Your cash is losing value right now. Not because you are spending it. Because inflation is quietly melting it away.

Most people never think about this. They check their bank balance, see the same number, and assume their money is safe. It is not. Every year that inflation outpaces your savings interest, your purchasing power shrinks. Your balance stays flat. What it can buy does not.

Michael Saylor, the CEO of a software company called MicroStrategy, noticed this in 2020 when he realized his $500 million in cash reserves was losing roughly $75 million in real value every single year. His response was to apply one of the oldest principles in finance, move his money from a melting asset into a scarce one, and that decision turned $250 million into a fortune worth tens of billions.

This article is not really about Bitcoin or about billionaires. It is about the one financial principle behind Saylor’s move, why that principle matters for your savings, and how the same rule works whether you have $500 million or $100.

Table of Contents

The Melting Ice Cube Problem

Most people think of cash as safe. Saylor realized it was the opposite.

Think of your cash as an ice cube sitting on a kitchen counter. Every hour, it melts a little. You cannot see the change minute by minute, but come back after a full day and a half, and the ice cube is gone.

That is what inflation does to your cash. It does not disappear overnight. It melts slowly, quietly, consistently. A dollar today buys less than a dollar last year. A dollar last year bought less than a dollar five years ago.

If you have ever noticed that groceries cost more than they used to, or that rent keeps climbing, or that the same salary feels tighter than it did a few years ago, you have already felt the melting ice cube.

Between 2020 and 2021, the Federal Reserve’s balance sheet nearly doubled as the government injected trillions into the economy to keep it afloat during the pandemic. I covered this concept in detail in my article on what inflation actually is and how it erodes your purchasing power. The short version is this: when governments print more money, each individual dollar becomes worth less. Your bank balance stays the same, but what it can buy quietly shrinks.

Saylor understood this better than most. He calculated that his $500 million was losing roughly $75 million in real purchasing power every single year. Not because he was spending it. Because the dollar itself was becoming worth less.

He called his cash a “melting ice cube.” And he decided to stop holding it.

The One Rule Behind the $59 Billion Pivot

The rule Saylor used is not new. It is one of the oldest principles in finance.

It is called the Time Value of Money. The idea is simple: a dollar today is worth more than a dollar tomorrow, because today’s dollar can be invested and grow. But there is a flip side that most people miss.

If you store your money in something that loses value over time (like cash during high inflation), you are going backwards. If you store your money in something that is scarce and holds or gains value over time, you are going forward.

Saylor thought of money as a battery for storing time and energy. You work, you earn, you save. Those savings are stored energy. The question is, what container are you storing it in?

A leaky container (cash that inflates away) drains your stored energy over time. A solid container (an asset with a limited supply that holds value) preserves or grows it.

That is the entire insight. It is not complicated. It is not a secret Wall Street formula. It is a principle you can find in any introductory finance textbook. The difference is that Saylor actually acted on it when most people did not.

What Saylor Actually Did

In August 2020, Saylor made his move.

When Bitcoin was trading around $10,000 per coin, he took $250 million of his company’s cash reserves and converted it into Bitcoin. His logic was straightforward. Bitcoin has a fixed supply of 21 million coins that can never be increased. The U.S. dollar has no supply limit and was being printed at record speed. In the long run, a scarce asset will hold value better than an unlimited one.

But he did not stop at $250 million. He used three financial strategies to accelerate his position.

Strategy 1: Low-Cost Debt

Saylor borrowed billions of dollars at extremely low interest rates, often near 0%. The money was cheap to borrow but expensive to hold as cash (because of inflation). So he converted the borrowed cash into Bitcoin immediately.

This is a concept I covered in my article on the risk-return tradeoff. Higher potential returns come with higher risk. Saylor accepted the risk of Bitcoin’s price volatility in exchange for the potential of long-term appreciation. He calculated that the risk of holding melting cash was actually greater than the risk of holding a volatile but scarce asset.

Strategy 2: Aggressive Compounding

As Bitcoin’s value grew, Saylor’s company used the gains to raise more capital and buy more Bitcoin. This created a compounding effect where each purchase made the next purchase possible.

This is the same principle that makes compound interest powerful for everyday investors. Whether you are compounding interest in a savings account or compounding asset growth in an investment portfolio, the math is the same. Growth builds on growth.

Strategy 3: Patience Over Decades

Saylor did not sell when Bitcoin dropped 50%. He did not sell when the media called him reckless. He did not sell when other companies abandoned their Bitcoin positions.

He held on because he was thinking in decades, not days. The Time Value of Money works over long time horizons. Over 10 or 20 years, a scarce asset in a world of increasing money supply has a mathematical advantage. Saylor trusted the math.

The Result

By early 2026, Saylor’s company (now renamed Strategy) held over 600,000 Bitcoin worth tens of billions of dollars. The exact value changes daily with Bitcoin’s price, but the trajectory has been clear. What started as a $250 million bet became one of the largest corporate fortunes built in the 21st century.

Why Most People Missed This Lesson

This is not really a story about Bitcoin. It is a story about a financial principle.

Most people missed Saylor’s lesson because they focused on the wrong part. They saw “CEO buys Bitcoin” and filed it under crypto speculation. What they missed was the underlying logic that applies to everyone.

The logic is this: if you hold your savings in a form that loses value over time, you are falling behind even if your bank balance stays the same. If you move your savings into assets that hold or grow in value, you are moving forward.

That does not mean everyone should buy Bitcoin. It means everyone should understand what their cash is actually doing.

If your savings account pays 3% interest but inflation is running at 4%, your money is melting. Slowly. Quietly. Just like Saylor’s $500 million was melting before he acted.

The asset you choose depends on your situation, your risk tolerance, and your timeline. It might be index funds. It might be real estate. It might be a diversified portfolio of stocks and bonds. The principle stays the same regardless of the asset.

Stop storing your time and energy in a leaky container.

What This Means If You Have $100

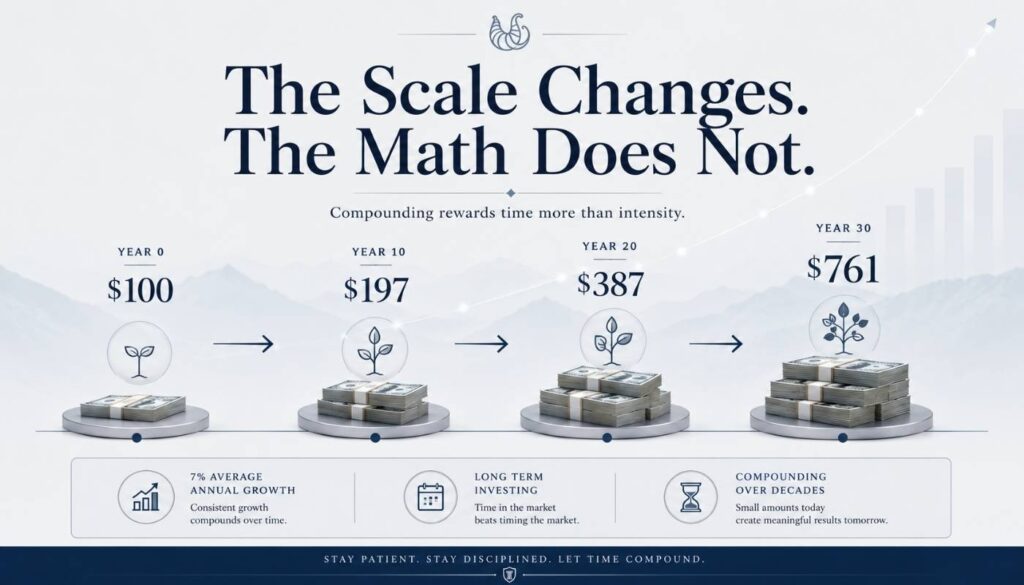

You do not need $500 million for this rule to work. You need $100 and patience.

The Time Value of Money does not care how much you start with. It cares how long you let it work.

If you have $100 and you leave it in a regular savings account earning 1% while inflation runs at 3%, you are losing roughly $2 of real purchasing power every year. That is the melting ice cube at a small scale.

If you take that same $100 and start investing it in an asset that grows at 7% per year on average (the long-term average return of a diversified stock portfolio), your $100 becomes roughly $197 in 10 years, $387 in 20 years, and $761 in 30 years.

The numbers are smaller than Saylor’s. The math is identical.

Saylor moved $250 million from a melting ice cube into a scarce asset. You can move $100 from a melting ice cube into a simple investment. The scale is different. The principle is the same.

That is why this article is in the Money Basics section of this site. Not because everyone should copy Saylor’s exact strategy. But because the rule he used, the Time Value of Money, is the single most important concept in personal finance, most people ignore it until it is too late.

If you want to understand this concept more deeply, I wrote a full breakdown in Time Value of Money for Beginners that explains it step by step without any jargon.

Three Takeaways You Can Use Today

1. Cash is a melting ice cube, not a safe haven.

Holding cash feels safe. In the short term, it is. But over the years and decades, inflation quietly erodes its value. This does not mean you should have zero cash. It means you should understand that cash is for short-term needs, not long-term wealth building. Anything you do not need for the next 6 to 12 months should be working for you, not sitting still.

2. Think in decades, not days.

Saylor did not panic when Bitcoin dropped 50% in a single week. He was thinking 10 years ahead. The same mindset applies to any long-term investment. Markets go up and down in the short term. Over 10 and 20 year periods, disciplined investors who hold quality assets have historically come out ahead. The Time Value of Money rewards patience.

3. The math does not require conviction. It requires action.

Most people understood intellectually that inflation was eroding their cash in 2020. Very few actually did anything about it. Saylor did. The difference between knowing a principle and applying it is the difference between watching wealth build and watching it melt. You do not need to be certain. You need to start.

Frequently Asked Questions

What is the “melting ice cube” concept in finance?

The melting ice cube is a metaphor for cash losing value over time due to inflation. Just as an ice cube slowly melts when left at room temperature, cash slowly loses its purchasing power when inflation outpaces the interest your savings earn. Michael Saylor used this concept to describe why holding $500 million in cash during a period of aggressive money printing was actually riskier than investing it.

Is Michael Saylor’s strategy only about Bitcoin?

No. The underlying principle is the Time Value of Money, which applies to all investing. Saylor chose Bitcoin because he believed it was the scarcest available asset during a period of rapid money printing. But the same principle (moving savings from depreciating containers into appreciating ones) applies to stocks, real estate, bonds, and other investment vehicles. The asset is the vehicle. The principle is the engine.

Can a regular person use the same rule as Michael Saylor?

Yes. The Time Value of Money works at any scale. Whether you invest $100 or $100 million, the math of compounding and purchasing power applies equally. The key is to move money you do not need in the short term out of cash and into assets that have the potential to grow faster than inflation over time.

Is holding cash always bad?

No. Cash is essential for short-term needs, emergency funds, and financial stability. The melting ice cube concept applies to long-term savings held in cash for years or decades. Financial experts generally recommend keeping 3 to 6 months of expenses in an accessible savings account. Beyond that, long-term savings benefit from being invested in assets that can outpace inflation.

What is the time value of money in simple terms?

The Time Value of Money means that a dollar today is worth more than a dollar in the future because today’s dollar can be invested and grow. It also means that a dollar in the future is worth less than a dollar today because inflation reduces what that future dollar can buy. This is the foundational concept behind all investing and the core principle Michael Saylor used to build his fortune.

Final Thoughts

Michael Saylor’s story is dramatic. A CEO staring at half a billion dollars in shrinking cash, making a bold move into an asset most people did not trust, and turning it into one of the largest corporate fortunes in modern history.

But the lesson underneath the drama is not dramatic at all. It is quiet, simple, and available to everyone.

Your cash is melting. Slowly. Quietly. Whether you have $500 million or $500. The question is not whether inflation is eroding your purchasing power. It is. The question is what you do about it.

You do not need to buy Bitcoin. You do not need to make a $250 million bet. You need to understand that money sitting still is money moving backwards, and then take even one small step to move it forward.

That is the rule. It works at $100. It works at $500 million. And it will keep working long after the headlines about Michael Saylor fade.

If you are just starting to think about this, my guides on compound interest, inflation, and how to start investing with just $100 are good places to begin.

The ice cube is melting. The only question is what you do next.

Leave a Reply