Let me tell you about my cousin Tariq.

Tariq is one of the smartest people I know. Graduated near the top of his class, got a decent job, never gambled, never blew money on ridiculous things. But at 34 years old, he had exactly $312 in savings. Not $312,000. Three hundred and twelve dollars.

When I asked him why, he looked at me like I’d asked him why the sky is blue. “I don’t come from money,” he said. “Building wealth is for people who already have it.”

I’ve heard that sentence, or something close to it, from so many people that I’m starting to think it’s some kind of virus. A money mindset virus that spreads quietly and keeps perfectly capable people broke.

Here’s what Tariq didn’t know: wealth is not inherited. It’s engineered. And the blueprint? It’s not as complicated as Wall Street wants you to believe.

In this article, I’m going to give you the exact 5-step framework for building wealth from scratch, even if you’re starting with nothing, even if you grew up with nothing, and even if the word “investing” still makes your eyes glaze over.

Let’s get into it.

Table of Contents

But First: What Does “Wealth” Actually Mean?

Before we talk about how to build wealth, we need to agree on what it is. Because most people have it wrong.

Wealth is not a salary. A doctor earning $300,000 a year who spends $310,000 is not wealthy — they’re one missed paycheck away from a crisis. Wealth is also not a flashy car or a big house. Those are symbols of wealth, and very often, they’re funded by debt.

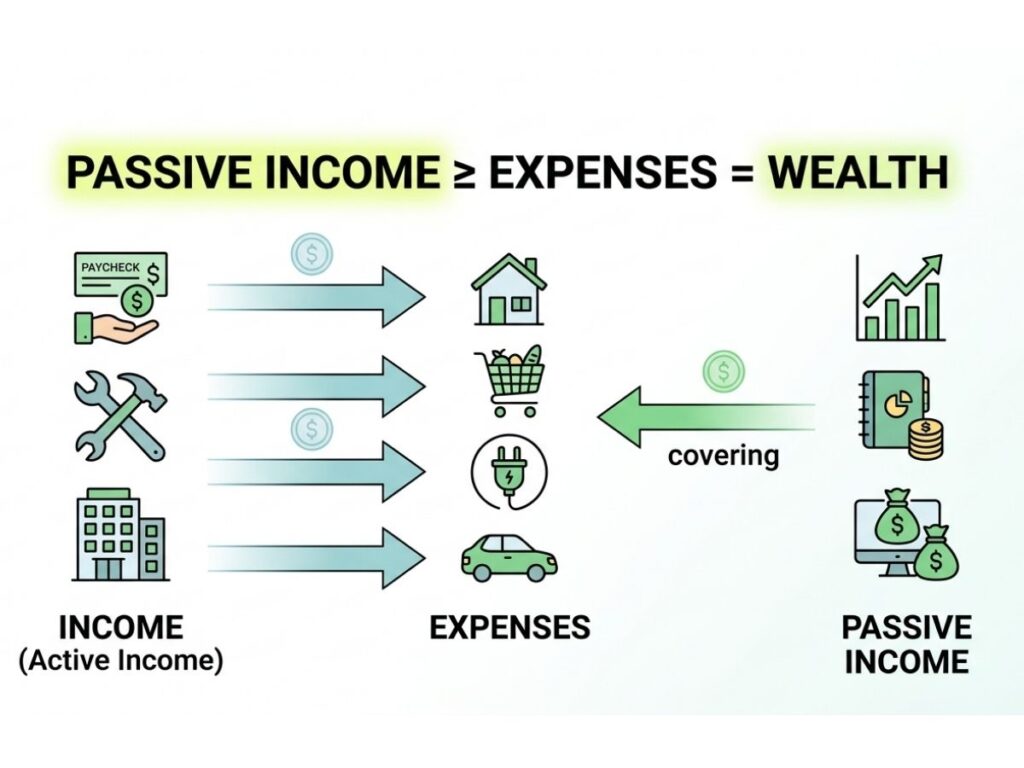

Real wealth is when your money works harder than you do.

More precisely, you are wealthy when your passive income (money coming in while you sleep) covers your living expenses. That’s it. That’s the finish line.

The good news? You don’t have to reach the finish line to start experiencing the benefits. Every step toward that line makes your life more stable, more flexible, and honestly, a lot less stressful.

Now. The blueprint.

Step 1: Stop the Bleeding (Fix Your Cash Flow)

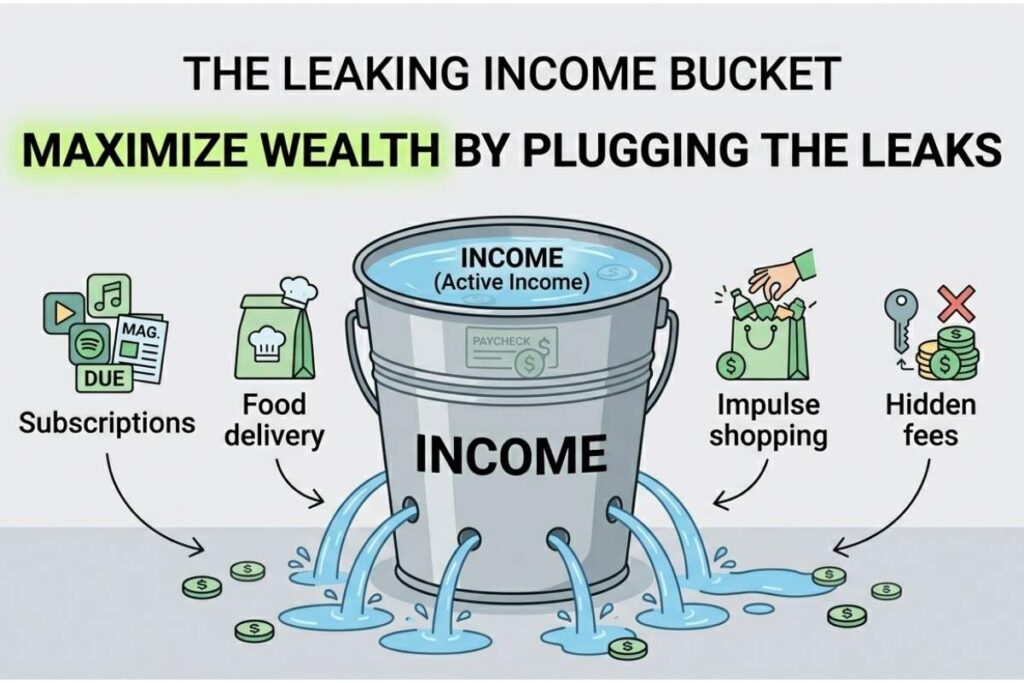

I once went three months without looking at my bank account. I’m not proud of it. I told myself I was “too busy,” but honestly? I was scared of what I’d see.

When I finally looked, really looked, I found $140/month going to a gym membership I hadn’t used since January (it was October). I found a $15/month subscription to a streaming service I’d signed up for during a free trial and completely forgotten. I found three separate food delivery apps all charging me annual fees.

That’s nearly $200 a month going absolutely nowhere.

Here’s the harsh truth: you cannot build wealth if more money is leaving than arriving. It’s like trying to fill a bathtub with the drain open. The first job is to plug the drain.

How to fix your cash flow right now:

Do a subscription audit. Go through your last two months of bank statements line by line. Highlight everything that recurs monthly. Cancel anything you forgot you had or don’t actively use. Most people find $50–200/month here.

Track every rupee/dollar for 30 days. Not to punish yourself — just to see. You cannot fix what you cannot see. Use a simple notes app, a spreadsheet, or any budgeting app. Just write it down.

Apply the 50/30/20 Rule:

- 50% of your take-home pay → Needs (rent, food, transport, utilities)

- 30% → Wants (eating out, entertainment, shopping)

- 20% → Savings and investments (this is non-negotiable — more on this shortly)

If your current math doesn’t allow for 20% savings, that’s okay. Start with 5%. Then push it to 10%. The number matters less than the habit.

Money Cornucopia Principle: Wealth is built in the gap between what you earn and what you spend. Widen the gap. Every. Single. Month.

Step 2: Build Your “Never Panic” Fund (Emergency Savings)

Here’s a scenario I want you to imagine.

It’s a Tuesday. Your car breaks down on the way to work. The mechanic calls and says it’ll cost $800 to fix. You have $200 in your account.

What do you do?

If you don’t have an emergency fund, you do one of three terrible things: you put it on a credit card (and pay 20%+ interest), you borrow from family (and damage a relationship), or you simply can’t fix the car and lose your job because you can’t get to work.

This is the cycle that keeps people broke. One emergency derails everything.

An emergency fund is the foundation of all wealth. Without it, every financial plan you build is one bad day away from collapse.

How big should your emergency fund be?

The standard advice is 3–6 months of living expenses. If your monthly expenses are $1,500, you need $4,500–$9,000 sitting in a savings account, untouched, earning interest.

That might sound like a lot. Here’s how to make it feel manageable:

Break it into milestones:

- Month 1 goal: $500 (your “small emergency” buffer)

- Month 3 goal: 1 month of expenses

- Month 6 goal: 3 months of expenses

- Month 12 goal: 6 months of expenses

Where to keep it: A high-yield savings account. Not under your mattress. Not in your checking account where you’ll spend it. A separate account that earns you some interest while it sits there, ready for when you need it.

My personal rule? I treat my emergency fund like it doesn’t exist — until I actually need it. Out of sight, out of mind, but always there.

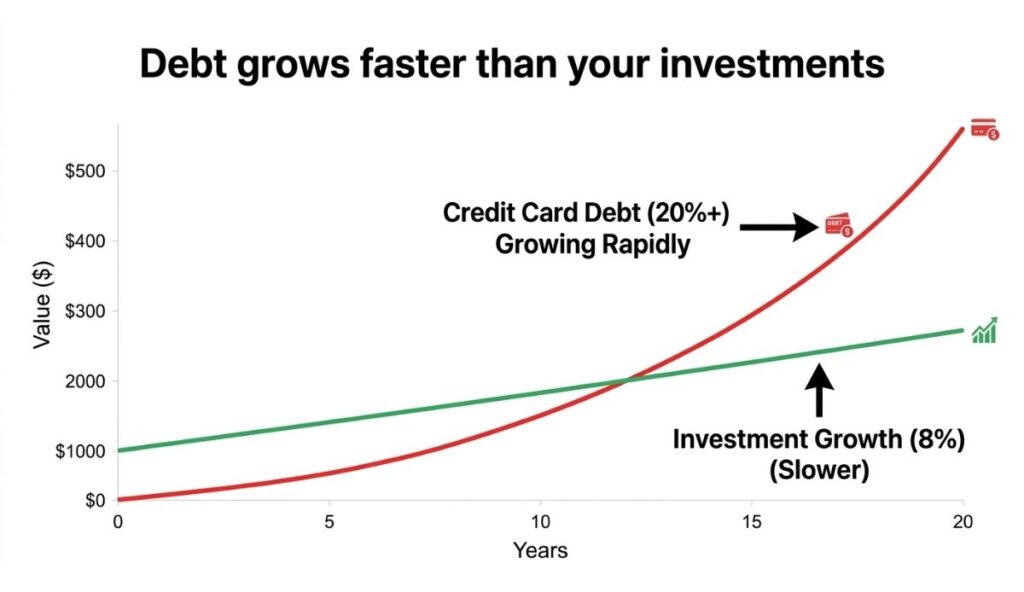

Step 3: Destroy High-Interest Debt (The Wealth Killer)

If Step 1 is plugging the drain and Step 2 is starting to fill the tub, then high-interest debt is someone drilling new holes while you’re not looking.

Credit card debt is, without exaggeration, one of the most destructive financial forces in an ordinary person’s life. At 20–30% annual interest, it grows faster than almost any investment you’ll ever make. While you’re trying to build wealth at 8% per year in the stock market, your credit card is eating it alive at 25%.

Let me make this real with numbers:

If you have $5,000 on a credit card at 22% interest and you only pay the minimum each month — you will pay over $8,000 in interest alone and take 15+ years to pay it off. On a $5,000 debt. That is $8,000 that will never be invested. Never compound. Never work for you.

Two proven strategies to crush debt:

The Avalanche Method (mathematically optimal): List all your debts from highest interest rate to lowest. Pay minimums on everything except the highest-rate debt — throw every extra dollar at that one. When it’s gone, attack the next. This saves the most money in interest.

The Snowball Method (psychologically powerful): List your debts from smallest balance to largest. Pay off the smallest one first, regardless of interest rate. When you kill that first debt, you get a rush of momentum that makes you want to keep going. Dave Ramsey swears by this one, and honestly? For people who struggle with motivation, it works.

Pick whichever one you’ll actually stick to. The best strategy is the one you follow.

One rule: Once a debt is paid off — do not refill it. This seems obvious. It is not obvious to your future self at 11pm on a Friday with a shopping app open.

Step 4: Make Your Money Grow (Start Investing)

This is the step where most people freeze up. “Investing is complicated.” “I don’t know enough.” “I’ll start when I have more money.”

I said all three of those things for two years. Two years of my money sitting in a savings account earning 0.5% interest while inflation quietly ate it alive.

Here’s the truth no one tells you clearly: not investing is a decision. It’s a decision to let inflation shrink your money a little bit every year. Staying in a savings account isn’t “safe” — it’s slowly losing ground.

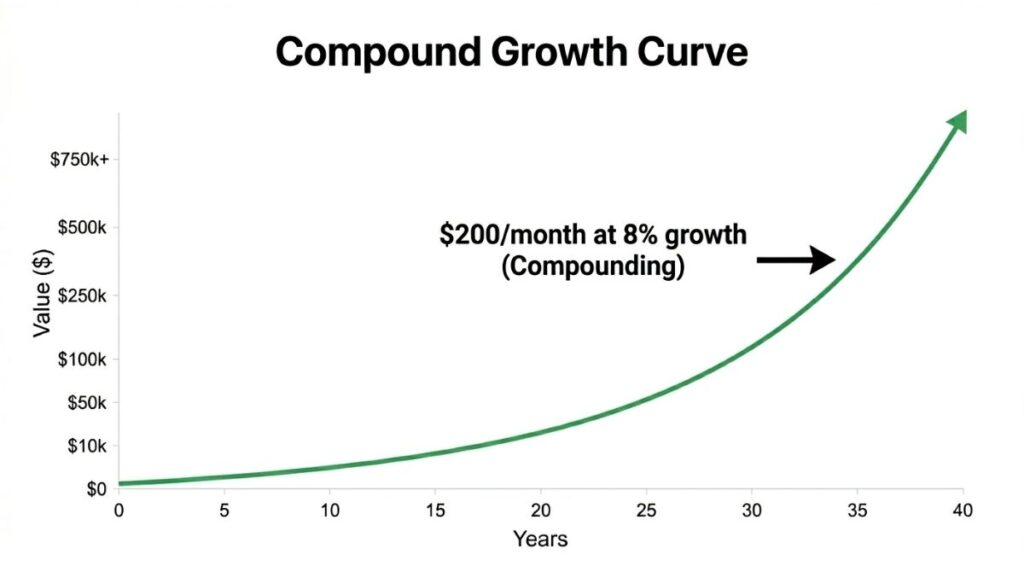

The beautiful thing about investing as a beginner is that you don’t need to pick stocks, read earnings reports, or understand complex financial instruments. You just need to understand one concept: compound interest.

Albert Einstein reportedly called compound interest the eighth wonder of the world. The idea is simple: your money earns returns. Then those returns earn their own returns. Then those returns earn returns. It snowballs — slowly at first, then explosively.

Here’s what that looks like in real life:

If you invest $200 per month starting at age 25 with an average annual return of 8%:

- By age 35 (10 years): ~$36,000

- By age 45 (20 years): ~$118,000

- By age 55 (30 years): ~$300,000

- By age 65 (40 years): ~$700,000

You contributed $96,000 of your own money over 40 years. The rest — over $600,000 — was created by compound interest doing its quiet, relentless work.

Where to start investing as a beginner:

Index Funds: Instead of picking individual stocks (risky, complicated, time-consuming), you buy a small slice of thousands of companies at once. When the overall market goes up — and historically, over the long run, it always has — your investment goes up. Low fees, low effort, highly effective.

ETFs (Exchange-Traded Funds): Similar to index funds but traded on the stock market like individual stocks. Very beginner-friendly.

Stocks vs. Bonds split: As a beginner, a simple starting point is: subtract your age from 100. That’s your stock percentage. If you’re 30, put 70% in stocks and 30% in bonds. As you age, gradually shift more toward bonds for stability.

The golden rule: Start now. Start small if you have to — even $25 a month. But start. Time in the market beats timing the market every single time.

Step 5: Protect and Multiply What You’ve Built

Most wealth-building advice stops at “invest in index funds.” That’s good advice. But it’s incomplete.

Building wealth isn’t just about growing your money — it’s about making sure a single bad event doesn’t wipe out everything you’ve spent years building.

Protect your wealth with insurance:

Health insurance is non-negotiable. A single serious illness without coverage can generate medical bills that take decades to pay off. This is not hypothetical — it’s the leading cause of bankruptcy in many countries.

Life insurance matters the moment someone depends on your income — a spouse, children, aging parents. Term life insurance is affordable and straightforward. Get it before you think you need it.

Emergency fund (yes, again) — I keep mentioning it because the wealthiest people I know treat their emergency fund like a sacred covenant. It is the buffer between you and financial catastrophe.

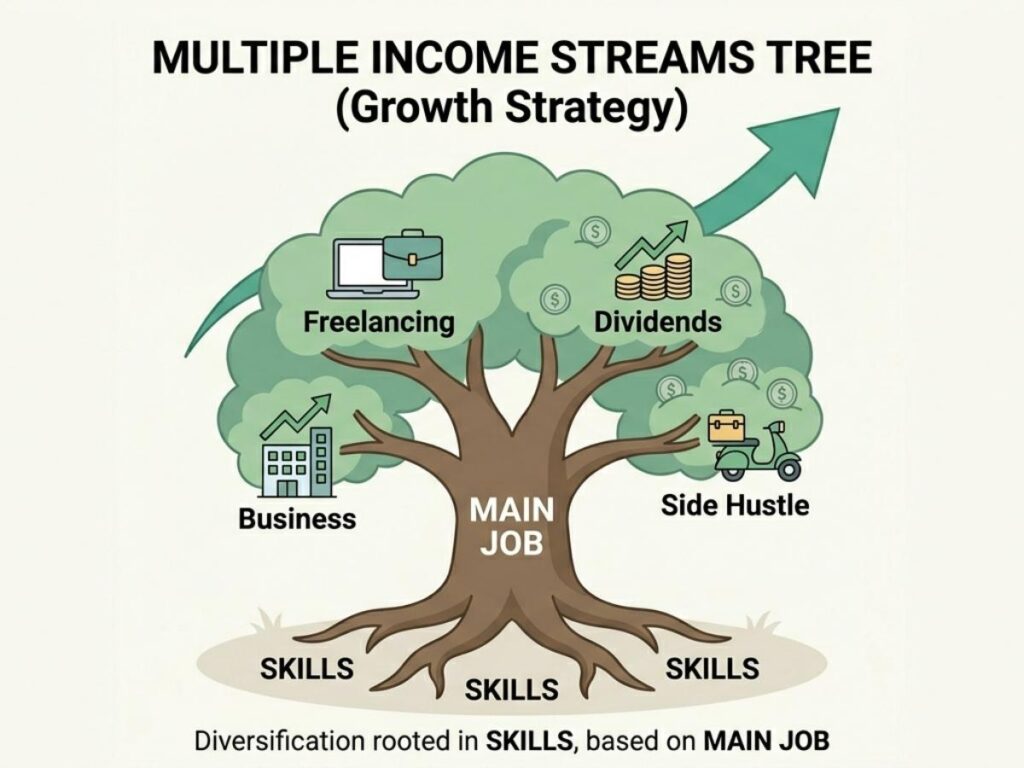

Multiply your wealth with income streams:

Building wealth from one job, one income source, is possible — but fragile. The wealthy don’t just have one river of money; they have many streams feeding into it.

Consider:

- Side income: Freelancing, tutoring, selling a skill online

- Passive income: Dividends from investments, interest from bonds, rental income if you get there

- Invest in yourself: Skills that make you more valuable — coding, writing, sales, communication — these raise your earning power, which accelerates everything above

You don’t need five income streams tomorrow. Start building a second one. Then a third. Each one you add makes the whole system more resilient.

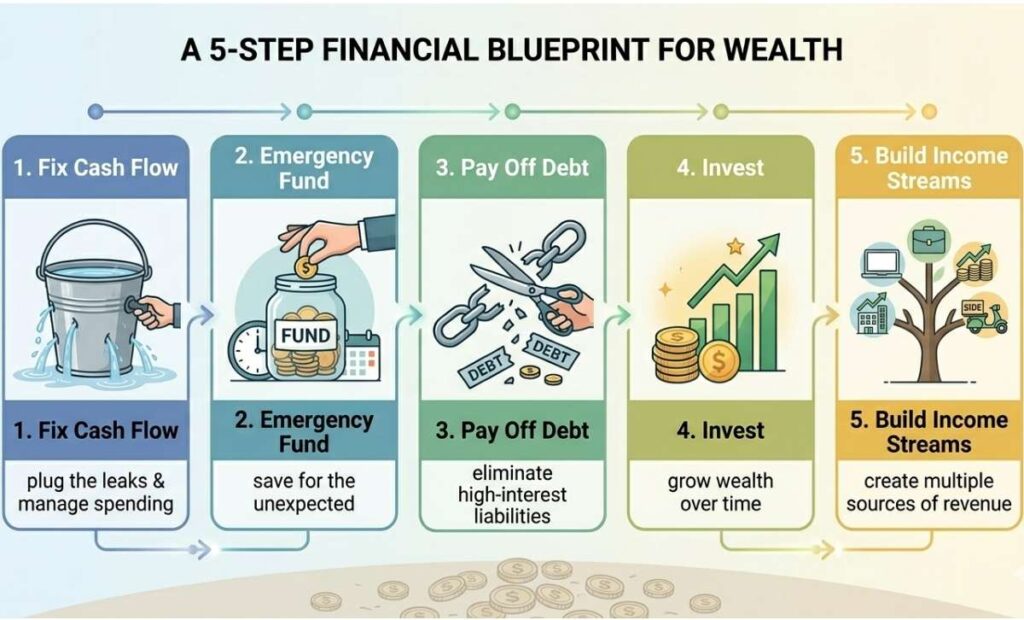

The Full Blueprint at a Glance

Here’s your 5-step wealth-building framework, simplified:

| Step | Action | Goal |

|---|---|---|

| 1 | Fix cash flow — stop the bleeding | Spend less than you earn |

| 2 | Build an emergency fund | 3–6 months of expenses saved |

| 3 | Eliminate high-interest debt | Freedom from the wealth killers |

| 4 | Start investing consistently | Let compound interest do the heavy lifting |

| 5 | Protect and multiply | Build multiple streams, shield what you have |

These steps are sequential for a reason. It’s hard to invest effectively if you’re drowning in debt. It’s hard to pay off debt if your cash flow is broken. Work them in order, even if it feels slow.

The Real Secret Nobody Talks About

You want to know the actual difference between people who build wealth and people who don’t?

It’s not intelligence. It’s not income. It’s not connections or luck or a trust fund.

It’s consistency over a long period of time.

That’s it. I know it sounds anticlimactic. We live in a world that sells us overnight success stories, crypto millionaires, and 30-under-30 lists. But the vast, overwhelming majority of real wealth is built quietly — one month of saving, one boring index fund contribution, one cancelled subscription, one avoided impulse purchase at a time.

My cousin Tariq, by the way? He started with Step 1 six months ago. He cancelled subscriptions, set up a $100/month auto-transfer to a savings account, and opened his first investment account with $250. He hasn’t gotten rich. But for the first time in a decade, he’s not living in fear of the next emergency.

That’s where wealth begins. Not with a windfall. Not with a hot stock tip. With a decision, followed by another decision, followed by a habit, followed by a life that looks completely different five years from now.

The best time to start was ten years ago. The second-best time is today.

Your Action Step for This Week

Don’t try to do all five steps at once. Pick one thing from this article and do it this week:

- ✅ Cancel one subscription you forgot you had

- ✅ Open a high-yield savings account for your emergency fund

- ✅ List all your debts and their interest rates

- ✅ Open an investment account and make your first deposit — even if it’s $25

- ✅ Calculate your 50/30/20 budget for this month

Small action. Repeated consistently. That’s the whole game.

Which step are you starting with? Drop a comment below — let’s build this together. 💰

Want to go deeper? Read our guides on What is Compound Interest? The “Magic” Way to Grow Your Money, Stocks vs Bonds: Are You an Owner or a Lender?, and What is Inflation? A Beginner’s Guide to Purchasing Power

Leave a Reply