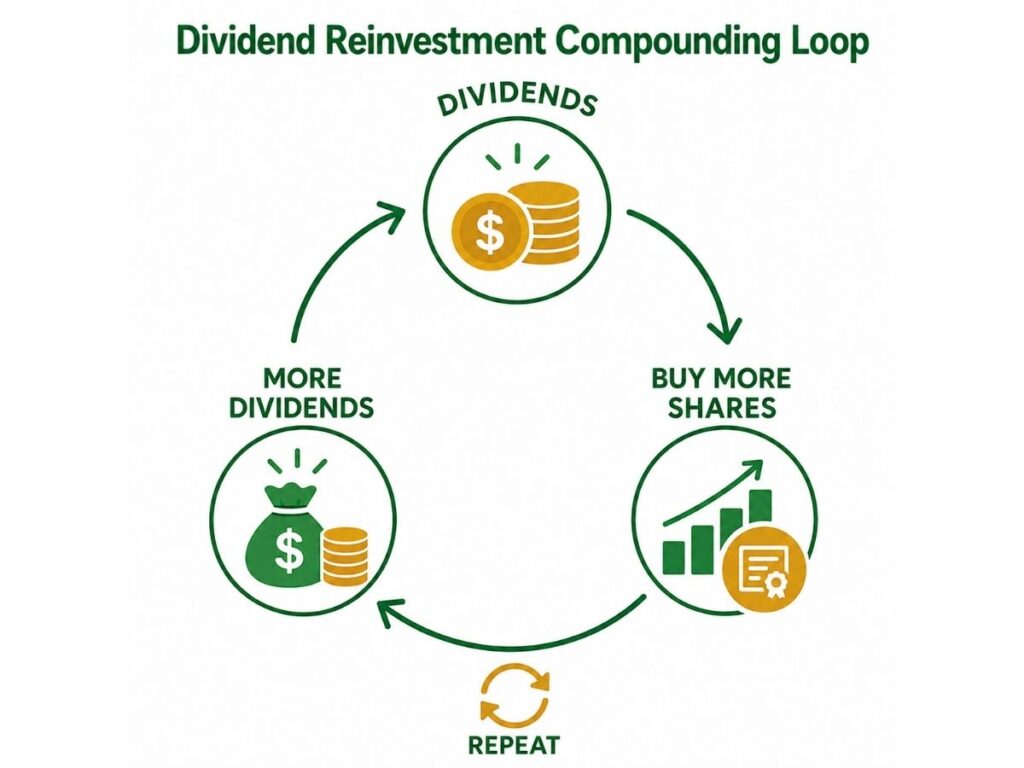

Dividend reinvestment means that instead of taking your dividend payments as cash, you automatically use them to buy more shares of the same stock or fund. Those new shares then generate their own dividends, which buy more shares, generating more dividends.

Sound familiar? That’s compounding.

A simple illustration: Imagine you own 100 shares of a dividend ETF worth $50/share. The fund pays a 3% annual dividend. That’s $150/year. If you reinvest those dividends, you now own 103 shares. Next year, your dividends will be slightly higher. The year after, higher still.

Over 20 or 30 years, this becomes a meaningful difference — studies show DRIP investors can accumulate 30–40% more wealth than those who take dividends as cash.

Most brokerages allow you to set up automatic dividend reinvestment for free. It takes about 90 seconds to turn on and then runs itself.

6. Real Estate Investment Trusts (REITs)

Best for: Investors who want real estate exposure without becoming a landlord.

REITs are companies that own income-producing real estate, apartment buildings, hospitals, data centers, and shopping centers. They’re legally required to distribute at least 90% of their taxable income to shareholders as dividends.

That makes them high-yield dividend payers — which, when reinvested, compound powerfully.

What I like about REITs:

- Accessible with as little as the price of one share (some are under $30)

- You get real estate diversification without the headaches of property management

- Publicly traded REITs can be bought and sold like any stock

What to watch out for:

- REITs are sensitive to interest rate changes (when rates rise, REIT prices often fall)

- Not all REITs are created equal — do your homework on occupancy rates, debt levels, and dividend history before buying

Case study: A colleague of mine started buying a diversified REIT ETF in 2018 with $300/month. By 2024, between price appreciation and reinvested dividends, his position had grown to roughly $32,000 from approximately $19,200 in contributions. That gap, $12,800, was compound growth doing its job.

Section 3: Advanced Options (For When You’re Ready to Go Further)

7. Bonds and Bond Funds (Stability with Compound Income)

Best for: Investors closer to retirement or anyone wanting to reduce portfolio volatility.

Individual bonds pay interest at fixed intervals, but bond funds automatically reinvest that interest — creating compound growth. Treasury bonds, corporate bonds, and municipal bonds each carry different risk/reward profiles.

In a balanced portfolio (say, 70% stocks / 30% bonds), the bond portion helps smooth out the turbulent years while still compounding quietly in the background.

8. I-Bonds (Inflation-Protected Compound Growth)

Best for: Money you want protected against inflation for 1–5 years.

Series I Savings Bonds are US government bonds that earn interest tied to the inflation rate. When inflation was running hot in 2022, I-Bonds were paying over 9% — attracting enormous attention from personal finance writers and savers alike.

The interest compounds every six months and is added to the bond’s principal, which then earns future interest. There are purchase limits ($10,000/year per person electronically) and you must hold them for at least 12 months.

They’re not a long-term wealth-builder on their own, but as a portion of your emergency fund or short-term savings, they’re a smart hedge.

9. Farmland and Alternative Assets (For Accredited Investors)

Best for: High-net-worth investors looking for portfolio diversification and inflation hedging.

Farmland has historically generated consistent returns — since 1990, US farmland has delivered average annual returns north of 10%, driven by both land appreciation and rental income from farmers.

Platforms like AcreTrader and FarmTogether allow accredited investors to purchase fractional interests in farmland. The income compounds as rental payments are reinvested.

Important caveat: These platforms are for accredited investors (generally those with $200K+ annual income or $1M+ net worth excluding primary residence). They’re also illiquid; you can’t sell them tomorrow if you need cash. Approach with eyes open.

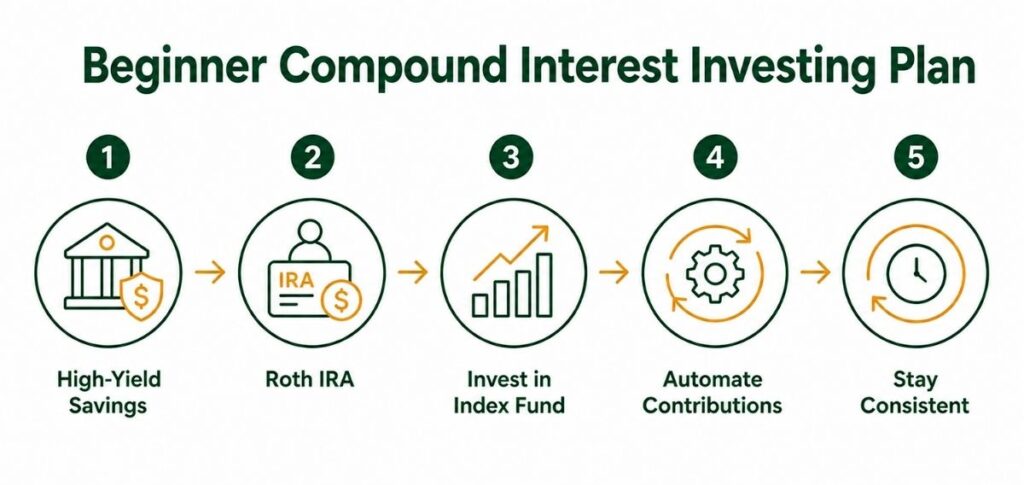

How to Start: A Beginner’s Compound Interest Playbook

If you’re reading this and thinking “okay, but where do I actually begin?”, here’s what I’d do if I were starting over today with $500:

- Open a high-yield savings account. Move your emergency fund (3–6 months of expenses) here. Let it compound while you build other investments.

- Open a Roth IRA. Contribute what you can — even $50/month matters more than you think. Invest it in a low-cost S&P 500 index fund.

- Turn on DRIP. If your brokerage account holds any dividend-paying fund or stock, turn on automatic dividend reinvestment immediately. It’s free and automatic.

- Automate everything. The biggest enemy of compound interest is you dipping into your investments when life gets messy. Automating contributions removes the temptation.

- Leave it alone. Seriously. The hardest part of compound investing isn’t finding the right account. It’s resisting the urge to pull money out during market dips or when a shiny new investment opportunity comes along.

The math is patient. You just have to be too.

Frequently Asked Questions FAQs

What’s the best compound interest investment for beginners?

A high-yield savings account for your emergency fund, and a Roth IRA invested in an S&P 500 index fund for long-term growth. These two together cover 80% of what most people need to start building wealth.

How much money do I need to start earning compound interest?

Far less than you think. Many high-yield savings accounts have no minimum balance. Index fund ETFs can be purchased for the price of a single share, some brokerages even allow fractional shares. You can literally start with $1.

How often does compound interest compound?

It depends on the account. Savings accounts and money market accounts typically compound daily and credit monthly. Index funds compound continuously as share prices rise and dividends are reinvested. CDs vary; read the terms before opening one.

Is compound interest better in a Roth IRA or a regular brokerage account?

A Roth IRA is almost always better if you qualify, because growth is tax-free. In a regular brokerage account, you pay capital gains taxes when you sell, which chips away at your compounded returns over time. Max your Roth IRA first ($7,000/year in 2026 if you’re under 50).

What kills compound interest?

Three things: withdrawing money early (you lose future compounding on everything you take out), fees (even 1% annual fees quietly eat 20–30% of your long-term returns), and inflation (if your savings account pays 0.5% and inflation is 3%, your money is actually shrinking in real terms).

How long does it take to see real results from compound interest?

This is the question nobody likes the honest answer to: it takes years. The first decade often feels slow. The second decade feels faster. The third decade is when people start calling it “magic.” The best time to start was yesterday. The second-best time is right now.

Can compound interest make you a millionaire?

Yes — with consistency, time, and patience. A 22-year-old who invests $400/month in an index fund averaging 8% annually would have over $1.5 million by age 62. That’s not a fantasy. That’s math.

The Bottom Line: Compound Interest Is Slow, Patient, and Quietly Powerful

Here’s the truth about compound interest that financial influencers rarely say out loud: it’s boring.

The best compound interest investment strategy isn’t a flashy app, a hot new alternative asset, or a product someone is getting paid to recommend. It’s opening the right accounts, automating your contributions, choosing low-fee investments, and then having the patience to leave everything alone for years at a time.

The readers I’ve seen build real, lasting wealth aren’t the ones who found the highest yield in a given month. They’re the ones who started earlier than most people, contributed consistently even when life was hard, and resisted the urge to do something clever when the market got scary.

You don’t need a PhD in economics to build wealth. You just need to understand how compound interest works, pick a few sensible vehicles for it, and get out of your own way.

If this article helped you, share it with someone who’s still keeping their savings in a 0.01% account. They’ll thank you in 10 years.

Money Cornucopia simplifies complex personal finance into easy, actionable steps. Nothing in this article constitutes personalized financial advice. Always consider your personal circumstances and consult a financial professional before making investment decisions.

Leave a Reply