I still remember the conversation that changed everything.

It was 2019, and I was sitting in a coffee shop with my friend Sarah, a financial advisor. I’d just told her I wanted to start investing, but I only had about $100 saved up. I expected her to laugh or tell me to come back when I had “real money.”

Instead, she said something that stuck with me: “The best time to plant a tree was 20 years ago. The second best time is today. Even if that tree is just a seedling.”

That $100 I invested in 2019? Thanks to compound interest and consistent additions, it’s grown into something I never imagined back then. And here’s the truth most people don’t realize: you don’t need thousands of dollars to start building wealth. You just need to start.

If you’re reading this with $100 (or even less) and wondering if it’s “enough” to begin investing, this guide is for you.

Table of Contents

Why $100 is Actually Enough to Start

Let me be blunt: the finance industry has spent decades convincing you that investing is only for wealthy people. They used to require minimum deposits of $3,000, $5,000, or even $10,000 just to open an account. This kept regular people locked out while the rich got richer.

But in 2026, that wall has completely crumbled.

Thanks to technology and fractional shares, you can now invest with as little as $1. Yes, ONE dollar. But let’s talk about why starting with $100 is actually the perfect amount:

The Power of Starting Small

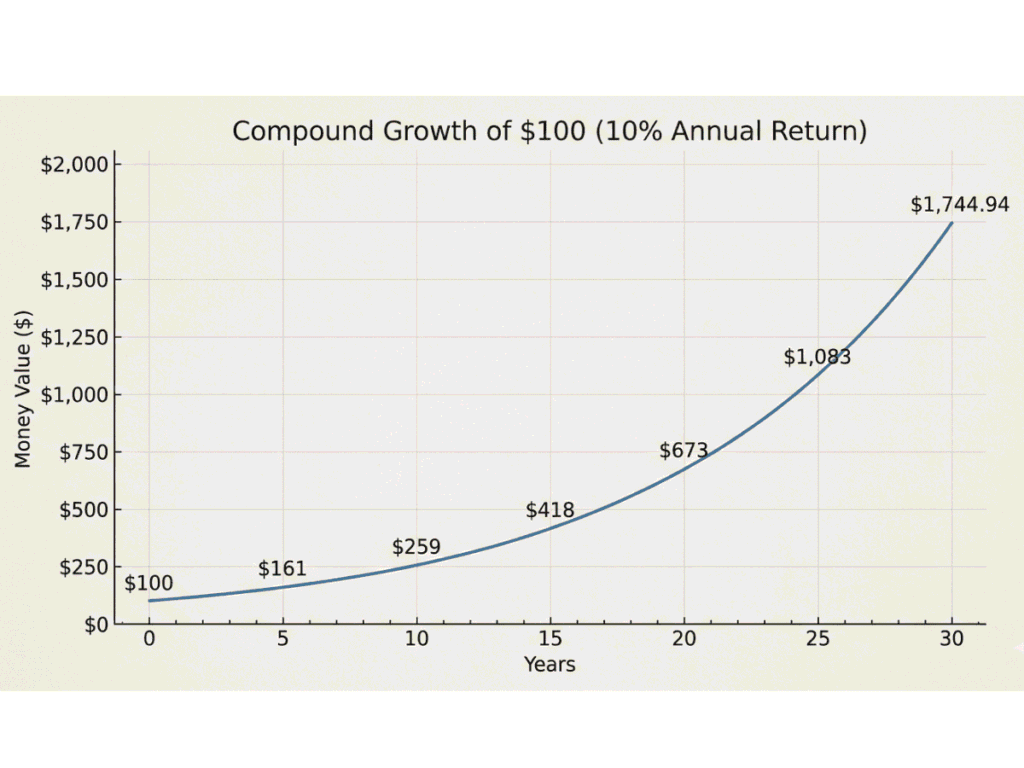

Here’s what happens when you invest $100 today at a 10% average annual return (which is historically what the S&P 500 has delivered):

- After 1 year: $110

- After 5 years: $161

- After 10 years: $259

- After 20 years: $673

- After 30 years: $1,745

“But that’s not life-changing money!” you might say.

You’re right. But here’s what you’re missing: most people who start with $100 don’t stop there.

Use this free Compound Interest Calculator to see exactly how your $100 could grow depending on your return and timeline.

The Real Value: Building the Habit

When I invested my first $100, the money itself wasn’t the point. What mattered was that I:

- Learned how to invest without risking my life savings

- Overcame the fear that keeps most people stuck

- Built the habit of investing regularly

- Saw my money grow (even if slowly), which motivated me to invest more

Within 6 months, I was adding $50 every paycheck. Within a year, I bumped it to $100. That initial $100 wasn’t my fortune—it was my starting line.

The “Wait Until I Have More” Trap

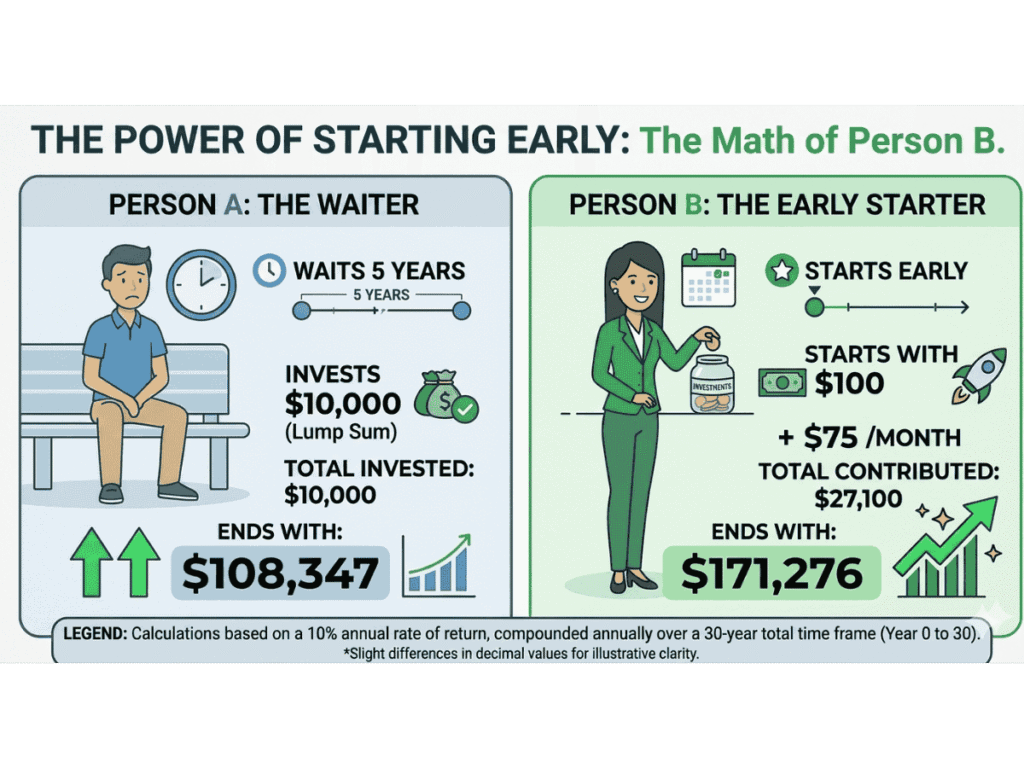

Here’s the math that will shock you:

Person A waits 5 years to save up $10,000, then invests it all at once.

Person B invests $100 today and adds just $75/month for 5 years.

Who has more money after 30 years (assuming 10% returns)?

- Person A: $174,494

- Person B: $184,824

Person B wins by over $10,000—even though they started with WAY less money.

Why? Because of the Time Value of Money. Every year you wait is a year you can’t get back. Starting with $100 today beats waiting to invest $1,000 tomorrow.

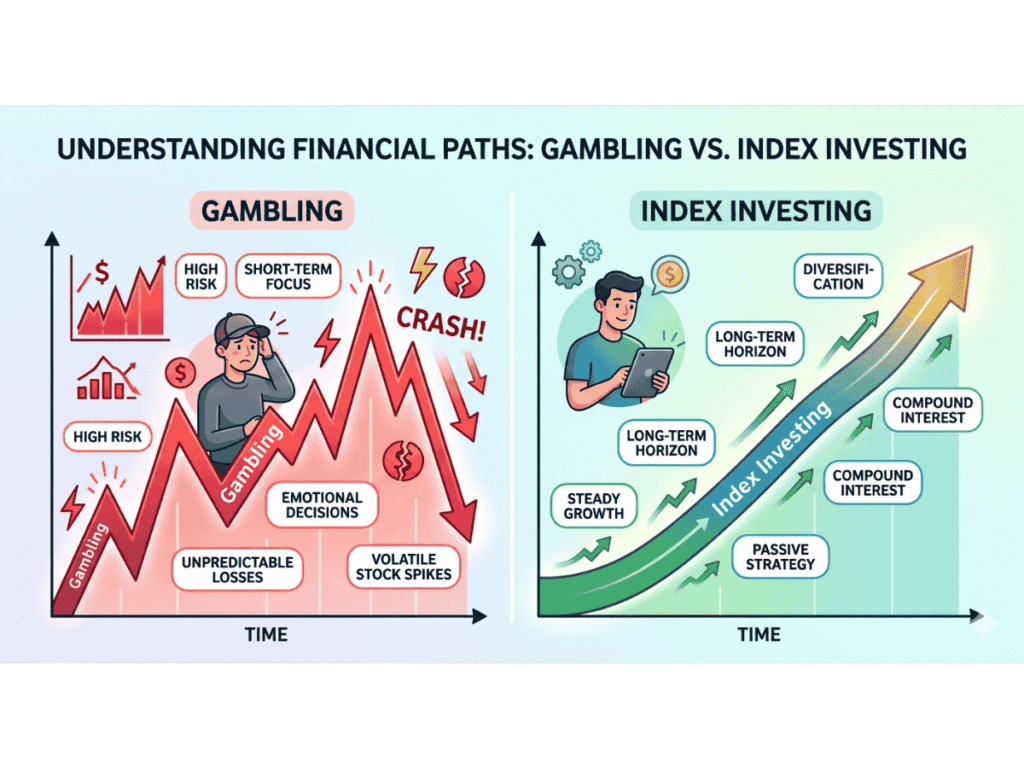

The Biggest Mistake Beginners Make

Before we dive into the “how,” let’s talk about the mistake that costs beginners more money than anything else:

Trying to “beat the market” with risky individual stocks.

I see this all the time. Someone has $100, and instead of building a solid foundation, they:

- Buy one share of a “hot stock” they heard about on social media

- Try day trading with apps that make investing feel like a casino

- Chase meme stocks or crypto with no strategy

Look, I get it. It’s boring to invest in index funds when everyone’s talking about the latest stock that went up 300% overnight. But here’s what they don’t tell you: for every stock that explodes upward, there are dozens that crash and burn.

When you only have $100, you can’t afford to gamble. You need to build a foundation.

What Works Better: Index Funds

An index fund is like buying a tiny slice of the entire stock market. Instead of betting on one company, you own a piece of hundreds or thousands of companies.

For example, the S&P 500 index fund gives you ownership in:

- Apple

- Microsoft

- Amazon

- Tesla

- …and 495 other top U.S. companies

If one company tanks, you barely feel it. If the overall economy grows (which it has for the past 100+ years), you profit.

This is how the wealthy invest. Warren Buffett himself recommends index funds for regular people.

Where to Invest Your First $100

Okay, you’re convinced. You’ve got $100. Now what?

Here are your best options, ranked by how I’d approach them:

Option 1: High-Yield Savings Account (If You Need Safety)

Best for: Emergency fund or short-term savings (less than 2 years)

How it works: Your money sits in a savings account earning interest, currently around 4-5% annually at top banks.

Returns: Low but guaranteed

Risk: Almost zero (FDIC insured up to $250,000)

My take: This isn’t technically “investing,” but if you don’t have an emergency fund yet, start here. Once you have 3-6 months of expenses saved, move to actual investments.

Where to open one:

- Marcus by Goldman Sachs (4.5% APY)

- SoFi (4.6% APY + $25 signup bonus)

- Ally Bank (4.35% APY)

Option 2: Index Fund via Robo-Advisor (Easiest for Beginners)

Best for: Complete beginners who want automatic investing

How it works: You answer a few questions about your goals and risk tolerance. The robo-advisor builds a portfolio of index funds for you and automatically rebalances it.

Returns: 6-10% average annually (historical)

Risk: Medium (your money can go down short-term)

My take: This is where I started. It’s simple, automated, and takes emotion out of investing. Perfect for $100.

Top robo-advisors:

- Betterment (no minimum, 0.25% fee)

- Wealthfront (no minimum, 0.25% fee)

- M1 Finance (no minimum, free for basic plan)

Option 3: S&P 500 Index Fund (What I Actually Do)

Best for: People comfortable with DIY investing

How it works: You open a brokerage account and buy shares of an S&P 500 index fund like VOO or SPY.

Returns: ~10% average annually (historical)

Risk: Medium (stock market fluctuates)

My take: This is the simplest long-term strategy. Buy it, hold it, add to it regularly, and don’t check it obsessively.

Where to buy:

- Robinhood (no fees, beginner-friendly app)

- Webull (no fees, free stock signup bonus)

- Fidelity (no fees, traditional brokerage)

Option 4: Fractional Shares of Individual Stocks (Riskier)

Best for: People who want to own specific companies

How it works: You can buy a fraction of expensive stocks. Love Apple, but it’s $170/share? Buy $20 worth (0.12 shares).

Returns: Varies wildly

Risk: High (individual stocks can tank)

My take: Only do this with money you’re okay losing. Even then, make it 10-20% of your portfolio max.

Option 5: Your 401(k) or IRA (The Tax-Smart Move)

Best for: Long-term retirement savings

How it works:

- 401(k): If your employer offers one, invest here FIRST if they match contributions (that’s free money)

- Roth IRA: You can open one yourself and invest $100 to start

Returns: Depends on what you invest in (usually index funds inside the account)

Risk: Medium

My take: If your employer matches 401(k) contributions, invest there before anywhere else. A 100% instant return (via the match) beats everything.

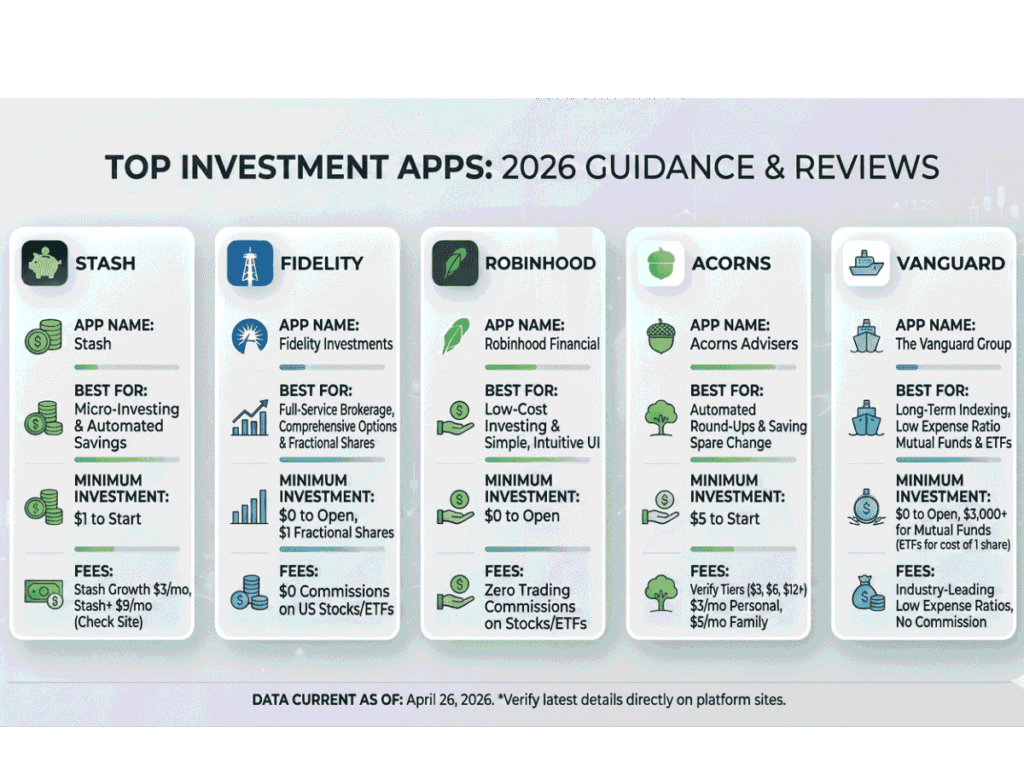

5 Best Investment Apps for Small Amounts

Let me walk you through the top platforms I recommend for beginners in 2026, based on fees, ease of use, and features.

1. Robinhood — Best for Absolute Beginners

Minimum investment: $1

Fees: $0 trading fees

Why I like it: Dead simple interface, fractional shares, instant deposits

Pros:

- Easiest app to use (seriously, a child could do it)

- No commissions on stocks or ETFs

- Great for learning without stress

Cons:

- Limited research tools (you’ll outgrow it eventually)

- Customer service can be slow

Best for: Someone making their very first investment who wants zero complexity.

My verdict: This is where I’d start if I were beginning today. Put in $100, buy a fraction of an S&P 500 ETF like VOO, and you’re officially an investor.

2. Webull — Best for Free Stock Bonuses

Minimum investment: $1

Fees: $0 trading fees

Signup bonus: Up to $75 in free stocks

Why I like it: You literally get free money just for signing up and depositing. That’s an instant return before you even invest.

Pros:

- Free stocks (usually worth $12-75)

- Better research tools than Robinhood

- Extended trading hours

Cons:

- Interface is slightly more complex

- Overwhelming for total beginners

Best for: Someone who wants a signup bonus and doesn’t mind a learning curve.

3. M1 Finance — Best for Long-Term Portfolios

Minimum investment: $100

Fees: $0 for basic plan

Why I like it: “Pies” lets you build custom portfolios and auto-rebalance

How it works: You create a “pie” of investments (e.g., 60% S&P 500, 30% bonds, 10% real estate). Every time you add money, it automatically distributes across your pie to maintain those percentages.

Pros:

- Completely free for basic investing

- Automatic rebalancing

- Great for “set it and forget it.”

Cons:

- Only trades once per day (not good for active traders)

- $100 minimum to start

Best for: Investors who want to build a balanced portfolio and automate everything.

4. Acorns — Best for Automatic Investing

Minimum investment: $5

Fees: $3-5/month

Why I like it: Invests your spare change automatically

How it works: Connect your debit card. Every time you buy something, Acorns rounds up to the nearest dollar and invests the change. Buy coffee for $4.50? It invests the extra $0.50.

Pros:

- Completely passive

- Great for people who struggle to save

Cons:

- $3/month fee eats into returns when you’re starting small

- Less control over investments

Best for: Someone who never remembers to invest manually.

My verdict: It’s clever, but that $3/month fee is 3% of your $100 starting balance annually—too high. I’d use this once you have $500+ invested.

5. Fidelity — Best Traditional Brokerage

Minimum investment: $0

Fees: $0 for stocks and ETFs

Why I like it: It’s a real, respected brokerage with decades of experience

Pros:

- Incredible research tools

- 24/7 customer service

- Wide range of investment options (stocks, bonds, mutual funds, IRAs)

Cons:

- Less “fun” interface than newer apps

- Feels old-school

Best for: Someone who wants a serious, long-term platform they won’t outgrow.

My verdict: If you’re thinking long-term and want one platform forever, start here.

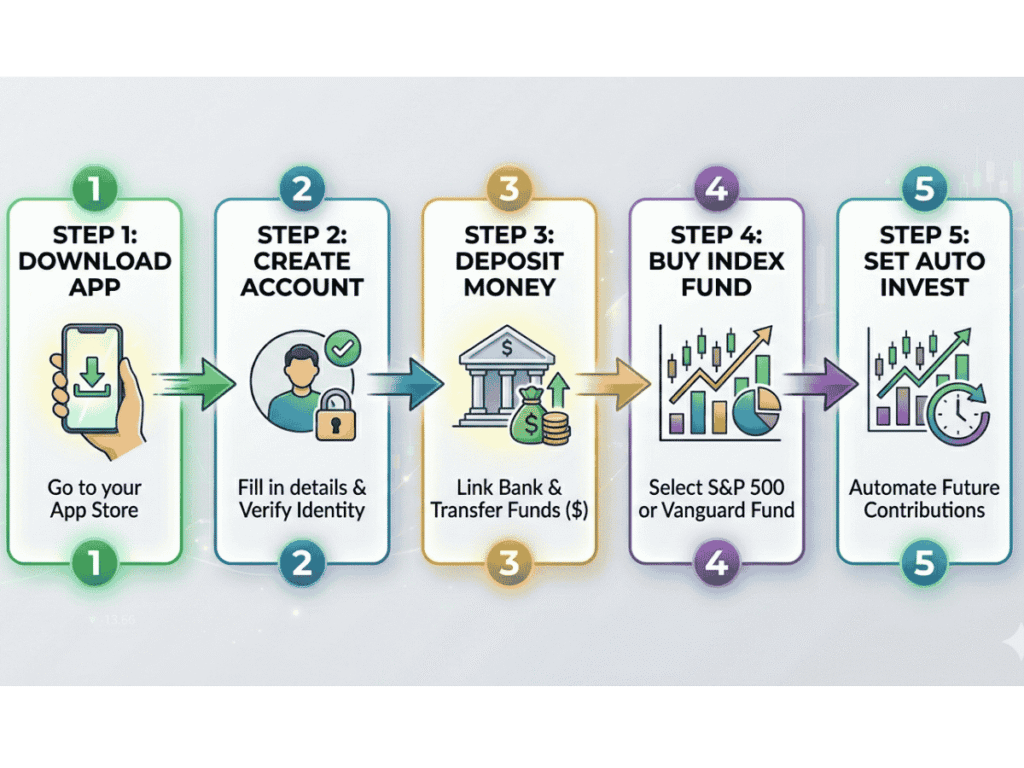

Step-by-Step: Your First Investment in 30 Minutes

Alright, enough theory. Let’s actually DO this. I’m going to walk you through making your first investment using Robinhood (the easiest option).

Step 1: Download the App (3 minutes)

- Go to your phone’s app store

- Download “Robinhood”

- Open the app

- Click “Sign Up”

Step 2: Create Your Account (5 minutes)

You’ll need:

- Your Social Security Number (for tax purposes)

- A valid ID (driver’s license or passport)

- Your bank account information

Answer the basic questions:

- Employment status

- Annual income

- Investment experience (be honest—”beginner” is fine)

Step 3: Link Your Bank Account (3 minutes)

- Click “Add Bank Account”

- Enter your bank login OR use account/routing numbers

- Verify with the micro-deposits they send (usually instant)

Step 4: Deposit $100 (1 minute)

- Click “Transfer”

- Choose “Deposit”

- Enter $100

- Select “Instant” (available immediately with Robinhood Gold trial) or “Standard” (3-5 days)

Step 5: Make Your First Investment (10 minutes)

Now for the exciting part:

- Tap the search icon

- Type “VOO” (Vanguard S&P 500 ETF)

- Click on VOO

- Tap “Trade”

- Choose “Buy”

- Select “Dollars” (not shares)

- Enter $100

- Review your order:

- You’re buying: ~$100 of VOO

- This equals approximately 0.19 shares (fractional)

- Swipe up to submit

That’s it. You’re now an investor. You own a piece of 500 of America’s biggest companies.

Step 6: Set Up Recurring Investments (5 minutes) — CRITICAL

This is where the magic happens. Don’t just invest once—automate it.

- Go to VOO in your portfolio

- Click “Invest on a schedule.”

- Choose:

- Amount: $25, $50, or $100 (whatever you can afford)

- Frequency: Weekly, bi-weekly, or monthly

- Start date: Your next payday

Why this matters: You’ve just built a wealth-building machine. Every paycheck, money automatically moves from your bank to investments. You’ll never “forget” to invest. And dollar-cost averaging means you buy more shares when prices are low, fewer when they’re high.

Step 7: Forget About It (Seriously)

Close the app. Live your life. Don’t check it every day.

The stock market goes up and down. If you check constantly, you’ll panic when it drops 5% in a day and sell at a loss. But if you ignore it for 5-10 years? It almost always goes up.

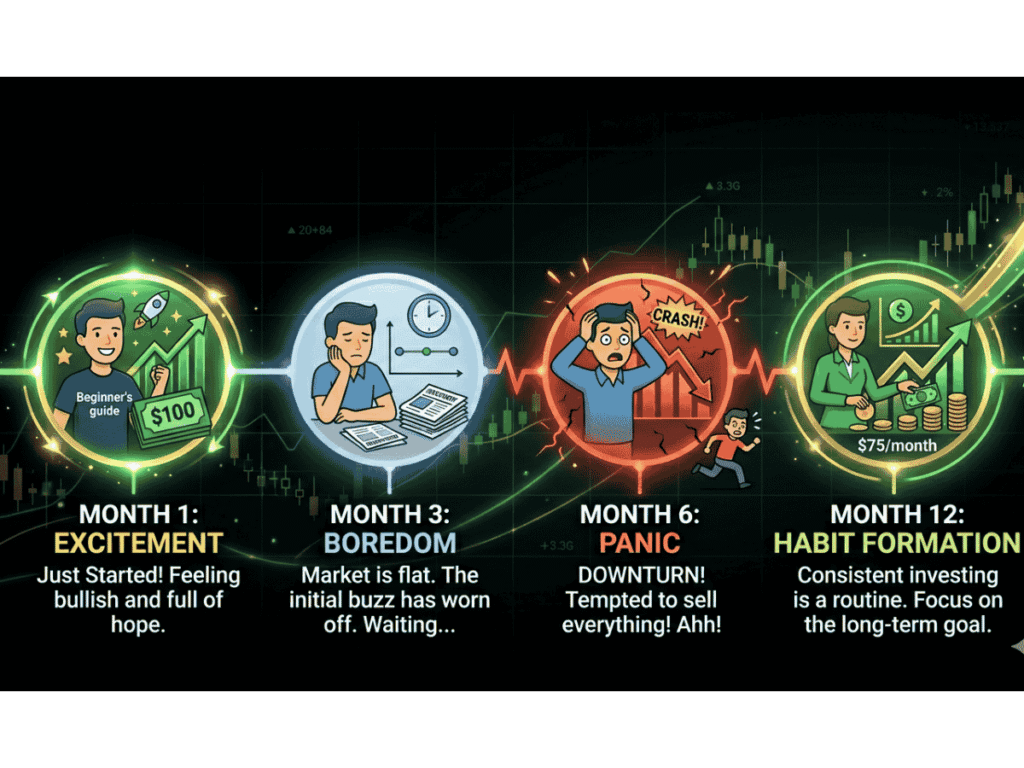

What to Expect in Your First Year

Let’s set realistic expectations because nobody talks about this part.

Month 1: Excitement and Obsession

You’ll check your portfolio 10 times a day. You’ll feel like a real investor. You might be up $3 or down $4. You’ll screenshot your gains and feel proud.

This is normal. Enjoy it, but don’t let it control you.

Months 2-3: Boredom

The novelty wears off. Your $100 is now $103… or $97. Nothing dramatic happens.

This is where most people quit. Don’t. This is when you’re building the foundation.

Months 4-6: The First Real Test

The market will have a bad week. Your $100 might drop to $92. You’ll panic.

“I should sell before it gets worse!” your brain will scream.

DO NOT SELL. This is the market testing you. Every successful investor has been here. The ones who held on got wealthy. The ones who sold stayed broke.

Months 7-12: The Habit Forms

By now, you’ve been auto-investing for months. You barely think about it. Your $100 is now $450 (from your monthly contributions) and has grown to maybe $485.

That’s $35 in gains you did NOTHING to earn. It just… happened.

You’re starting to see why this works.

Realistic First-Year Returns

If you:

- Start with $100

- Add $50/month automatically

- Get a 10% average return

After 1 year, you’ll have:

- Total invested: $700

- Account value: ~$730-760

- Profit: $30-60

That might not sound like much. But remember:

- You learned to invest without losing sleep

- You built a habit that will make you wealthy

- You earned money while literally doing nothing

- You’re lapping everyone who’s “waiting for the right time.”

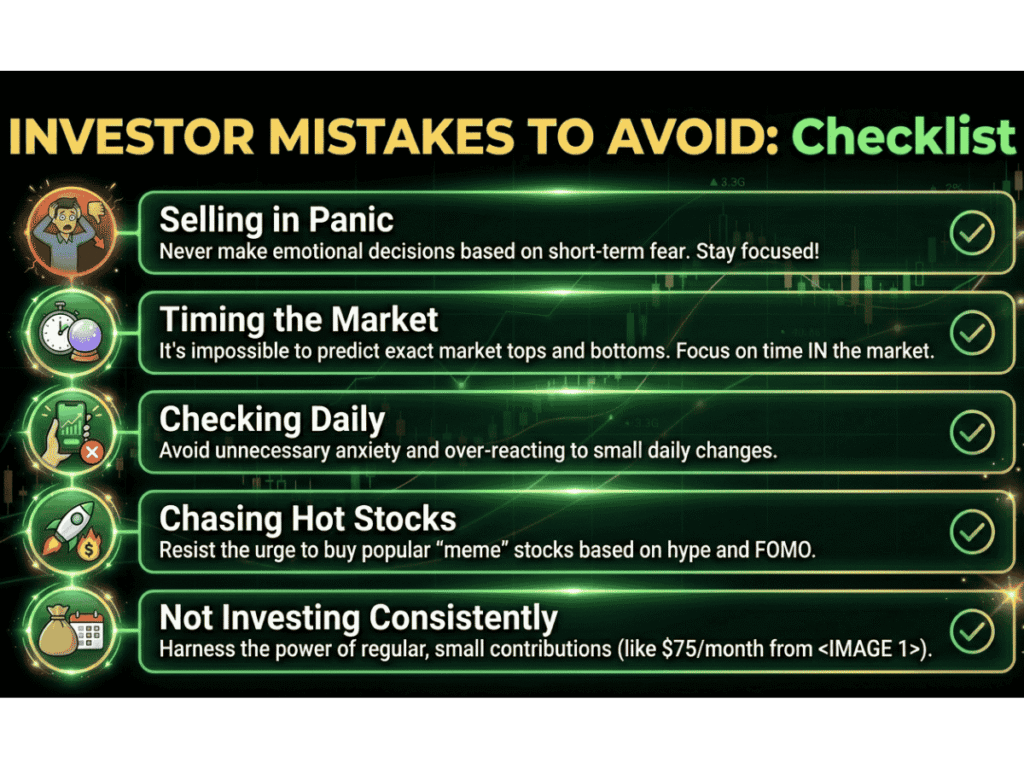

Common Mistakes to Avoid

I’ve made these. My friends have made these. You’ll be tempted to make these. Don’t.

Mistake #1: Selling When the Market Drops

The scenario: The market drops 10% in a week. Your $100 is now $90.

What people do: Sell to “stop the bleeding.”

What you should do: Buy MORE. Everything is on sale.

Why it matters: Since 1928, the S&P 500 has had 26 years where it dropped over 10%. In 100% of those cases, it eventually recovered and went higher. Selling locks in your loss. Holding (or buying more) turns it into a gain.

Mistake #2: Trying to Time the Market

The scenario: “I’ll invest when the market drops a bit more.”

What actually happens: The market goes up 20% while you wait for the “perfect” entry.

The data: Missing just the 10 best days in the stock market over 30 years reduces your returns by 50%. You can’t predict these days. Just stay invested.

Mistake #3: Checking Your Portfolio Daily

The problem: The market fluctuates. Seeing red numbers triggers anxiety, even when nothing is actually wrong.

The solution: Check monthly at most. Or better yet, quarterly. Your investment horizon should be 5-30 years, not 5 days.

Mistake #4: Chasing “Hot Stocks”

The scenario: Your coworker made $500 on some crypto/meme stock/NFT. You want in.

The reality: By the time you hear about it, the gain already happened. You’re buying at the peak. It crashes. You lose money.

The alternative: Boring index funds have beaten 90% of “hot stock” traders over any 10-year period.

Mistake #5: Stopping After the Initial $100

The biggest mistake? Investing once and never again.

Your $100 today will grow, but it won’t change your life. What changes your life is investing $100… then $50 next month… then $75… then $100/month… consistently for years.

Wealth is a habit, not an event.

FAQ: Starting with $100

Can I really make money investing only $100?

Yes, but let’s be honest about timelines. If you invest $100 once and never add to it, you’ll have ~$259 in 10 years (at 10% returns). That’s nice, but not life-changing.

The real power comes from adding to it regularly. Invest $100 now, then add $50-100/month, and in 10 years you could have $10,000-20,000. That’s real money.

What’s the safest investment for $100?

A high-yield savings account or Treasury bonds. You’ll earn 4-5% with almost zero risk. It won’t make you rich, but it won’t make you poor either.

If you want growth, an S&P 500 index fund is the safest stock market investment. It’s not guaranteed, but it’s as close as stocks get.

Should I invest $100 or pay off debt?

Great question. Here’s my rule:

Credit card debt (15-25% interest)? Pay that off first. No investment beats guaranteed 20% returns.

Student loans (4-7% interest)? This one’s close. I’d split it: $50 to loans, $50 to investing.

Mortgage (3-4% interest)? Invest the $100. Your returns will likely beat the interest.

Can I lose money investing $100?

Yes, but let me explain what that really means.

Short-term (1-2 years): Absolutely. The stock market can drop 20-30% in a bad year. Your $100 could become $70.

Long-term (10+ years): Historically, the S&P 500 has never had a negative return over any 20-year period. Ever. Since 1928.

So yes, you can lose money if you panic and sell during a downturn. But if you hold, history says you’ll profit.

How long until I see returns?

Technically, you could see returns today if the market goes up. But meaningful, life-changing returns? Think 5-10+ years.

This isn’t a get-rich-quick scheme. It’s a get-rich-slowly guarantee.

What if I can only invest $50 or $25?

Do it. Right now. Don’t wait until you have $100.

The difference between $50 and $100 is tiny compared to the difference between $0 and $50. Starting matters more than the amount.

Should I use a savings account or invest?

Both. Here’s the framework:

First $1,000: High-yield savings (your emergency starter fund)

Next $100-500: Start investing (learn the ropes)

Build to 3-6 months expenses: Back to savings (full emergency fund)

Everything after that: Invest aggressively

You need both. Savings =

Your Next Steps

You’ve read this far. That puts you ahead of 95% of people who will think about investing but never actually do it.

Here’s exactly what to do in the next 24 hours:

Today (30 minutes):

- ✅ Download an investment app (I recommend Robinhood for beginners)

- ✅ Create your account

- ✅ Link your bank account

- ✅ Deposit $100

Tomorrow (10 minutes):

- ✅ Buy your first investment (VOO or a robo-advisor portfolio)

- ✅ Set up automatic recurring investments

- ✅ Close the app and don’t check it for a month

Next Month:

- ✅ Add $25-100 to your investment (whatever you can afford)

- ✅ Read one article on investing (keep learning)

In One Year:

- ✅ Review your portfolio (you’ll be amazed at your progress)

- ✅ Increase your monthly contributions if possible

- ✅ Teach someone else how to start

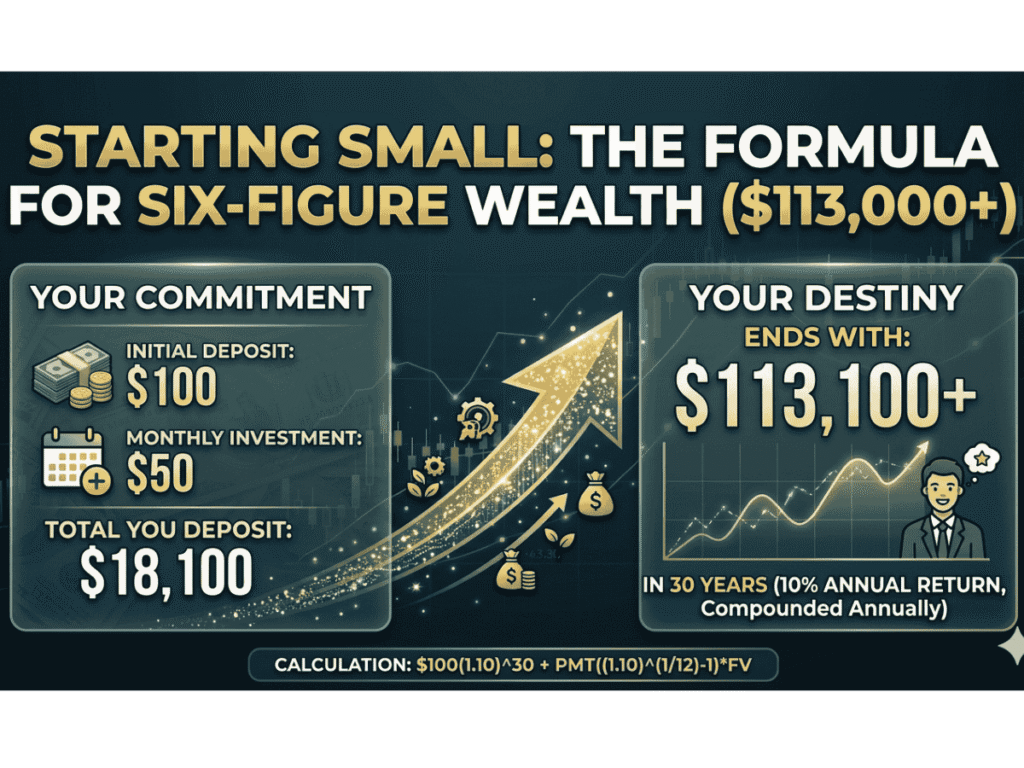

The Truth About $100

That $100 in your bank account isn’t going to change your life sitting there.

But $100 invested today, with $50 added every month for the next 30 years? That becomes $113,000.

And here’s the beautiful part: you’re not going to add “just $50” for 30 years. As you earn more, you’ll invest more. Most people who start with $100 are investing $500-1,000/month within 5 years.

But they had to start somewhere.

They had to overcome the voice that said “it’s not enough.”

They had to plant that tiny seedling even though it didn’t look like much.

The best time to invest was 10 years ago. The second-best time is right now.

Your $100 is enough. You are ready. The only question is: will you actually do it?

Related Articles

Want to go deeper? Check out these guides:

- What is Compound Interest? The “Magic” Way to Grow Your Money

- Time Value of Money for Beginners: A Simple Guide

- How to Use Asset Allocation & Diversification to Grow Wealth

Disclaimer: This article is for educational purposes only and should not be considered financial advice. Investing involves risk, including the potential loss of principal. Always do your own research and consider consulting with a financial advisor before making investment decisions. The author may earn affiliate commissions from some links in this article at no cost to you.

Your turn: Did you invest your first $100? What app did you choose? Drop a comment below and let me know where you’re starting your journey!

Leave a Reply