Simple explanations of everyday money concepts like compound interest, inflation, investing, and interest rates. No jargon, no fluff. Just the financial basics that help you make smarter decisions with your money over time.

If a country is struggling financially, why can’t it print more money and get rich?

It sounds like the simplest solution in the world.

No taxes. No debt. Just print and fix everything.

But every country that has tried this ended up making things worse. Much worse.

In this post, you’ll learn exactly why printing money doesn’t work, why printing money causes inflation, and what actually happens when governments print money without creating real value.

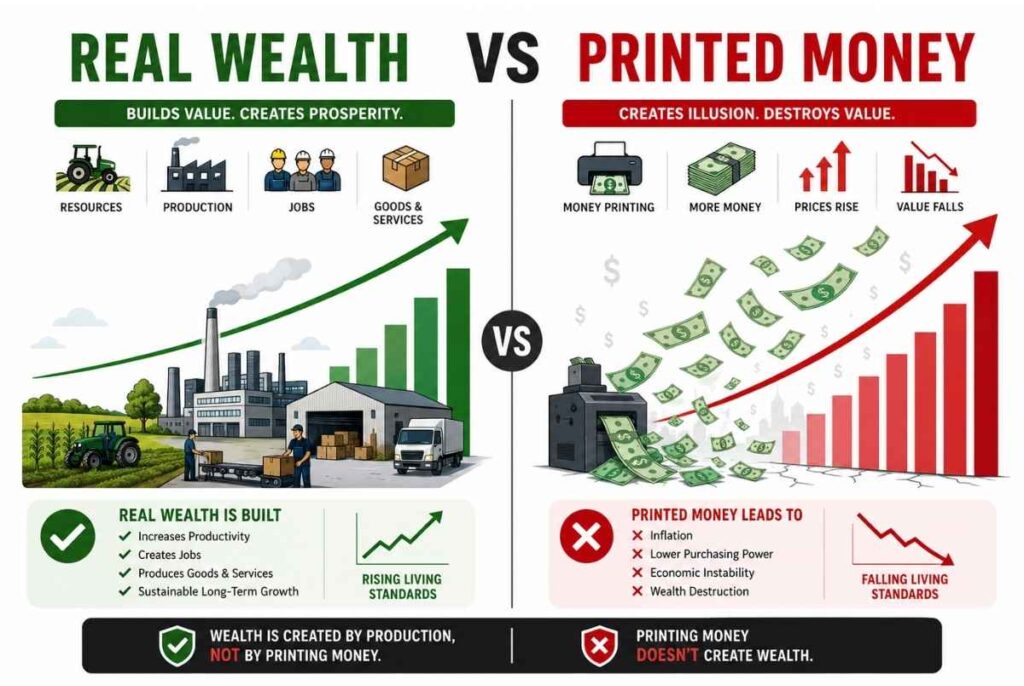

More Money Doesn’t Mean More Wealth

Here is the mistake most people make:

Money is not wealth. Money is just a way to measure wealth.

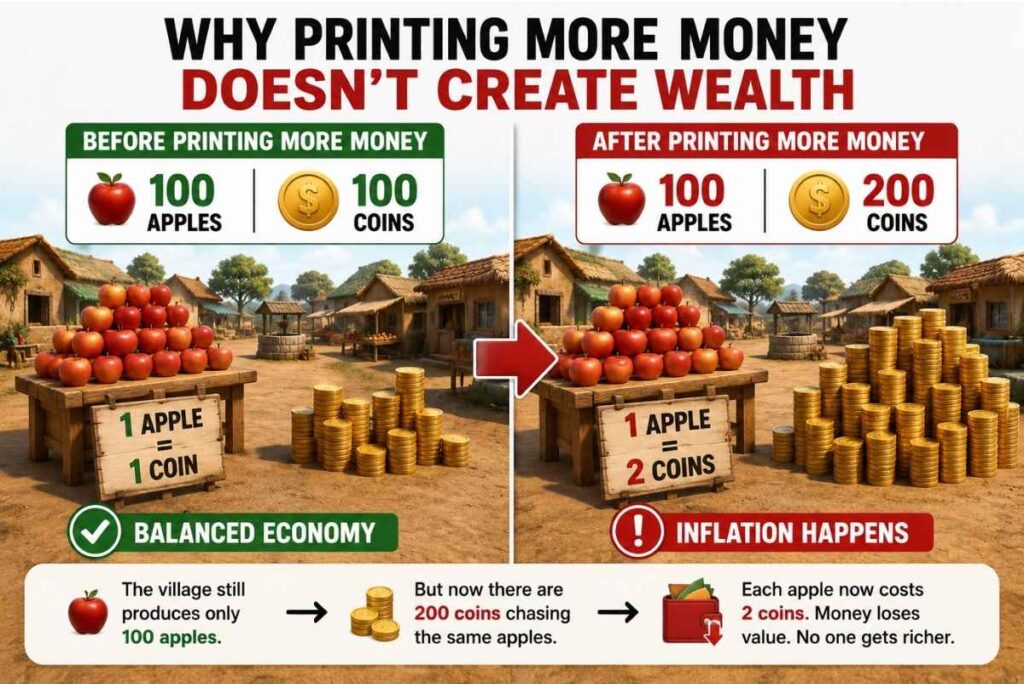

Imagine your entire country is a small village.

The village produces 100 apples. There are 100 coins in circulation. Each apple costs 1 coin.

Everything is balanced.

Now the government prints more money and adds 100 new coins into the system.

Did the village suddenly produce more apples? No.

There are still only 100 apples.

But now there are 200 coins chasing those same apples.

So what happens?

Each apple now costs 2 coins.

Nobody got richer.

The apples did not increase. Your money just lost value.

That is exactly why printing money causes inflation.

Printing money does not create wealth. It just spreads the same wealth across more pieces of paper.

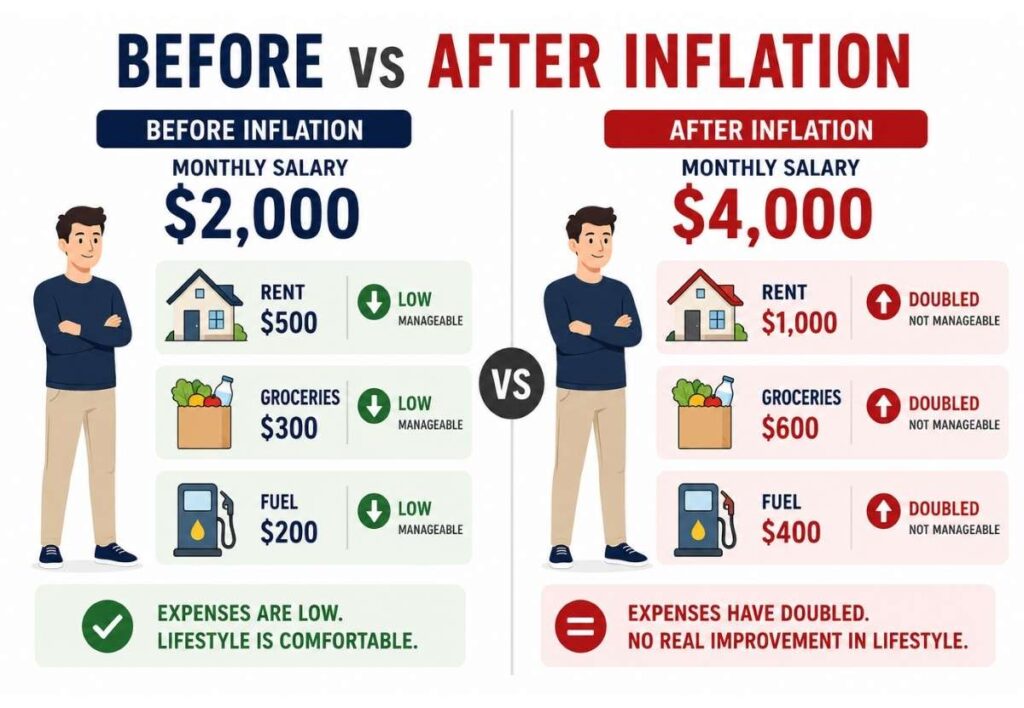

Your Salary Goes Up, but You Are Not Richer

Now let’s make it personal.

Imagine your salary doubles from 2,000 dollars to 4,000 dollars a month.

Sounds like a win.

But at the same time:

Your rent doubles Your groceries double Your fuel costs double

Suddenly, that extra money means nothing.

You are earning more. But you are not living better.

In reality, you are standing still.

And your savings?

They are quietly losing value while you watch your balance go up.

This is what happens when governments print money without increasing real production.

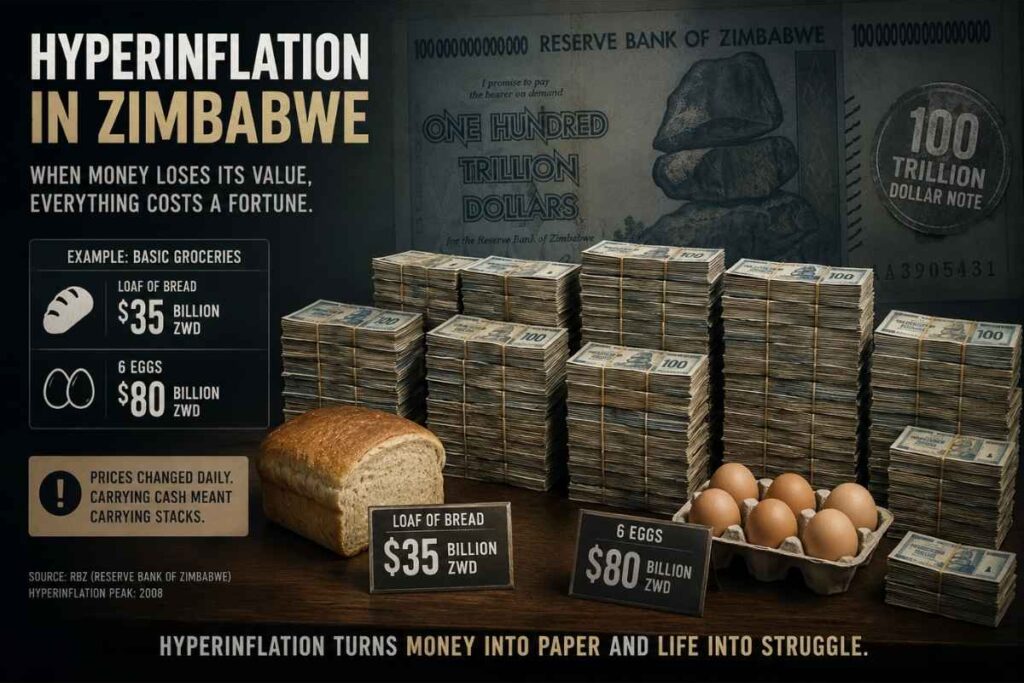

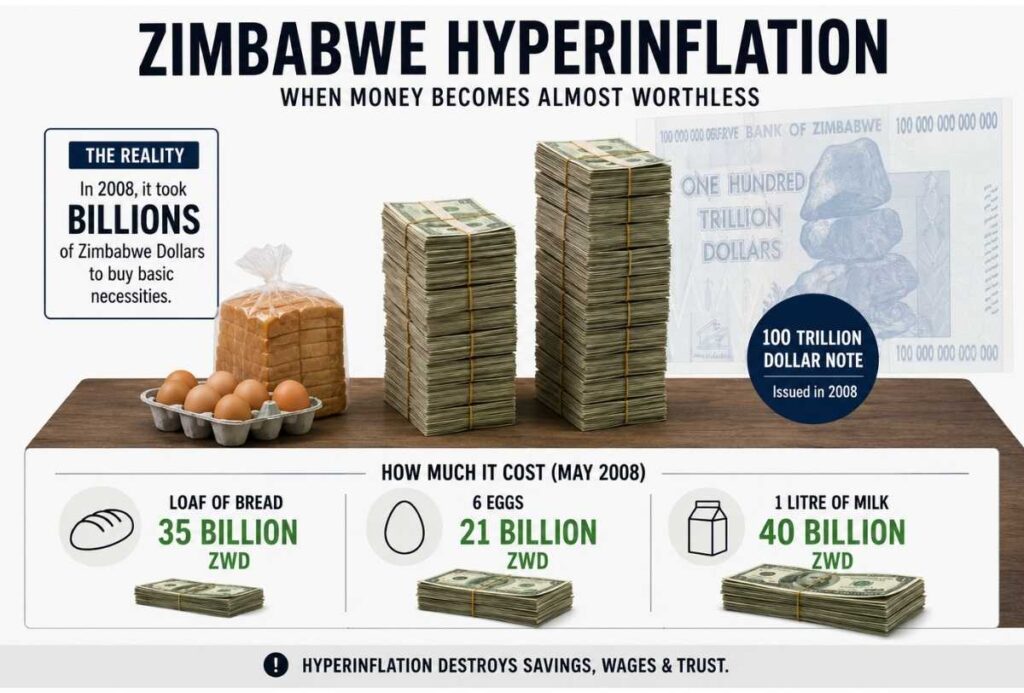

The Real World Proof: Zimbabwe

There is a real-world example that shows exactly what happens when countries print more money without control.

In the early 2000s, the government started printing money to pay its bills.

At first, it felt like a solution.

Then prices started rising.

So they printed more money.

Prices rose even faster.

They printed even more.

This cycle spiraled out of control.

By 2008, inflation reached 89.7 sextillion percent.

A single egg costs billions.

The government printed a 100 trillion dollar note.

And it still was not enough to buy basic groceries.

People needed stacks of cash just to buy bread.

Eventually, the currency became useless.

Zimbabwe had to abandon it completely.

This is what happens when money grows faster than real value.

So How Do Countries Actually Get Richer?

So if printing money doesn’t work, how do countries actually get rich?

There is only one real answer.

Production.

Countries get richer by creating more.

More goods More services More businesses More innovation

When there is more real value in the economy, then adding more money makes sense.

Without that, printing money only leads to inflation.

More money with the same goods leads to inflation More money with more goods leads to real growth

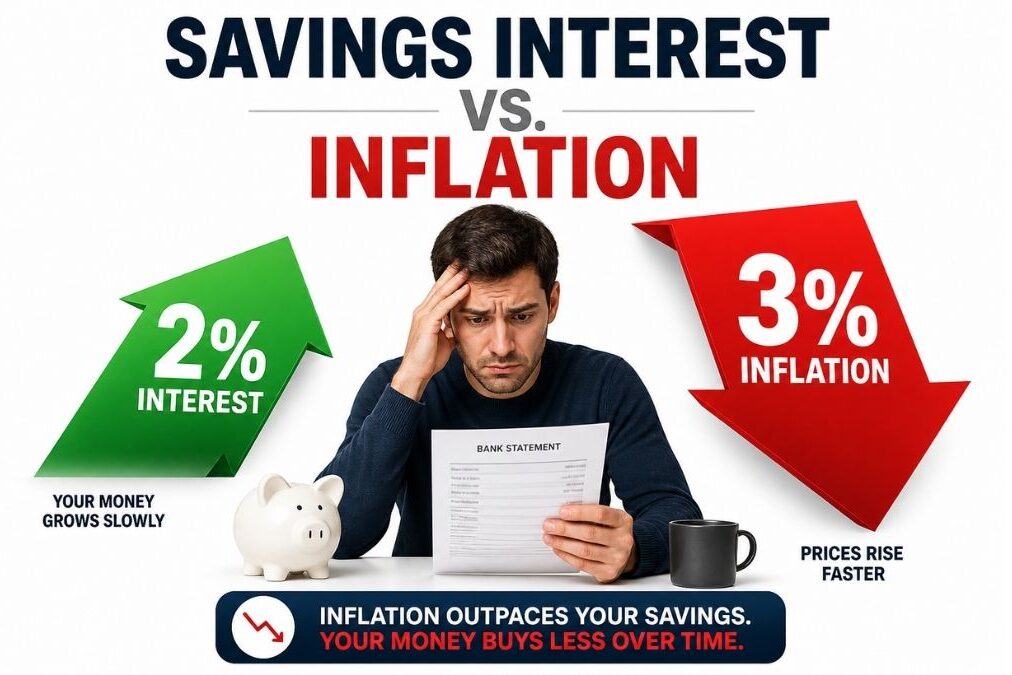

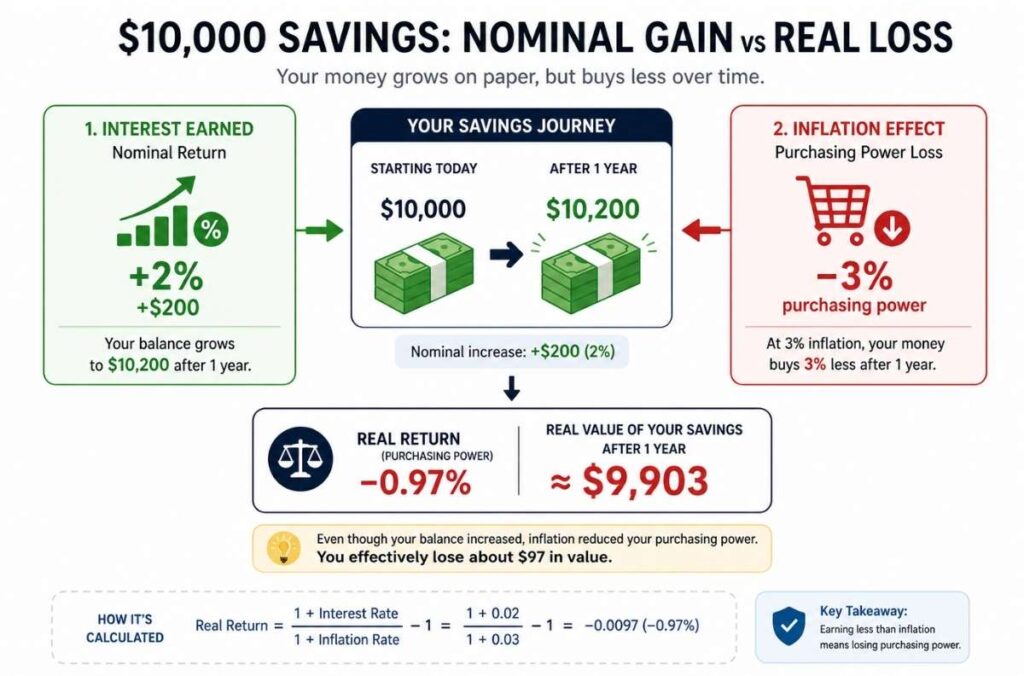

What This Means for Your Money

So what does this mean for you?

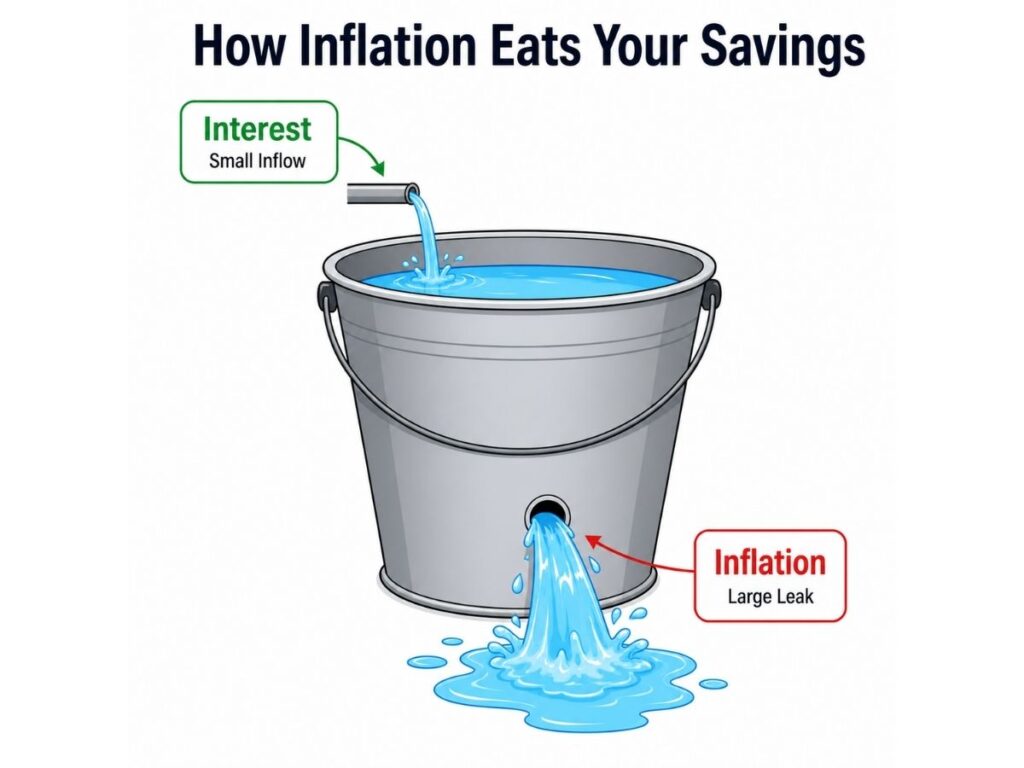

Every time excessive money printing happens, your savings take a hit.

Your balance does not change. But what it can buy slowly shrinks.

This is exactly why understanding money printing and inflation matters for your personal finances.

It is also why leaving your money sitting still during inflation is one of the most common and costly mistakes.

Understanding this is not just economics.

It is the difference between protecting your money and slowly losing it.

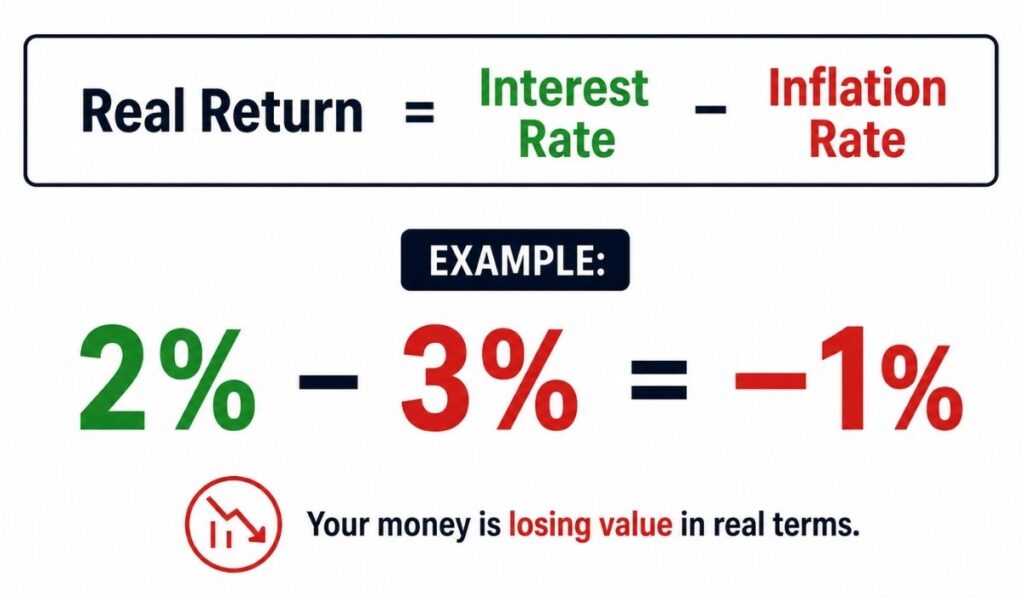

A dollar today is worth more than a dollar tomorrow.

But when inflation is higher than your interest rate?

Time is no longer helping you—it’s working against you.

A savings account was never designed to grow your wealth.

It was designed to protect your money,not multiply it. That’s valuable… but only for money you need in the short term. For everything else, a savings account is quietly working against you.

3 Moves to Stop Losing Money Right Now

Here’s the good news:

You don’t need to earn more money to fix this. You just need to put your money in better places.

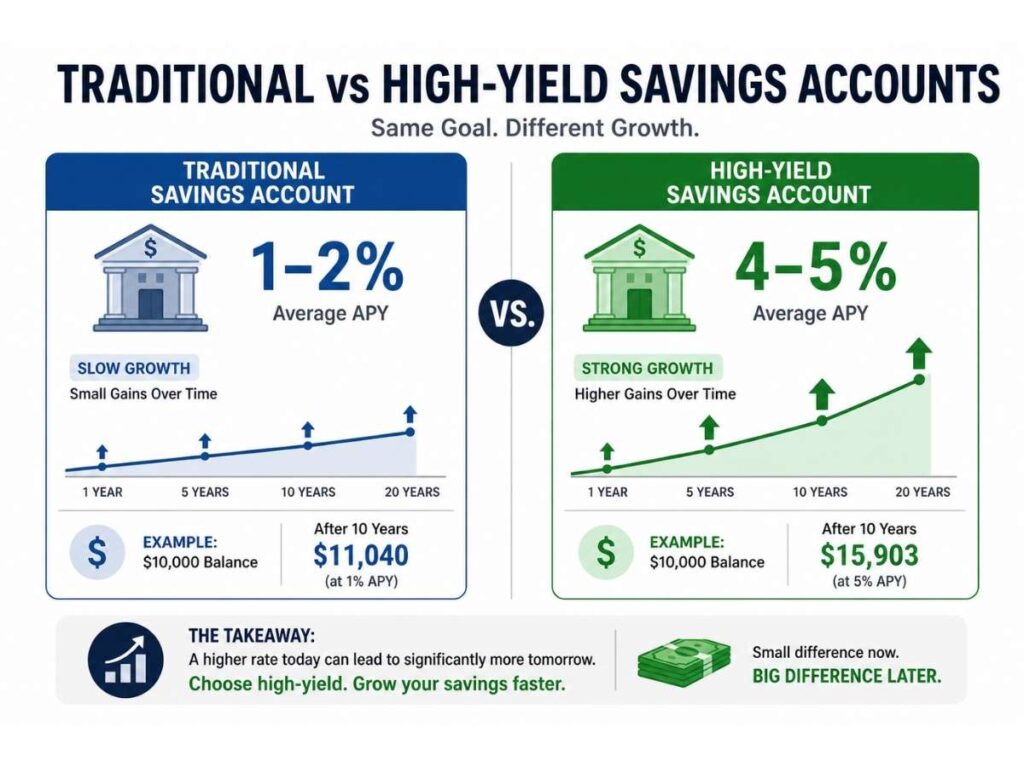

1. Switch to a High-Yield Savings Account (HYSA)

Some online banks are offering 4–5% interest right now—often 2–3x more than traditional banks.

That one move alone can turn your return from negative to positive without taking extra risk.

2. Look at I-Bonds for Money You Won’t Touch for a Year

I-Bonds are designed specifically for this problem.

Their interest rate adjusts with inflation—so your money keeps up instead of falling behind.

You can buy I-Bonds directly and safely through the U.S. Treasury’s official TreasuryDirect platform. The trade-off is that your money is locked in for a minimum of one year. But for a portion of your savings you don’t need immediately, they’re one of the safest inflation beaters available.

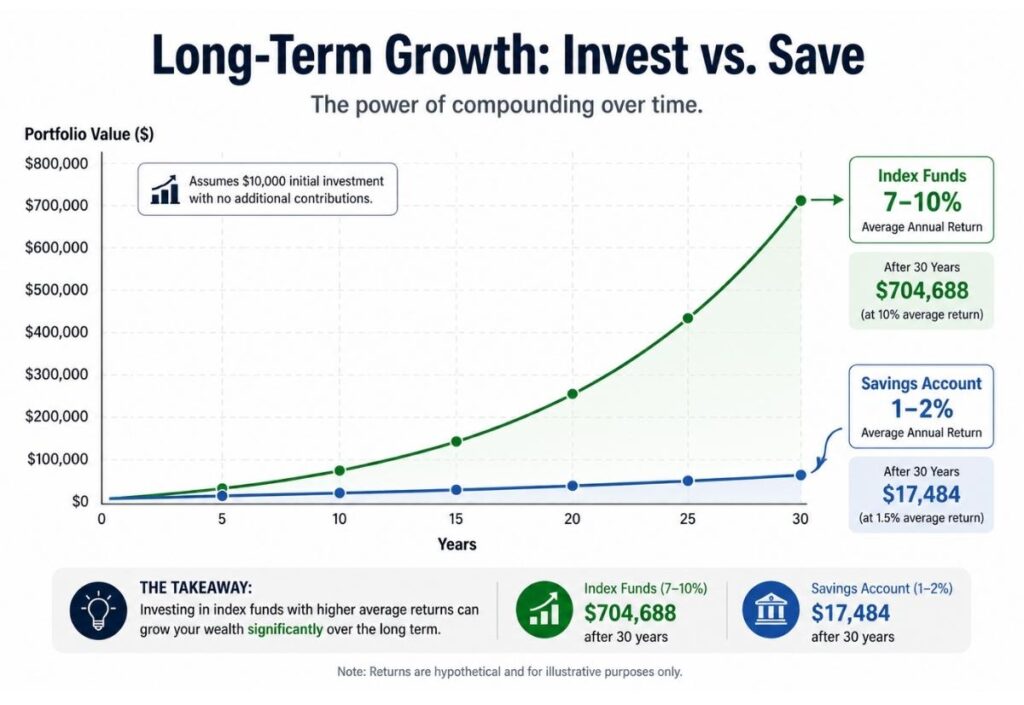

3. Consider Index Funds for Long-Term Money (5+ Years)

Over the long term, index funds have historically returned 7–10% per year.

That’s not just growth—it’s growth that beats inflation.

Short-term, they fluctuate. Long-term, they’ve consistently outpaced rising prices.

This is where understanding the difference between Stocks and Bonds becomes critical because index funds are built on stocks, and knowing what you own gives you the confidence to stay invested when markets get bumpy.

If you want to understand how your money compounds inside an index fund over time, our post on Compound Interest shows you exactly how the math works with real examples.

If you have money you genuinely won’t need for five or more years, leaving long-term money in a savings account is one of the most expensive financial mistakes you can make.

Your One Action for Today

Do this right now:

Open your savings account. Find your interest rate. Then check the current inflation rate.

Before we get to the list, let me make sure we’re speaking the same language, because “compound interest” gets thrown around a lot without anyone explaining why it actually matters.

Here’s the simple version: with regular (simple) interest, you earn returns only on your original deposit. With compound interest, you earn returns on your original deposit plus all the interest you’ve already earned.

It’s the difference between a snowball that melts a little every day and one that picks up more snow as it rolls downhill.

A quick example that hits differently when you see the math:

You invest $5,000 at 7% annual return.

Year 1: You earn $350. Balance: $5,350.

Year 2: You earn 7% on $5,350 — that’s $374. Balance: $5,724.

Year 10: Your balance is over $9,800 — without touching it.

Year 30: Your original $5,000 has grown to nearly $38,000.

You didn’t put in a single extra dollar after year one. Time did the work.

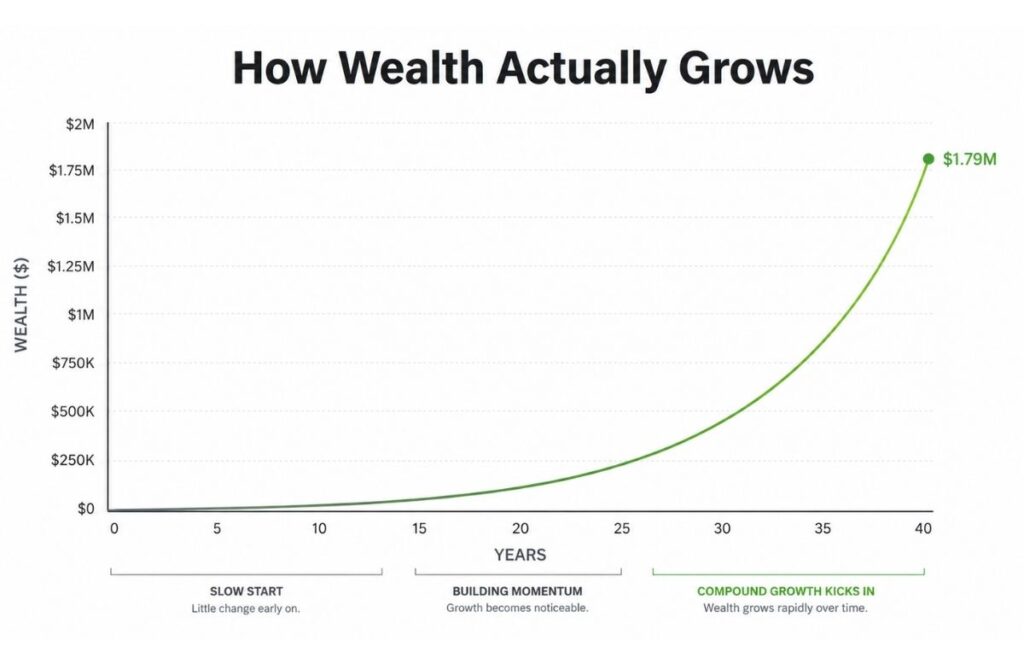

This is why starting early matters more than starting big. A 25-year-old investing $200/month will almost always end up richer than a 40-year-old investing $600/month — simply because compound interest needs time as its fuel.

Table of Contents

The Best Compound Interest Investments (Ranked From Beginner-Friendly to Advanced)

I’ve organized these by accessibility and risk so you can find your starting point quickly. If you’re new to investing, start with Section 1. If you already have the basics covered, scroll to Section 2.

Section 1: Best Compound Interest Accounts for Beginners (Start With What You Have)

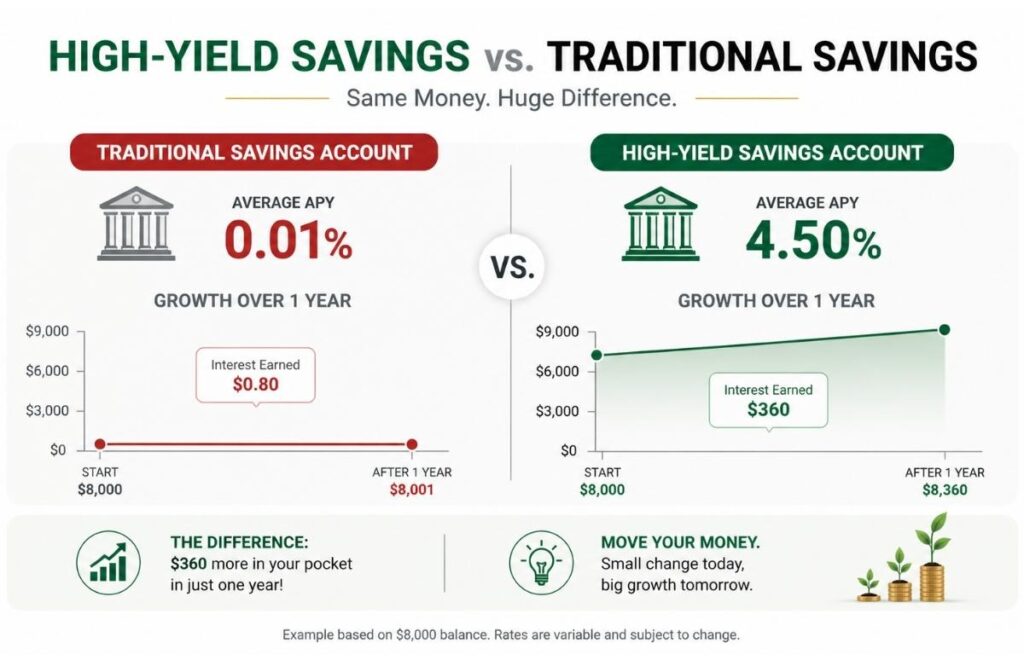

1. High-Yield Savings Accounts (HYSAs)

Best for: Anyone with cash sitting in a regular bank account earning next to nothing.

This is where most people should start — and where I started.

When I switched from a traditional bank savings account (earning 0.01% APY) to a high-yield savings account, my monthly interest went from pennies to real, meaningful dollars. In 2024, the best HYSAs were paying 4.5% to 5.0% APY — a staggering difference from what most big banks offer.

What makes them compound: Interest is calculated daily and added to your balance monthly. So every month, you’re earning interest on a slightly higher number than the month before.

Realistic case study: My friend Tariq kept $8,000 in a Chase savings account for two years, earning roughly $16 total. When he moved it to a high-yield account at 4.75% APY, he earned over $760 in the first year alone. Same money. Completely different result.

What to look for in a HYSA:

APY of 4.0% or higher (as of 2026)

No monthly fees or minimum balance requirements

FDIC insured (up to $250,000)

Easy online access and fast transfers

Quick note: Rates fluctuate with the Federal Reserve’s decisions. When the Fed cuts rates, HYSA rates typically follow. Don’t chase the single highest rate — look for a consistently competitive institution with no gotcha fees.

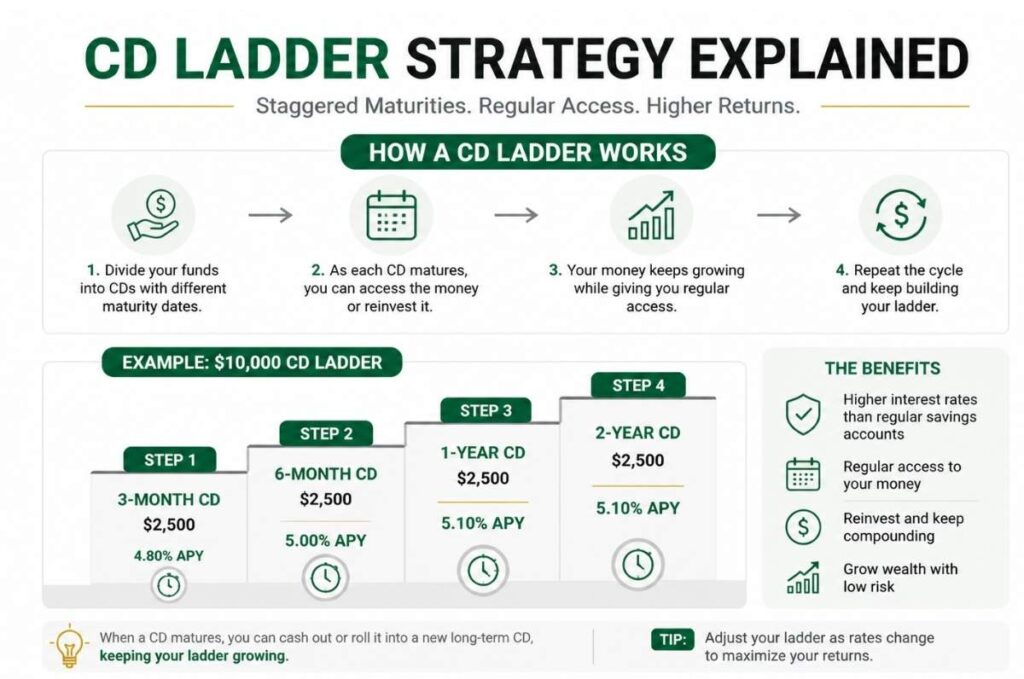

2. Certificates of Deposit (CDs)

Best for: Money you won’t need for 6 months to 5 years that you want to grow at a guaranteed rate.

CDs are essentially a deal you make with a bank: you promise to leave your money alone for a set period, and in return, they offer you a higher interest rate than a regular savings account.

The compounding here works the same way as HYSAs, but the rate is locked in — which can be great when rates are high and frustrating when they drop.

What I’d actually do: Consider a “CD ladder” — splitting your money across CDs with different maturity dates (3 months, 6 months, 1 year, 2 years). This gives you regular access to your money while still benefiting from higher rates on longer-term CDs.

Case Study — The $10,000 CD Ladder: A reader of mine (she asked to stay anonymous, so I’ll call her Priya) had $10,000 she wanted to keep safe but growing. She split it:

$2,500 in a 3-month CD at 4.8% APY

$2,500 in a 6-month CD at 5.0% APY

$2,500 in a 1-year CD at 5.1% APY

$2,500 in a 2-year CD at 4.9% APY

By the end of year one, she had earned approximately $482 in interest — and had access to her money in rolling 3-month windows. She felt none of the anxiety of having her savings “locked away” while still outperforming a regular savings account by a mile.

3. Money Market Accounts

Best for: People who want HYSA-level returns but with check-writing or debit access.

Money market accounts sit between a checking account and a savings account. They typically offer competitive interest rates with slightly more flexibility than a CD. The compounding works daily or monthly, depending on the institution.

They’re not dramatically better than HYSAs in most cases, but if you want to keep emergency funds accessible while still compounding them, a money market account is a sensible choice.

Section 2: Intermediate Compound Interest Investments (Where Real Wealth Is Built)

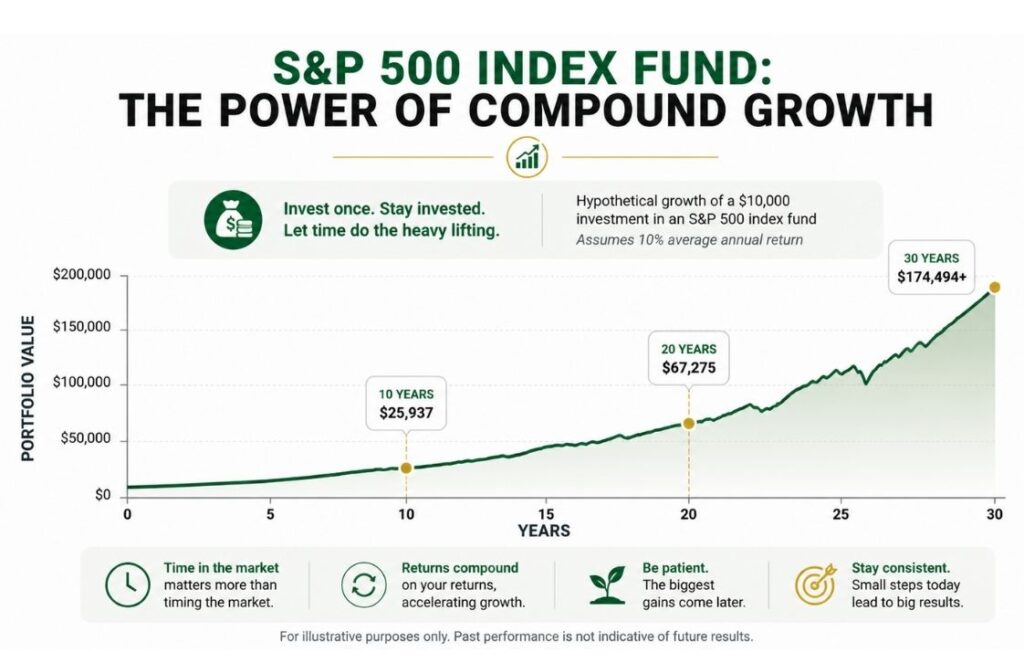

4. Index Funds and ETFs (The Compound Interest Powerhouse Most People Overlook)

Best for: Long-term investors who can leave money alone for 10+ years.

This is where the real compounding magic lives — and it’s also where most people make the mistake of looking for “better” options when this one is right in front of them.

An S&P 500 index fund — like those offered by Vanguard, Fidelity, or Schwab — tracks the 500 largest US companies. Historically, the S&P 500 has returned about 10% annually on average (roughly 7% after inflation).

That might not sound dramatic. Until you compound it.

$10,000 invested in an S&P 500 index fund:

After 10 years at 10% avg return: ~$25,937

After 20 years: ~$67,275

After 30 years: ~$174,494

Your original $10,000 becomes nearly $175,000 — without adding another cent.

Now add $200/month in contributions:

After 30 years: over $430,000.

This is not a hypothetical. This is the mathematical reality of compound growth over time.

My personal experience: I started investing in index funds in my mid-20s with $150/month. Not because I had a lot of money, but because I finally understood that waiting until I had “enough” to invest was the biggest mistake I could make. The time I’d lose by waiting was irreplaceable.

What makes this “compound interest”? Technically it’s compound growth (since stocks don’t pay a fixed interest rate), but the mechanism is identical — returns are reinvested, and you earn returns on your returns. Dividend reinvestment especially creates this compounding snowball effect.

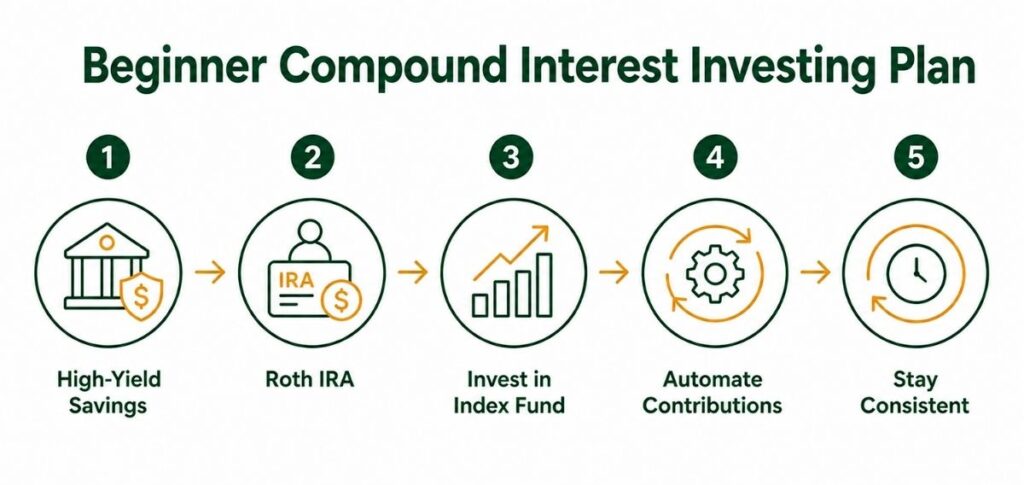

Key point for beginners: Use a tax-advantaged account. Maxing out a Roth IRA ($7,000/year in 2026) before investing in a taxable brokerage account is almost always the right move. Growth inside a Roth IRA is 100% tax-free in retirement.

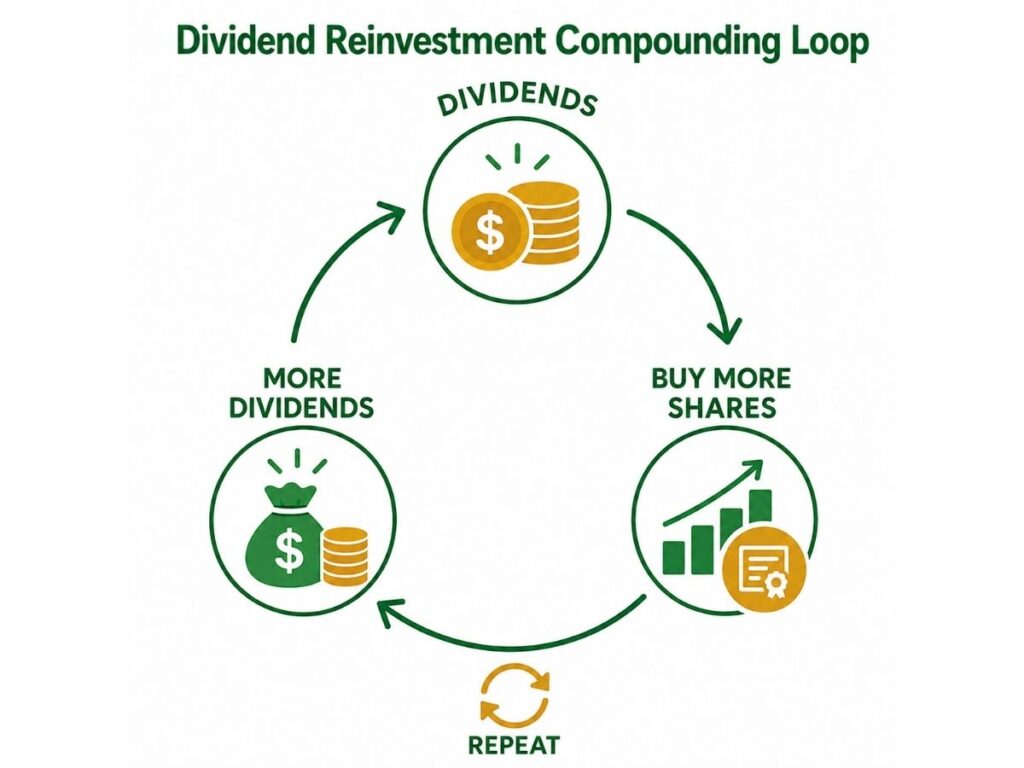

5. Dividend Reinvestment (DRIP)

Best for: Investors who own dividend-paying stocks or ETFs and want their income to work harder automatically.

Dividend reinvestment means that instead of taking your dividend payments as cash, you automatically use them to buy more shares of the same stock or fund. Those new shares then generate their own dividends, which buy more shares, generating more dividends.

Sound familiar? That’s compounding.

A simple illustration: Imagine you own 100 shares of a dividend ETF worth $50/share. The fund pays a 3% annual dividend. That’s $150/year. If you reinvest those dividends, you now own 103 shares. Next year, your dividends will be slightly higher. The year after, higher still.

Over 20 or 30 years, this becomes a meaningful difference — studies show DRIP investors can accumulate 30–40% more wealth than those who take dividends as cash.

Most brokerages allow you to set up automatic dividend reinvestment for free. It takes about 90 seconds to turn on and then runs itself.

6. Real Estate Investment Trusts (REITs)

Best for: Investors who want real estate exposure without becoming a landlord.

REITs are companies that own income-producing real estate, apartment buildings, hospitals, data centers, and shopping centers. They’re legally required to distribute at least 90% of their taxable income to shareholders as dividends.

That makes them high-yield dividend payers — which, when reinvested, compound powerfully.

What I like about REITs:

Accessible with as little as the price of one share (some are under $30)

You get real estate diversification without the headaches of property management

Publicly traded REITs can be bought and sold like any stock

What to watch out for:

REITs are sensitive to interest rate changes (when rates rise, REIT prices often fall)

Not all REITs are created equal — do your homework on occupancy rates, debt levels, and dividend history before buying

Case study: A colleague of mine started buying a diversified REIT ETF in 2018 with $300/month. By 2024, between price appreciation and reinvested dividends, his position had grown to roughly $32,000 from approximately $19,200 in contributions. That gap, $12,800, was compound growth doing its job.

Section 3: Advanced Options (For When You’re Ready to Go Further)

7. Bonds and Bond Funds (Stability with Compound Income)

Best for: Investors closer to retirement or anyone wanting to reduce portfolio volatility.

Individual bonds pay interest at fixed intervals, but bond funds automatically reinvest that interest — creating compound growth. Treasury bonds, corporate bonds, and municipal bonds each carry different risk/reward profiles.

In a balanced portfolio (say, 70% stocks / 30% bonds), the bond portion helps smooth out the turbulent years while still compounding quietly in the background.

8. I-Bonds (Inflation-Protected Compound Growth)

Best for: Money you want protected against inflation for 1–5 years.

Series I Savings Bonds are US government bonds that earn interest tied to the inflation rate. When inflation was running hot in 2022, I-Bonds were paying over 9% — attracting enormous attention from personal finance writers and savers alike.

The interest compounds every six months and is added to the bond’s principal, which then earns future interest. There are purchase limits ($10,000/year per person electronically) and you must hold them for at least 12 months.

They’re not a long-term wealth-builder on their own, but as a portion of your emergency fund or short-term savings, they’re a smart hedge.

9. Farmland and Alternative Assets (For Accredited Investors)

Best for: High-net-worth investors looking for portfolio diversification and inflation hedging.

Farmland has historically generated consistent returns — since 1990, US farmland has delivered average annual returns north of 10%, driven by both land appreciation and rental income from farmers.

Platforms like AcreTrader and FarmTogether allow accredited investors to purchase fractional interests in farmland. The income compounds as rental payments are reinvested.

Important caveat: These platforms are for accredited investors (generally those with $200K+ annual income or $1M+ net worth excluding primary residence). They’re also illiquid; you can’t sell them tomorrow if you need cash. Approach with eyes open.

How to Start: A Beginner’s Compound Interest Playbook

If you’re reading this and thinking “okay, but where do I actually begin?”, here’s what I’d do if I were starting over today with $500:

Open a high-yield savings account. Move your emergency fund (3–6 months of expenses) here. Let it compound while you build other investments.

Open a Roth IRA. Contribute what you can — even $50/month matters more than you think. Invest it in a low-cost S&P 500 index fund.

Turn on DRIP. If your brokerage account holds any dividend-paying fund or stock, turn on automatic dividend reinvestment immediately. It’s free and automatic.

Automate everything. The biggest enemy of compound interest is you dipping into your investments when life gets messy. Automating contributions removes the temptation.

Leave it alone. Seriously. The hardest part of compound investing isn’t finding the right account. It’s resisting the urge to pull money out during market dips or when a shiny new investment opportunity comes along.

The math is patient. You just have to be too.

Frequently Asked Questions FAQs

What’s the best compound interest investment for beginners?

A high-yield savings account for your emergency fund, and a Roth IRA invested in an S&P 500 index fund for long-term growth. These two together cover 80% of what most people need to start building wealth.

How much money do I need to start earning compound interest?

Far less than you think. Many high-yield savings accounts have no minimum balance. Index fund ETFs can be purchased for the price of a single share, some brokerages even allow fractional shares. You can literally start with $1.

How often does compound interest compound?

It depends on the account. Savings accounts and money market accounts typically compound daily and credit monthly. Index funds compound continuously as share prices rise and dividends are reinvested. CDs vary; read the terms before opening one.

Is compound interest better in a Roth IRA or a regular brokerage account?

A Roth IRA is almost always better if you qualify, because growth is tax-free. In a regular brokerage account, you pay capital gains taxes when you sell, which chips away at your compounded returns over time. Max your Roth IRA first ($7,000/year in 2026 if you’re under 50).

What kills compound interest?

Three things: withdrawing money early (you lose future compounding on everything you take out), fees (even 1% annual fees quietly eat 20–30% of your long-term returns), and inflation (if your savings account pays 0.5% and inflation is 3%, your money is actually shrinking in real terms).

How long does it take to see real results from compound interest?

This is the question nobody likes the honest answer to: it takes years. The first decade often feels slow. The second decade feels faster. The third decade is when people start calling it “magic.” The best time to start was yesterday. The second-best time is right now.

Can compound interest make you a millionaire?

Yes — with consistency, time, and patience. A 22-year-old who invests $400/month in an index fund averaging 8% annually would have over $1.5 million by age 62. That’s not a fantasy. That’s math.

The Bottom Line: Compound Interest Is Slow, Patient, and Quietly Powerful

Here’s the truth about compound interest that financial influencers rarely say out loud: it’s boring.

The best compound interest investment strategy isn’t a flashy app, a hot new alternative asset, or a product someone is getting paid to recommend. It’s opening the right accounts, automating your contributions, choosing low-fee investments, and then having the patience to leave everything alone for years at a time.

The readers I’ve seen build real, lasting wealth aren’t the ones who found the highest yield in a given month. They’re the ones who started earlier than most people, contributed consistently even when life was hard, and resisted the urge to do something clever when the market got scary.

You don’t need a PhD in economics to build wealth. You just need to understand how compound interest works, pick a few sensible vehicles for it, and get out of your own way.

If this article helped you, share it with someone who’s still keeping their savings in a 0.01% account. They’ll thank you in 10 years.

Money Cornucopia simplifies complex personal finance into easy, actionable steps. Nothing in this article constitutes personalized financial advice. Always consider your personal circumstances and consult a financial professional before making investment decisions.

Yesterday in Omaha, Nebraska, something historic happened.

Tens of thousands of people showed up before midnight, sleeping outside an arena in the cold, just to get a seat inside. Not for a concert. Not for a sports final. For a company’s annual shareholders meeting.

That is the kind of man Warren Buffett is. At 95 years old, having handed the CEO role of Berkshire Hathaway to Greg Abel at the start of this year, Buffett sat in the audience yesterday as an observer for the first time in six decades. No longer the one running the show. Just a man watching what he built; carry on without him.

And when Abel raised Buffett’s jersey to the rafters with the number 60 on it, one for each year Buffett served as CEO, the room erupted in applause. The jersey now hangs permanently alongside the late Charlie Munger’s, numbered 45 for his own tenure. A can of Cherry Coke, Buffett’s favorite drink, sat on the table next to Abel’s notes.

It was, as one long-time attendee put it, “a flawlessly executed handoff.”

Who Is Warren Buffett and Why Should a Beginner Care?

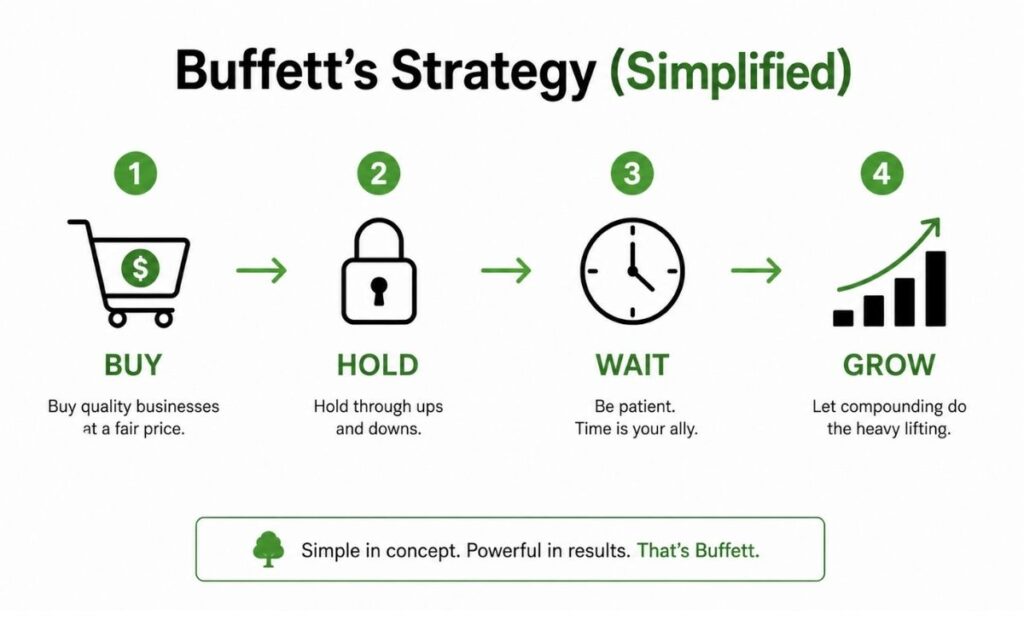

If you are new to investing, here is all you need to know. Buffett started investing at age 11 with $114. He is now worth over $150 billion. And he did it almost entirely through one strategy that anyone can understand, and anyone can copy.

He bought great businesses and held them. For decades. Without panicking. Without chasing trends. Without doing anything clever.

That is it. That is the whole secret.

While everyone else was jumping in and out of markets, timing crashes, picking hot stocks, and following tips from their cousin, Buffett just kept buying and holding. Compound interest did the rest.

The same compound interest we talk about regularly right here at Money Cornucopia.

Not a word about stock picks. Not a word about market timing. Not a word about being the smartest person in the room.

Just patience. Just trust. Just long-term thinking.

That is the lesson. And it is devastatingly simple.

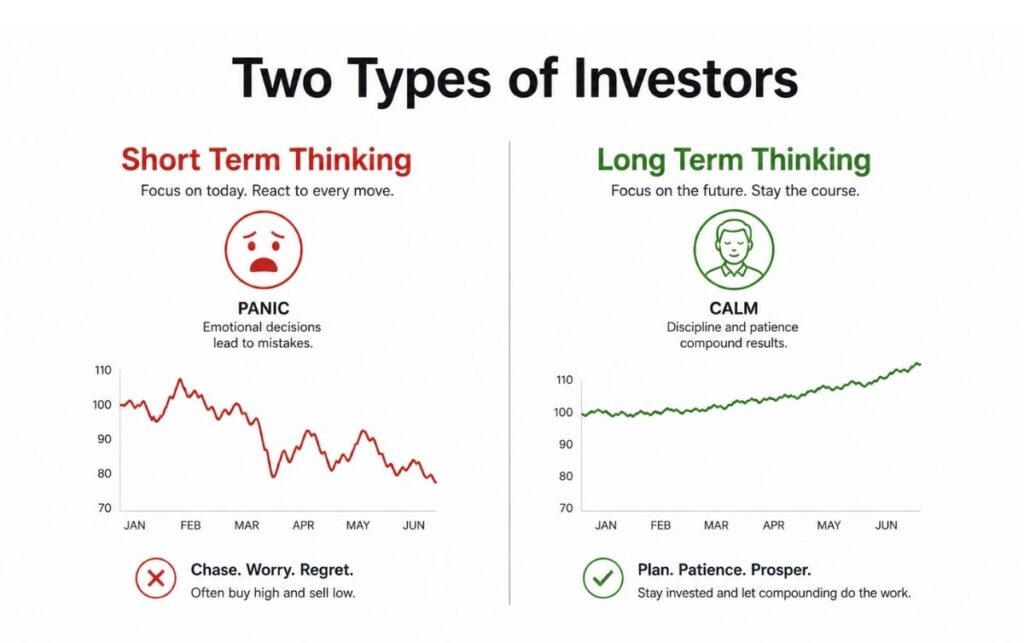

Most beginners approach investing like they are trying to win a sprint. They want returns this month, this quarter, this year. They check their portfolio every day. They panic when markets dip. They sell when things get scary. They are playing an entirely different game from the one Buffett played for 60 years.

Buffett played the long game so consistently and so stubbornly that he became the greatest investor in human history doing it. Not because he was smarter than everyone else. Because he was more patient than everyone else.

Patience is free. It costs nothing. And it is the one thing that separates people who build wealth from people who just talk about it.

What This Means for You Today

You do not need $150 billion to apply this lesson. You need $50 a month and the discipline to leave it alone.

Start investing in a low-cost index fund. Set it to automatic. Stop checking it every day. Let it compound for 20 years. Then look at what happened.

That is Buffett’s actual strategy stripped down to its beginner form. Everything else is noise.

The man just handed over the most successful investment empire in history at 95 years old. He did not do it by being clever. He did it by being consistent.

You can be consistent too. That is entirely within your control starting today.

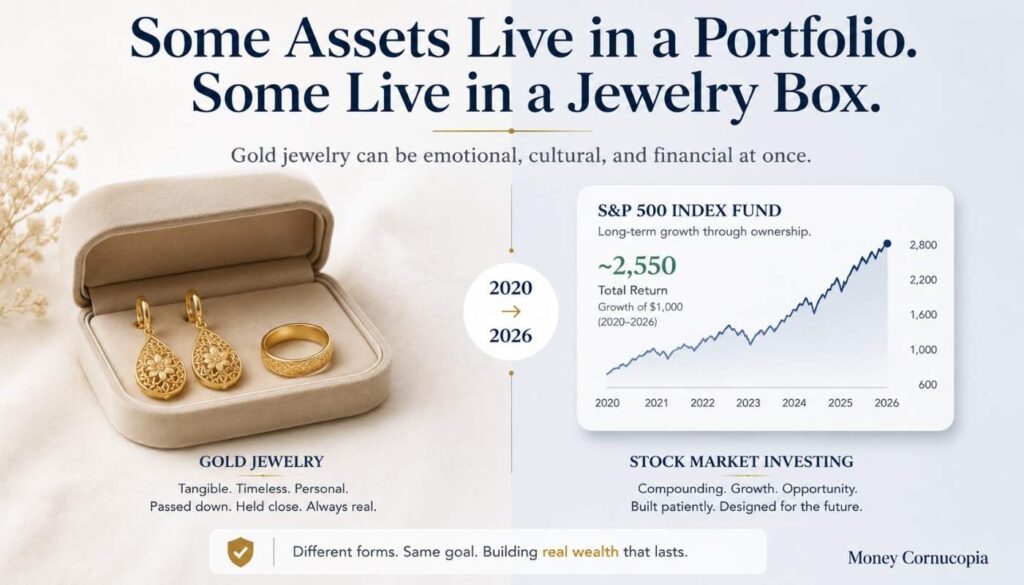

In 2020, I walked into a jewelry shop and bought my wife a pair of gold earrings and a ring. The total came to a little over $1,000.

I was not thinking about portfolio allocation or hedge strategies. I was thinking about two things. First, my wife would love them. Second, my family had always told me that gold is never a bad place to put your money.

Six years later, that $1,000 in gold is worth roughly $2,500.

But here is the part that surprised me. When I ran the numbers on what would have happened if I had put that same $1,000 into the stock market instead, the result was almost identical. Stocks returned nearly the same amount over the same period.

And the savings account? That is where the real story is. The $1,000 I could have left in savings barely grew at all. Once you factor in the inflation that followed 2020, especially the sharp price increases in 2021 and 2022, that money likely buys less today than the original $1,000 bought six years ago.

So I did the full math on all three. Here is what I found.

Table of Contents

The Real Numbers: $1,000 in Gold vs Stocks vs Savings (2020 to 2026)

This is not a hypothetical. These are real returns based on verified market data.

Gold averaged roughly $1,770 per ounce in 2020. As of May 2026, gold is trading at approximately $4,520 per ounce. The S&P 500 started 2020 at roughly 3,258 and sits at approximately 7,470 in May 2026. A standard savings account averaged roughly 2% interest per year over this period.

Where $1,000 went in 2020

Approximate value in May 2026

Total return

Gold (at 2020 average price)

~$2,500 to ~$2,550

~150% to ~155%

S&P 500 (total return with dividends reinvested)

~$2,550

~155%

S&P 500 (price return only, no dividends)

~$2,300

~129%

Savings account (average 2% interest)

~$1,125

~12.6%

Read that table carefully. Gold and stocks performed almost identically over this 6-year period. Depending on which exact date you bought and whether you count reinvested dividends, either one could have slightly won. The gap is so small it is essentially a tie.

The massive gap is not between gold and stocks. The massive gap is between investing and not investing.

$1,000 that was invested (in either gold or stocks) became roughly $2,500. $1,000 that was left in a savings account became $1,125. The savings account produced less than one-tenth of the return that gold or stocks produced. And once you factor in the inflation that followed 2020, especially the sharp price increases in 2021 and 2022, that $1,125 likely buys less today than the original $1,000 bought in 2020.

The savings account did not just underperform. It quietly lost purchasing power while looking like it was growing.

That is the finding most people miss.

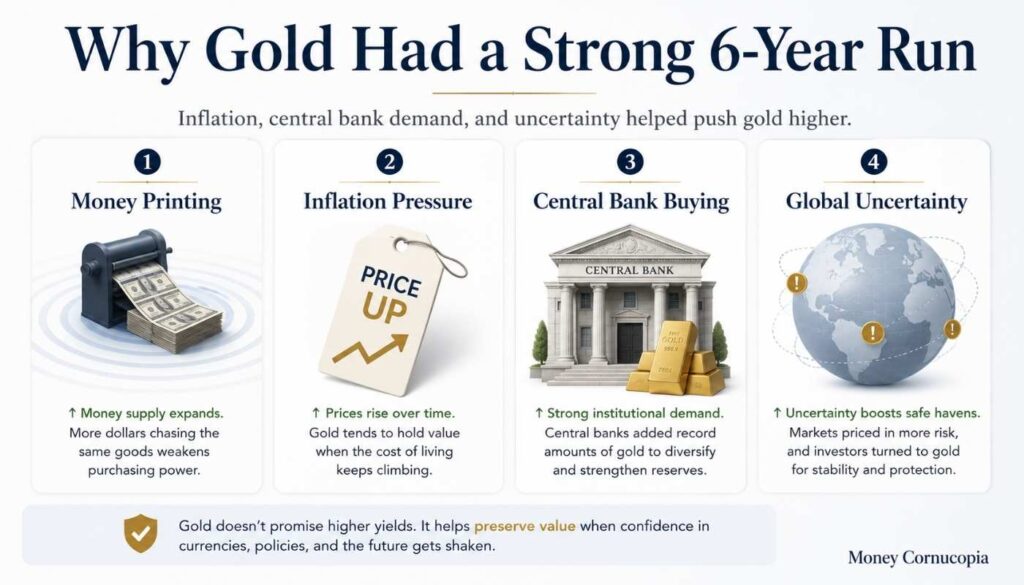

Why Gold Performed So Well From 2020 to 2026

Gold does not always match stocks. But this period was almost perfectly designed for gold to shine.

Several forces aligned at the same time to drive gold prices from roughly $1,770 per ounce in 2020 to over $4,500 per ounce by May 2026.

Massive Money Printing

In 2020, governments around the world printed trillions of dollars to keep economies alive during the pandemic. When more money floods the system, each dollar becomes worth less. Gold, which has a fixed supply that cannot be printed, becomes relatively more valuable. This is the same “melting ice cube” concept I covered in my article on Michael Saylor’s wealth strategy. Cash was melting. Gold was not.

Persistent Inflation

Inflation rose sharply after 2020 and has remained elevated into 2026. When inflation runs higher than the interest rate on your savings account, your cash is quietly losing purchasing power. Gold historically holds value during inflationary periods because its supply cannot be inflated away.

Central Banks Buying Gold at Record Levels

Central banks around the world, particularly in China, Poland, and India, have been buying gold at record levels. According to J.P. Morgan’s gold research, combined central bank and investor demand is expected to average roughly 585 tonnes per quarter in 2026. When the biggest financial institutions in the world are buying, the price tends to rise.

Geopolitical Uncertainty

Wars, trade tensions, and political instability have pushed investors toward safe-haven assets. Gold has been considered a safe haven for centuries, and in times of global uncertainty, demand spikes.

Why Stocks Also Performed Well (And Why They Usually Do)

The S&P 500 returned roughly 129% in price gains and roughly 155% in total return over the same period.

That is a genuinely impressive result. Including reinvested dividends lifts the rough return from about 129% to about 155%, a difference of around 26 percentage points. Over longer periods of 20 to 30 years, stocks have historically returned roughly 7 to 10% per year on average, which tends to outpace gold’s long-term average.

Stocks also have one advantage gold never will: they pay dividends. When you own stocks through an index fund, the companies inside that fund pay you a share of their profits regularly. Over the 2020 to 2026 period, those reinvested dividends were the reason stocks slightly edged ahead of gold in total return.

Gold pays nothing. It just sits there, holding value but not generating cash.

Here is the honest comparison:

Factor

Gold

Stocks (S&P 500)

Savings account

2020 to 2026 return

~150% to ~155%

~155% (with dividends)

~12.6%

Long term historical average

~5 to 7% per year

~7 to 10% per year

~1 to 3% per year

Pays dividends or interest

No

Yes (dividends)

Yes (interest)

Protects against inflation

Historically yes

Historically yes (long term)

Often no

Volatility

Moderate

High

Very low

That last row is not entirely a joke. It is genuinely part of why I bought gold as jewelry instead of a gold ETF.

The Honest Downsides of Gold (That Most Articles Will Not Tell You)

Every competing article I read while researching this piece was quietly selling gold. I am not selling anything, so I can be honest about the downsides.

Gold Does Not Generate Income

Stocks pay dividends. Savings accounts pay interest. Bonds pay coupons. Gold just sits there. Over the 2020 to 2026 period, reinvested dividends were the reason stocks slightly edged out gold in total return. If you need your investments to produce cash flow, gold alone will not do that.

Gold Jewelry Has a Hidden Cost

This is important for anyone considering my approach. When you buy gold as jewelry, you pay a “making charge” on top of the gold value. This premium covers the craftsmanship, design, and profit margin for the jeweler. Depending on where you buy, this can add 10 to 25% to the price.

When you sell gold jewelry, you typically get the gold value back, not the making charge. So on day one, your jewelry is worth less than what you paid. Over time, if gold appreciates enough (as it did from 2020 to 2026), the growth more than covers the making charge. But in the short term, you are starting at a small loss.

This is an honest disclosure that most “invest in gold” articles skip because they do not want to discourage you from buying.

Gold Can Drop Sharply

Gold hit an all-time high of roughly $5,600 in January 2026 and then dropped approximately 20% to around $4,500 by May 2026. That is a significant short-term decline. If you had bought at the January peak and needed to sell in May, you would have lost roughly one-fifth of your investment.

Gold is less volatile than stocks on average, but it is not risk-free.

Storage and Security

If you buy physical gold (bars, coins, or jewelry), you need to keep it safe. For jewelry, that usually means wearing it or keeping it in a secure location. For gold bars, you might need a bank safety deposit box or a home safe.

Gold ETFs solve this problem because they are digital, but then you lose the tangible, dual-purpose benefit that jewelry provides.

The Part Nobody Talks About: Why I Bought Gold as Jewelry

Most English-language investing guides treat gold as a ticker symbol. For my family, gold means something different.

I did not buy gold because a YouTube guru told me to. I bought it because my family has always treated gold as a financial tradition. Gifting gold jewelry to your wife is not just an expression of love. It is a way of building family wealth that has worked across generations.

The gold earrings and ring I bought my wife in 2020 serve two purposes that no ETF can match. First, my wife wears them and enjoys them. Second, they have appreciated in value from roughly $1,000 to roughly $2,500.

In many cultures across South Asia, the Middle East, and beyond, gold jewelry is not a “fun accessory.” It is the family’s financial safety net. It is what your grandmother gave your mother. It is the asset your family falls back on in an emergency. It is portable, universally valued, and does not require a bank account or brokerage.

When my family advised me to buy gold, they were not giving me a stock tip. They were sharing generational financial wisdom. The same gold that protected their wealth through economic crises, currency devaluations, and political instability is now protecting mine.

This perspective is almost completely absent from Western financial media. And yet it applies to hundreds of millions of people reading about gold investing in English right now.

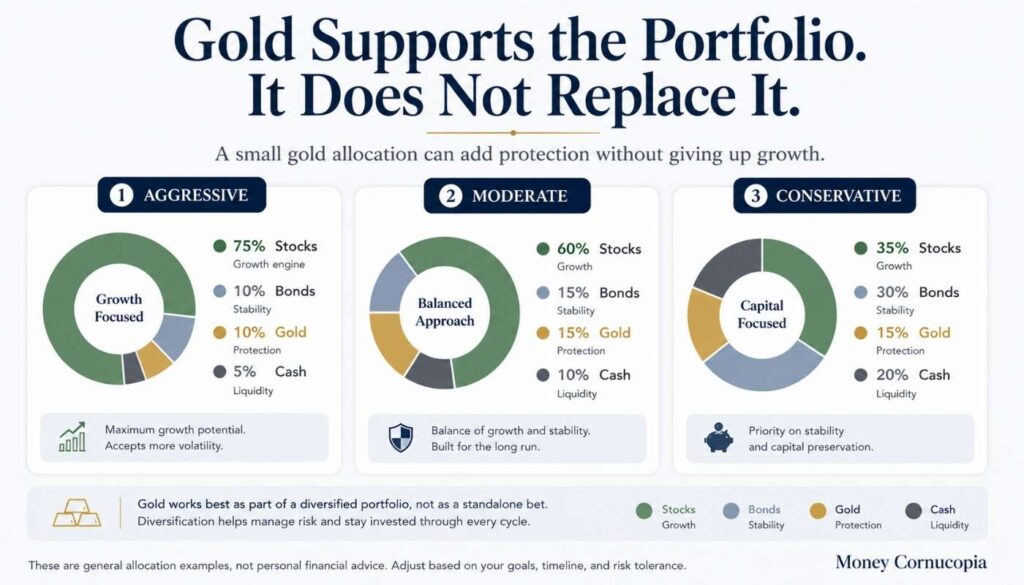

Where Gold Actually Fits in Your Portfolio

Gold is not an entire investment strategy. It is one piece of a larger plan.

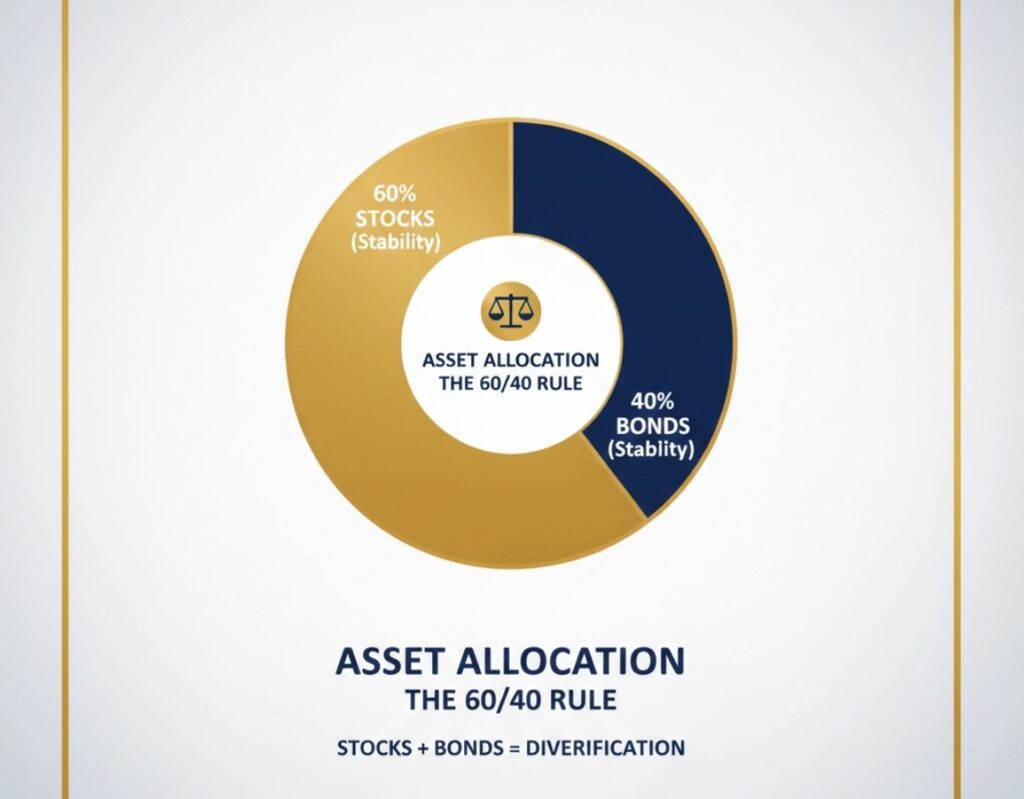

In my article on asset allocation and diversification, I explained how spreading your money across different types of investments protects you from any single one failing. Gold is one of those types.

Most financial experts suggest keeping 5 to 15% of your portfolio in gold or precious metals. Not 100%. Not 50%. A slice that provides protection without sacrificing the growth potential of stocks.

Here is a simple framework for a beginner:

Risk profile

Stocks

Bonds

Gold

Cash

Aggressive (20+ year horizon)

75%

10%

10%

5%

Moderate (10 to 20 years)

60%

15%

15%

10%

Conservative (under 10 years)

35%

30%

15%

20%

Gold never dominates the portfolio. It supports it. This connects to the risk-return tradeoff that every investor needs to understand. Higher potential returns come with higher risk. Gold sits in the middle, offering moderate returns with moderate volatility.

What I Would Tell a Beginner With $500

If someone asked me, “Should I put my money in gold, stocks, or savings?” here is my honest answer.

Do not put all of it into any one option.

Put $300 into a low-cost stock index fund. This is the growth engine. Over 10 to 20 years, it has the highest expected return and pays dividends along the way. You can start investing with as little as $100.

Put $100 into gold, whatever form makes sense for your situation. Physical gold if you value the tangible asset and the cultural significance. A gold ETF if you want convenience and lower premiums.

Keep $100 in a savings account as an emergency buffer. Not for growth. For peace of mind.

The 2020 to 2026 data proves the core principle: it barely mattered whether you chose gold or stocks. What mattered was whether you invested at all. The person who put $1,000 into either gold or stocks has roughly $2,500 today. The person who left it in savings has $1,125 and falling purchasing power.

The enemy is not choosing the wrong investment. The enemy is not investing at all.

Different Ways to Invest in Gold

Physical Gold (Jewelry, Coins, Bars)

This is the traditional approach and the one I took. You buy tangible gold that you can hold, wear, or store. The upside is ownership you can see and touch. The downside is the making charge on jewelry and the need for secure storage.

Gold ETFs (Exchange Traded Funds)

A gold ETF tracks the price of gold and trades on the stock market like a stock. You never hold physical gold. The upside is convenience, low fees, and no storage. The downside is that you own a financial product, not a tangible asset.

Gold Coins and Bars (Bullion)

Pure gold in standardized weights. Lower premiums than jewelry (usually 3 to 8% versus 10 to 25% for jewelry). Same storage challenge without the wearable benefit.

Gold Savings Accounts and Digital Gold

Some platforms let you buy gold digitally in small amounts. Easy to start (even $10 at a time). The risk is that you are trusting a company to hold your gold.

Frequently Asked Questions

Is gold a good investment for beginners in 2026?

Gold can be a strong part of a beginner’s portfolio, but it works best alongside stocks, not as a replacement for them. From 2020 to 2026, gold returned roughly 150% to 155%, while the S&P 500 returned roughly 155% with dividends reinvested. Both dramatically outperformed savings accounts. Most experts recommend keeping 5 to 15% of your portfolio in gold.

Did gold beat stocks from 2020 to 2026?

Gold and stocks performed almost identically over this period. Gold returned roughly 150% to 155%, while the S&P 500 returned roughly 129% in price gains and roughly 155% when you include reinvested dividends. The difference is small enough that either one could be called the winner depending on the exact purchase date and method. The real takeaway is that both dramatically outperformed savings accounts.

Is gold jewelry a good investment?

Gold jewelry can be a good investment, but it comes with a making charge (10 to 25% above gold value) that pure gold bars or ETFs do not have. Over time, if gold appreciates significantly, the growth can more than cover this premium. Gold jewelry also has emotional and cultural value that financial products cannot replicate. For many families, it serves as both a wearable asset and a long-term store of wealth.

How much gold should I have in my portfolio?

Most financial experts suggest 5 to 15% of your total portfolio. This provides a meaningful hedge against inflation and market downturns without sacrificing the growth potential of stocks. The exact percentage depends on your risk tolerance, time horizon, and overall goals.

Does gold always beat inflation?

Over long periods, gold has historically kept pace with or outpaced inflation. But there have been shorter periods where gold declined while inflation continued. Gold is a long-term inflation hedge, not a short-term guarantee.

Can I start investing in gold with just $100?

Yes. You can buy a small gold coin, purchase fractional shares of a gold ETF through most brokerage apps, or use digital gold platforms that let you buy in small amounts. In many cultures, families buy small amounts of gold consistently over the years, building a collection gradually.

What happens to gold when interest rates go up?

Higher interest rates generally put downward pressure on gold prices because they make savings accounts and bonds more attractive relative to gold (which pays no interest). However, if inflation remains high even as rates rise, gold can still hold value because its primary appeal is as an inflation hedge. The 2020 to 2026 period showed that gold can perform well even during periods of rising rates if other factors like money printing, central bank buying, and geopolitical tension are strong enough.

Final Thoughts

Six years ago, I bought my wife gold earrings and a ring. It cost me a little over $1,000. That gold is now worth roughly $2,500.

Was gold the best possible investment? Over this specific period, it nearly tied with stocks. Both more than doubled. If I had bought an S&P 500 index fund instead, I would have ended up with roughly the same amount.

But I also would not have seen my wife’s face light up when she opened the box.

The real lesson from this comparison is not “buy gold” or “buy stocks.” The real lesson is that both of them dramatically outperformed the savings account. The $1,000 left in savings barely grew while inflation quietly ate away at its purchasing power.

Long-term cash can become a melting ice cube when inflation stays above the interest you earn. Whether you move it into gold or stocks matters less than whether you move it at all.

Stocks give you growth and dividends. Gold gives you protection and permanence. Savings give you short-term safety. You need all three in the right proportions. But the biggest mistake you can make is leaving everything in the “safe” option and watching it quietly lose value year after year.

That is what the math says. And the math does not care about opinions.

Tariq is one of the smartest people I know. Graduated near the top of his class, got a decent job, never gambled, never blew money on ridiculous things. But at 34 years old, he had exactly $312 in savings. Not $312,000. Three hundred and twelve dollars.

When I asked him why, he looked at me like I’d asked him why the sky is blue. “I don’t come from money,” he said. “Building wealth is for people who already have it.”

I’ve heard that sentence, or something close to it, from so many people that I’m starting to think it’s some kind of virus. A money mindset virus that spreads quietly and keeps perfectly capable people broke.

Here’s what Tariq didn’t know: wealth is not inherited. It’s engineered. And the blueprint? It’s not as complicated as Wall Street wants you to believe.

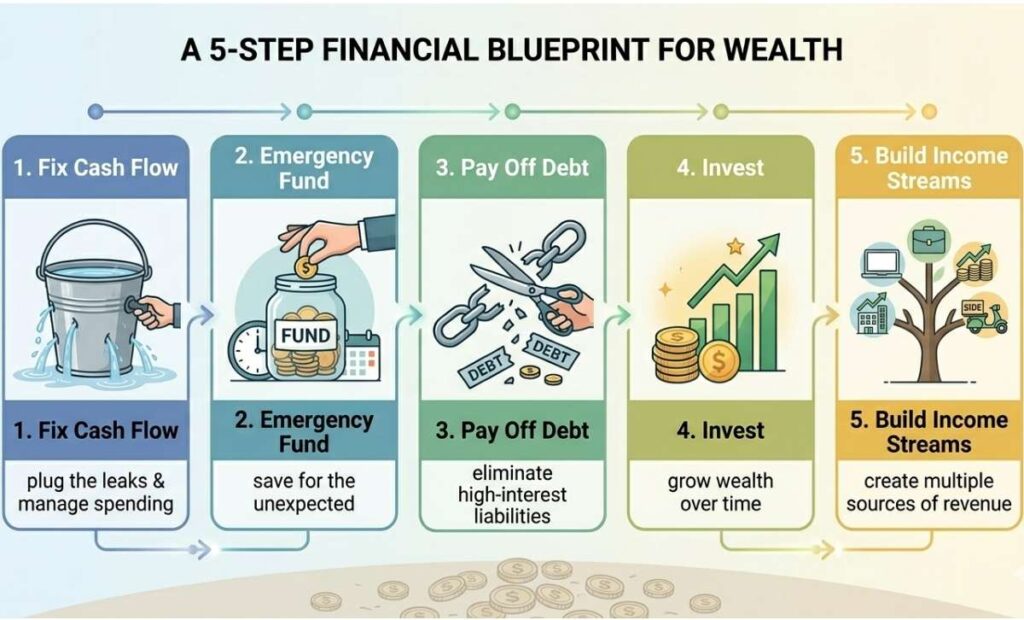

In this article, I’m going to give you the exact 5-step framework for building wealth from scratch, even if you’re starting with nothing, even if you grew up with nothing, and even if the word “investing” still makes your eyes glaze over.

Let’s get into it.

Table of Contents

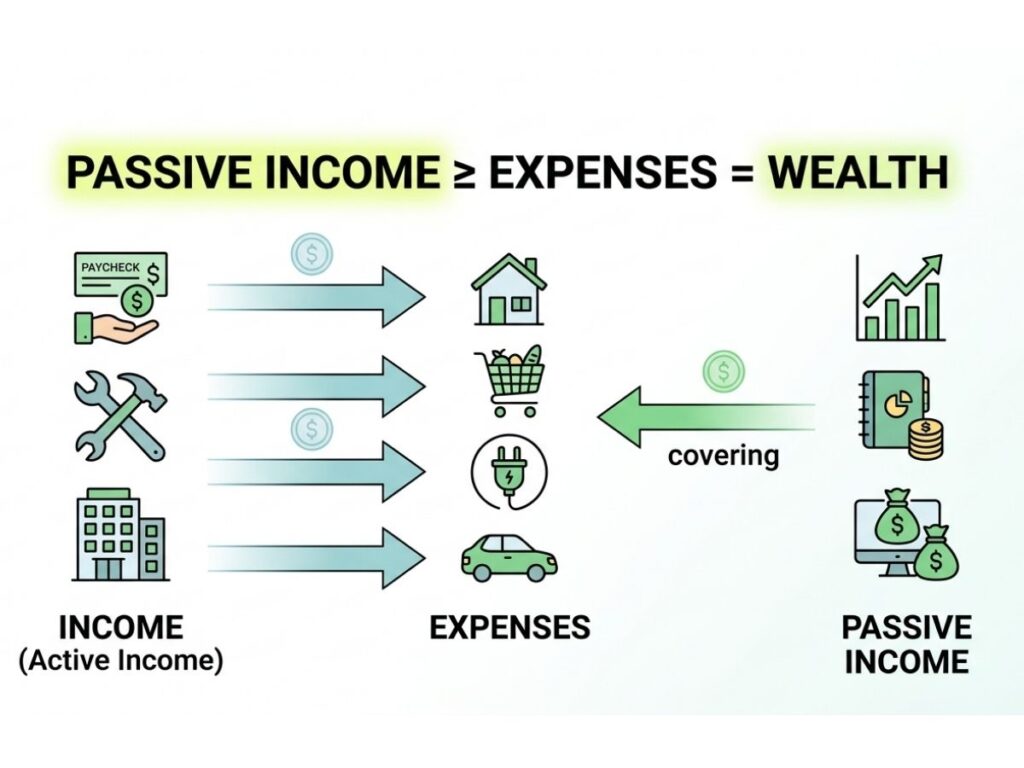

But First: What Does “Wealth” Actually Mean?

Before we talk about how to build wealth, we need to agree on what it is. Because most people have it wrong.

Wealth is not a salary. A doctor earning $300,000 a year who spends $310,000 is not wealthy — they’re one missed paycheck away from a crisis. Wealth is also not a flashy car or a big house. Those are symbols of wealth, and very often, they’re funded by debt.

Real wealth is when your money works harder than you do.

More precisely, you are wealthy when your passive income (money coming in while you sleep) covers your living expenses. That’s it. That’s the finish line.

The good news? You don’t have to reach the finish line to start experiencing the benefits. Every step toward that line makes your life more stable, more flexible, and honestly, a lot less stressful.

Now. The blueprint.

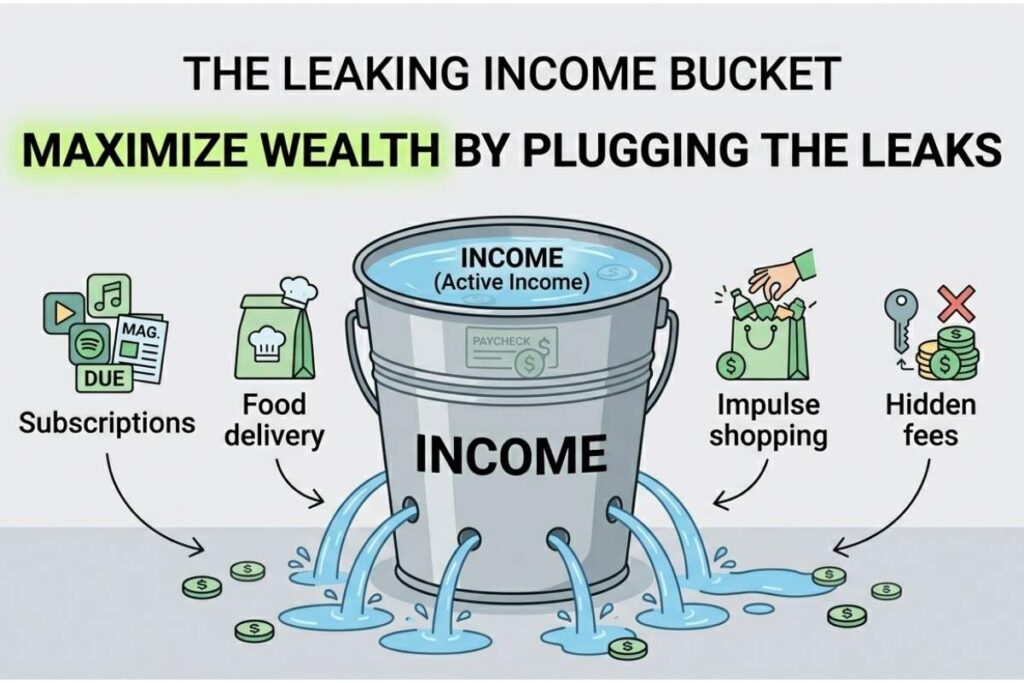

Step 1: Stop the Bleeding (Fix Your Cash Flow)

I once went three months without looking at my bank account. I’m not proud of it. I told myself I was “too busy,” but honestly? I was scared of what I’d see.

When I finally looked, really looked, I found $140/month going to a gym membership I hadn’t used since January (it was October). I found a $15/month subscription to a streaming service I’d signed up for during a free trial and completely forgotten. I found three separate food delivery apps all charging me annual fees.

That’s nearly $200 a month going absolutely nowhere.

Here’s the harsh truth: you cannot build wealth if more money is leaving than arriving. It’s like trying to fill a bathtub with the drain open. The first job is to plug the drain.

How to fix your cash flow right now:

Do a subscription audit. Go through your last two months of bank statements line by line. Highlight everything that recurs monthly. Cancel anything you forgot you had or don’t actively use. Most people find $50–200/month here.

Track every rupee/dollar for 30 days. Not to punish yourself — just to see. You cannot fix what you cannot see. Use a simple notes app, a spreadsheet, or any budgeting app. Just write it down.

Apply the 50/30/20 Rule:

50% of your take-home pay → Needs (rent, food, transport, utilities)

30% → Wants (eating out, entertainment, shopping)

20% → Savings and investments (this is non-negotiable — more on this shortly)

If your current math doesn’t allow for 20% savings, that’s okay. Start with 5%. Then push it to 10%. The number matters less than the habit.

Money Cornucopia Principle: Wealth is built in the gap between what you earn and what you spend. Widen the gap. Every. Single. Month.

Step 2: Build Your “Never Panic” Fund (Emergency Savings)

Here’s a scenario I want you to imagine.

It’s a Tuesday. Your car breaks down on the way to work. The mechanic calls and says it’ll cost $800 to fix. You have $200 in your account.

What do you do?

If you don’t have an emergency fund, you do one of three terrible things: you put it on a credit card (and pay 20%+ interest), you borrow from family (and damage a relationship), or you simply can’t fix the car and lose your job because you can’t get to work.

This is the cycle that keeps people broke. One emergency derails everything.

An emergency fund is the foundation of all wealth. Without it, every financial plan you build is one bad day away from collapse.

How big should your emergency fund be?

The standard advice is 3–6 months of living expenses. If your monthly expenses are $1,500, you need $4,500–$9,000 sitting in a savings account, untouched, earning interest.

That might sound like a lot. Here’s how to make it feel manageable:

Where to keep it: A high-yield savings account. Not under your mattress. Not in your checking account where you’ll spend it. A separate account that earns you some interest while it sits there, ready for when you need it.

My personal rule? I treat my emergency fund like it doesn’t exist — until I actually need it. Out of sight, out of mind, but always there.

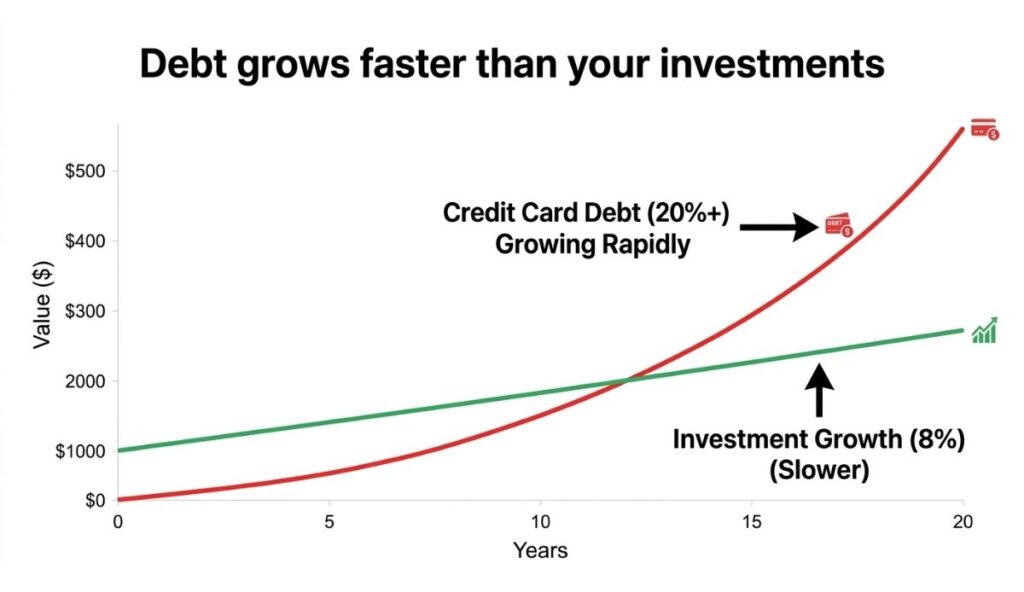

Step 3: Destroy High-Interest Debt (The Wealth Killer)

If Step 1 is plugging the drain and Step 2 is starting to fill the tub, then high-interest debt is someone drilling new holes while you’re not looking.

Credit card debt is, without exaggeration, one of the most destructive financial forces in an ordinary person’s life. At 20–30% annual interest, it grows faster than almost any investment you’ll ever make. While you’re trying to build wealth at 8% per year in the stock market, your credit card is eating it alive at 25%.

Let me make this real with numbers:

If you have $5,000 on a credit card at 22% interest and you only pay the minimum each month — you will pay over $8,000 in interest alone and take 15+ years to pay it off. On a $5,000 debt. That is $8,000 that will never be invested. Never compound. Never work for you.

Two proven strategies to crush debt:

The Avalanche Method (mathematically optimal): List all your debts from highest interest rate to lowest. Pay minimums on everything except the highest-rate debt — throw every extra dollar at that one. When it’s gone, attack the next. This saves the most money in interest.

The Snowball Method (psychologically powerful): List your debts from smallest balance to largest. Pay off the smallest one first, regardless of interest rate. When you kill that first debt, you get a rush of momentum that makes you want to keep going. Dave Ramsey swears by this one, and honestly? For people who struggle with motivation, it works.

Pick whichever one you’ll actually stick to. The best strategy is the one you follow.

One rule: Once a debt is paid off — do not refill it. This seems obvious. It is not obvious to your future self at 11pm on a Friday with a shopping app open.

Step 4: Make Your Money Grow (Start Investing)

This is the step where most people freeze up. “Investing is complicated.” “I don’t know enough.” “I’ll start when I have more money.”

I said all three of those things for two years. Two years of my money sitting in a savings account earning 0.5% interest while inflation quietly ate it alive.

Here’s the truth no one tells you clearly: not investing is a decision. It’s a decision to let inflation shrink your money a little bit every year. Staying in a savings account isn’t “safe” — it’s slowly losing ground.

The beautiful thing about investing as a beginner is that you don’t need to pick stocks, read earnings reports, or understand complex financial instruments. You just need to understand one concept: compound interest.

Albert Einstein reportedly called compound interest the eighth wonder of the world. The idea is simple: your money earns returns. Then those returns earn their own returns. Then those returns earn returns. It snowballs — slowly at first, then explosively.

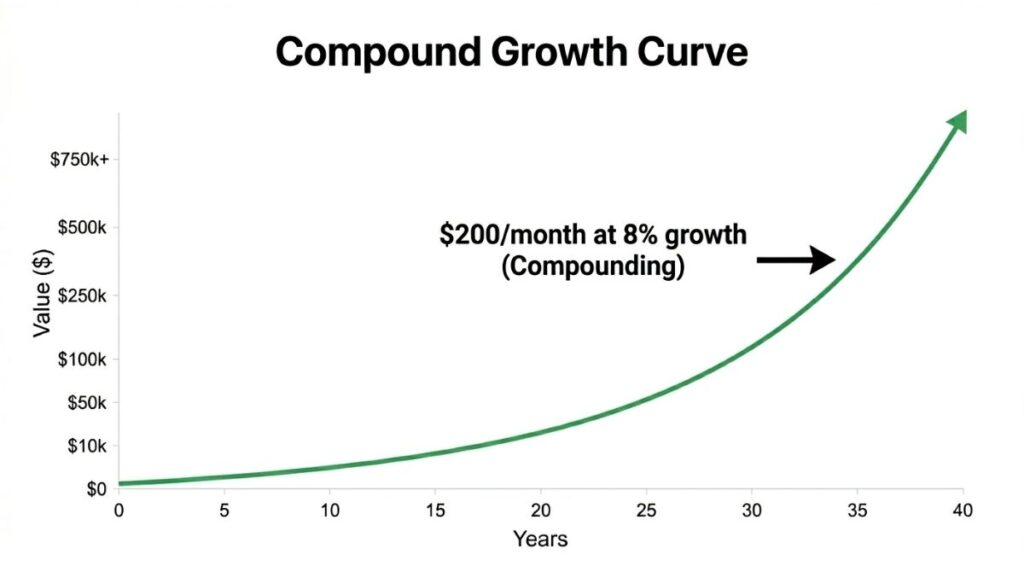

Here’s what that looks like in real life:

If you invest $200 per month starting at age 25 with an average annual return of 8%:

By age 35 (10 years): ~$36,000

By age 45 (20 years): ~$118,000

By age 55 (30 years): ~$300,000

By age 65 (40 years): ~$700,000

You contributed $96,000 of your own money over 40 years. The rest — over $600,000 — was created by compound interest doing its quiet, relentless work.

Where to start investing as a beginner:

Index Funds: Instead of picking individual stocks (risky, complicated, time-consuming), you buy a small slice of thousands of companies at once. When the overall market goes up — and historically, over the long run, it always has — your investment goes up. Low fees, low effort, highly effective.

ETFs (Exchange-Traded Funds): Similar to index funds but traded on the stock market like individual stocks. Very beginner-friendly.

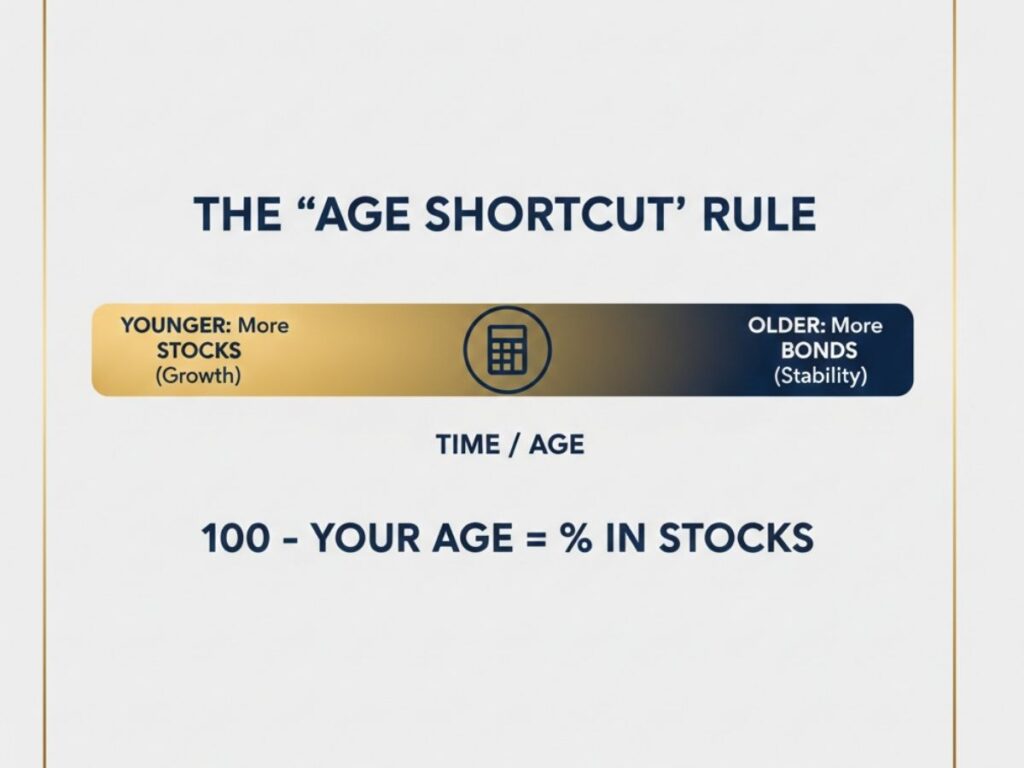

Stocks vs. Bonds split: As a beginner, a simple starting point is: subtract your age from 100. That’s your stock percentage. If you’re 30, put 70% in stocks and 30% in bonds. As you age, gradually shift more toward bonds for stability.

The golden rule: Start now. Start small if you have to — even $25 a month. But start. Time in the market beats timing the market every single time.

Step 5: Protect and Multiply What You’ve Built

Most wealth-building advice stops at “invest in index funds.” That’s good advice. But it’s incomplete.

Building wealth isn’t just about growing your money — it’s about making sure a single bad event doesn’t wipe out everything you’ve spent years building.

Protect your wealth with insurance:

Health insurance is non-negotiable. A single serious illness without coverage can generate medical bills that take decades to pay off. This is not hypothetical — it’s the leading cause of bankruptcy in many countries.

Life insurance matters the moment someone depends on your income — a spouse, children, aging parents. Term life insurance is affordable and straightforward. Get it before you think you need it.

Emergency fund (yes, again) — I keep mentioning it because the wealthiest people I know treat their emergency fund like a sacred covenant. It is the buffer between you and financial catastrophe.

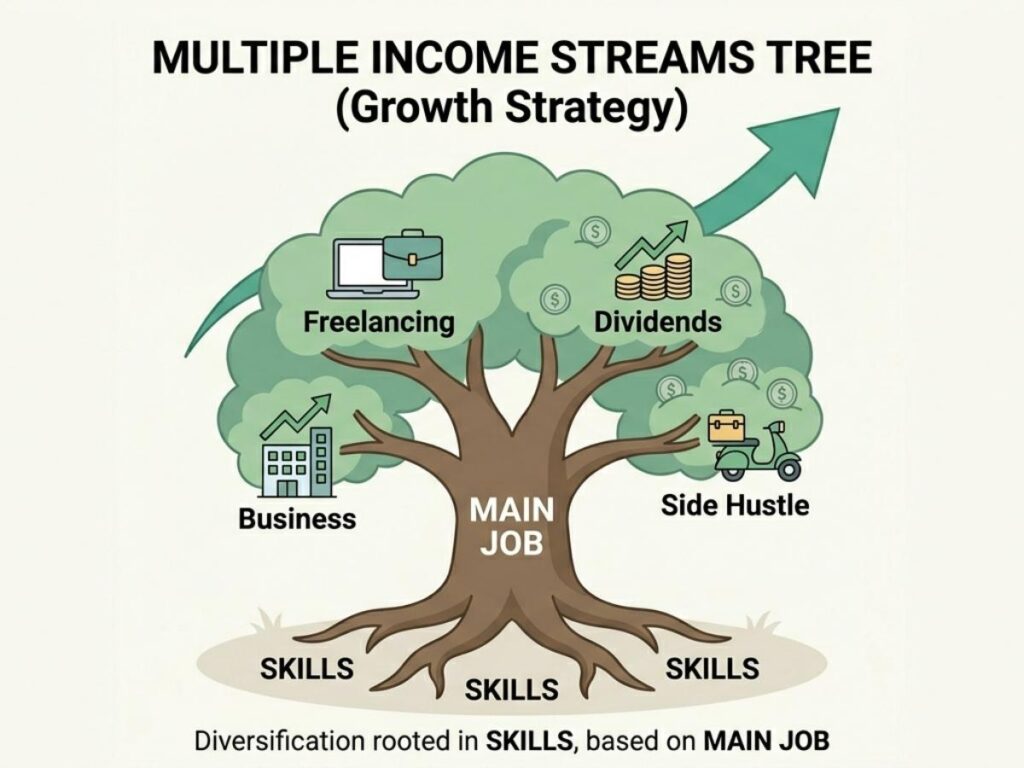

Multiply your wealth with income streams:

Building wealth from one job, one income source, is possible — but fragile. The wealthy don’t just have one river of money; they have many streams feeding into it.

Consider:

Side income: Freelancing, tutoring, selling a skill online

Passive income: Dividends from investments, interest from bonds, rental income if you get there

Invest in yourself: Skills that make you more valuable — coding, writing, sales, communication — these raise your earning power, which accelerates everything above

You don’t need five income streams tomorrow. Start building a second one. Then a third. Each one you add makes the whole system more resilient.

The Full Blueprint at a Glance

Here’s your 5-step wealth-building framework, simplified:

Step

Action

Goal

1

Fix cash flow — stop the bleeding

Spend less than you earn

2

Build an emergency fund

3–6 months of expenses saved

3

Eliminate high-interest debt

Freedom from the wealth killers

4

Start investing consistently

Let compound interest do the heavy lifting

5

Protect and multiply

Build multiple streams, shield what you have

These steps are sequential for a reason. It’s hard to invest effectively if you’re drowning in debt. It’s hard to pay off debt if your cash flow is broken. Work them in order, even if it feels slow.

The Real Secret Nobody Talks About

You want to know the actual difference between people who build wealth and people who don’t?

It’s not intelligence. It’s not income. It’s not connections or luck or a trust fund.

It’s consistency over a long period of time.

That’s it. I know it sounds anticlimactic. We live in a world that sells us overnight success stories, crypto millionaires, and 30-under-30 lists. But the vast, overwhelming majority of real wealth is built quietly — one month of saving, one boring index fund contribution, one cancelled subscription, one avoided impulse purchase at a time.

My cousin Tariq, by the way? He started with Step 1 six months ago. He cancelled subscriptions, set up a $100/month auto-transfer to a savings account, and opened his first investment account with $250. He hasn’t gotten rich. But for the first time in a decade, he’s not living in fear of the next emergency.

That’s where wealth begins. Not with a windfall. Not with a hot stock tip. With a decision, followed by another decision, followed by a habit, followed by a life that looks completely different five years from now.

The best time to start was ten years ago. The second-best time is today.

Your Action Step for This Week

Don’t try to do all five steps at once. Pick one thing from this article and do it this week:

✅ Cancel one subscription you forgot you had

✅ Open a high-yield savings account for your emergency fund

✅ List all your debts and their interest rates

✅ Open an investment account and make your first deposit — even if it’s $25

✅ Calculate your 50/30/20 budget for this month

Small action. Repeated consistently. That’s the whole game.

Which step are you starting with? Drop a comment below — let’s build this together. 💰

Oil prices rise. You notice it at the petrol station first. Then your grocery bill goes up. Then your electricity bill. Then the delivery fee on your online order.

It feels like everything is connected. Because it is.

Most people understand that expensive oil means expensive petrol. What most people do not understand is everything else. The food. The electricity. The packaging. The fertilizer. The plastics. The shipping. And the savings account that quietly loses value while all of this is happening.

This article explains the full chain reaction in plain language, from a single barrel of crude oil to your monthly budget, and what you can actually do about it.

Quick Answer: Why Do Oil Prices Affect Everything?

Oil affects prices across the economy for two reasons. First, oil is the fuel that powers almost all transportation, meaning everything that moves anywhere costs more when oil is expensive. Second, oil is a physical ingredient in a vast range of products, from the plastic packaging around your groceries to the fertilizer used to grow the food inside.

When oil gets expensive, the cost of moving things goes up. The cost of making things goes up. The cost of growing things goes up. Eventually, all of those costs reach you, the buyer at the end of the chain.

The impact is not immediate. Petrol prices respond within days. Shipping costs follow in weeks. Grocery prices take months. But the connection is real, it is predictable, and understanding it helps you manage your budget before the damage arrives rather than after.

Table of Contents

Why Oil Is More Than Just Petrol

Most petroleum becomes fuel. But a significant share becomes the materials and chemicals that make up everyday life.

According to the US Energy Information Administration, about 71% of all petroleum consumed in the US is used for transportation fuels, including gasoline, diesel, and jet fuel. The rest is used across industrial, commercial, residential, and other uses, including petrochemicals that become plastics, packaging, synthetic fibers, and many everyday materials.

Oil is not only something you burn. It is also something the modern economy builds with. The plastic on your desk. The packaging on your lunch. The fabric in your clothes. Petrochemicals derived from petroleum are used in the manufacture of an enormous range of everyday products.

The quantity of oil-based polyester in clothing has doubled since 2000. Over half of all fibers produced worldwide are now made from petroleum. The cosmetics industry is heavily dependent on petroleum since items such as hand cream, shampoo, and most makeup are made from petrochemicals. S&P Dow Jones Indices

That is why an oil price change does not stay contained at the pump. It moves outward through supply chains into almost every category of spending you have.

How Oil Reaches Your Grocery Bill

Oil does not just deliver your food. It helps grow it.

This is the part most people never think about, and it is where the biggest impact on household budgets comes from.

The food industry is especially sensitive to the price of energy, more so than any other sector, because petroleum is a key component of its supply chain at every step of the way, from planting and harvesting through processing and packaging. The biggest use of petroleum in industrial farming is not transportation or fueling machinery but rather fertilizers. Vast amounts of oil and natural gas go into fertilizers and pesticides used to produce and protect grains, vegetables, and fruits. It takes 283 gallons of oil to raise one 1,250-pound steer. S&P Dow Jones Indices

Before a single truck has moved, the food you will buy in three months time is already more expensive to grow.

Then add the transport layer. Fuel prices account for 50% to 60% of the total operating cost of shipping goods by ship. When diesel gets expensive, every truck, train, and ship carrying food charges more. Distributors add surcharges. Wholesalers pass costs to supermarkets. Supermarkets eventually pass costs to you (Swissamerica).

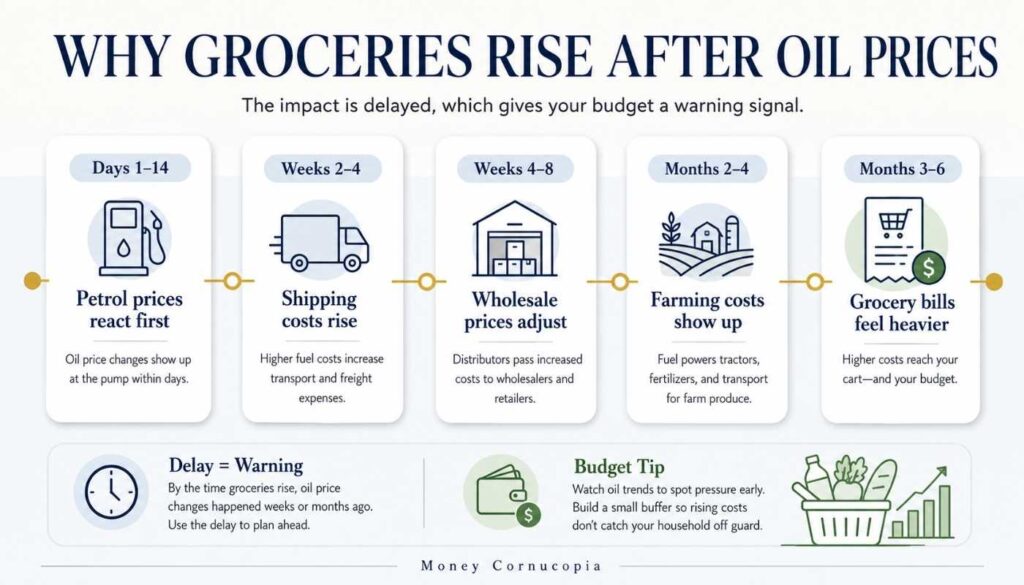

Why Food Prices Often Rise After Oil Prices

The lag between an oil spike and a higher grocery bill is real. Here is exactly how it works.

The chain spreads in stages, and each stage adds time:

Timeline

What happens

Where you feel it

Days 1 to 14

Crude oil prices rise. Wholesale fuel prices climb. Petrol station prices jump

Higher transport costs reach distributors and wholesalers. Supermarkets begin seeing higher wholesale prices from suppliers

Supermarket supply chain

Months 2 to 4

Fertilizer costs rise because natural gas is a key ingredient in fertilizer production. Food planted months ago becomes more expensive to harvest and process

Farming input costs

Months 3 to 6

Grocery prices for consumers begin rising noticeably. Fresh produce, meat, and dairy tend to rise first as they are most transport-dependent

Your grocery receipt

I noticed this in my own shopping. The petrol price spike happened in early spring. My grocery bill started feeling heavier two to three months later, without me buying anything different. The lag is real, and it is also a warning signal. When you see an oil price spike in the news, you have weeks, sometimes months, before the full impact reaches your grocery receipt.

Americans spend roughly 10% of their disposable income on food, which is about twice what they spend on gas. Concerns over grocery prices topped consumer concern polling in 2025, 2024, and 2023. The grocery impact is the oil shock that lasts the longest and hurts the most (Bitget).

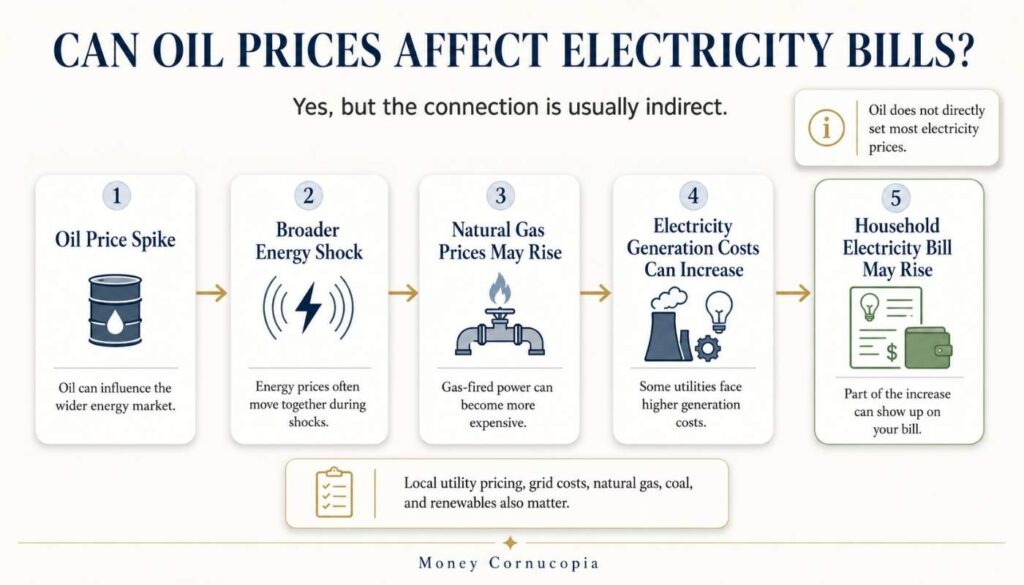

Can Oil Prices Affect Electricity Bills?

Yes, but the connection is indirect. Here is how it actually works.

Oil does not directly set most electricity prices. In most countries, electricity prices are more directly affected by natural gas, coal, renewables, grid infrastructure costs, and local utility pricing. But during broader energy shocks, oil and natural gas prices can rise at the same time, which is why an oil price spike may still coincide with higher electricity bills even for households that never buy a drop of petrol.

According to the US Energy Information Administration, natural gas accounts for roughly 41% of US electricity generation. When energy markets experience broad supply disruptions, natural gas prices often rise alongside oil, which can push electricity generation costs higher and filter through to household bills.

The second connection is through heating. Homes heated with oil or natural gas see direct cost increases when energy prices rise. Even homes on electricity face higher bills when the electricity itself costs more to generate.

This is why an energy price shock does not only hit drivers. It hits renters, households in cold climates, and anyone who uses electricity, which means everyone.

How Oil Affects Shipping, Packaging, and Online Shopping

Every time you click add to cart, you are buying something that moved through an oil-powered supply chain.

The product you ordered was made in a factory that used energy, packaged in plastic made from petrochemicals, transported from a manufacturer to a warehouse by diesel-powered vehicles, stored in a warehouse that uses electricity, and then loaded onto another vehicle for final delivery.

Every stage uses oil. Every stage passes costs forward. By the time the package arrives at your door, the oil price has been embedded multiple times.

When fuel prices rise, courier companies adjust their surcharges quickly. You may see delivery fees tick up, free delivery thresholds increase, or shipping times lengthen as companies reroute to save fuel. None of it is dramatic on any given day, but across a full month of shopping, it adds up.

How Oil Prices Affect Inflation

Oil-driven inflation is different from other types, and that difference matters for your money.

Oil price increases are generally thought to increase inflation and reduce economic growth. In terms of inflation, oil prices directly affect the prices of goods made with petroleum products and indirectly affect costs such as transportation, manufacturing, and heating. The increase in these costs can, in turn, affect the prices of a variety of goods and services as producers pass production costs on to consumers. Bitget

This type of inflation, driven by rising production costs rather than rising consumer demand, is what economists call cost-push inflation. It is harder to fight than demand-driven inflation because central banks cannot reduce the price of oil by raising interest rates. They can slow spending, but they cannot fix a supply disruption.

That means oil-driven inflation tends to be persistent. It does not disappear when the central bank acts. It fades only when oil prices themselves stabilize or fall. The 1973 oil shock, the 1979 oil shock, and the 2008 commodity spike all followed the same pattern. Prices rose sharply, inflation ran high, and the full economic effect lasted far longer than the initial supply disruption.

How Inflation Quietly Hurts Your Savings

This is the part nobody explains, and it is where the quiet damage happens.

When oil drives inflation, your account balance can go up while your purchasing power goes down. That gap between your savings rate and the inflation rate is where the real cost lives.

This is not about being alarmist. It is about recognizing that your account balance growing does not automatically mean your purchasing power is growing. If your money earns 2% in a savings account while oil-driven prices rise by 5%, your balance is higher, but your real buying power is lower. You can buy less with more money. I covered exactly how this works in my article on what happens when your savings rate is lower than inflation.

There is a very strong correlation between the movement of energy prices and the movement of food prices. Oil topping $100 a barrel has historically coincided with significant food price inflation. Wall Street Survivor

Let me put the household budget impact in concrete terms:

Budget item

Normal month

Oil shock month

Petrol and transport

$80

$110

Groceries

$300

$340

Electricity bill

$60

$75

Online shopping delivery

$15

$22

Total monthly impact

$455

$547

That is roughly $90 extra per month. Over a year, that is more than $1,000 in additional spending that was not in the original budget. The impact is not dramatic enough to feel like an emergency on any given day. It is quiet. Gradual. Cumulative. That is exactly how oil-driven inflation works.

Understanding the time value of money means understanding that money sitting still is money moving backwards when inflation runs above your savings rate. Inflation-resilient assets like broadly diversified index funds have historically outpaced oil-driven inflation over long periods, which is why keeping some portion of your money working outside a savings account matters when energy prices stay elevated.

What You Can Actually Do When Oil Prices Rise

The practical steps that actually help your budget, not just generic advice.

Review Your Budget Before the Prices Arrive

Oil drives prices with a predictable lag. Use that lag. When you see oil prices spiking in the news, review your budget now. Identify where you have flexibility before the increases arrive rather than scrambling to adjust after your grocery bill has already climbed.

Check Your Savings Rate Against Inflation

Go to your bank account and find your savings interest rate. Compare it to the current inflation rate. If your rate is lower than inflation, which it typically is during oil-driven price spikes, your real purchasing power is shrinking even while your balance grows. Emergency funds should stay in cash. But money you will not need for 12 months or more should be working harder. I covered the step-by-step approach in how to start investing with just $100.

Think About Your Asset Allocation

When oil drives inflation, having your money spread across different types of assets matters more than usual. A basic understanding of asset allocation and diversification helps you decide how much of your money should stay in cash, how much in investments, and how much in assets that have historically held value during inflationary periods.

Adjust Your Flexible Spending

Some oil-driven costs are fixed: electricity, gasoline to get to work, and heating. Others are flexible: eating out frequency, brand choices at the supermarket, and timing of discretionary purchases. Identifying which is which gives you real control, even when the broader economy is working against your budget.

Stay the Course With Long-Term Investments

If your investment portfolio dips during an oil shock, that is normal and expected. Markets have absorbed every major oil shock in history. Short-term price drops during energy crises have historically recovered. Making dramatic investment changes in response to oil news is usually a worse outcome than staying the course with a sensible long-term allocation.

Frequently Asked Questions

Why do oil prices affect food prices?

Higher oil prices raise costs across the food supply chain, from fuel used in farming and fertilizer production to transportation and refrigeration, according to the Federal Reserve Bank of St. Louis. Oil is not just used to deliver food. It is used to grow it through fertilizer production that requires oil and natural gas as raw materials. The effect on grocery prices is delayed by one to three months but is real and well-documented by agricultural economists (GoldSilver).

Do oil prices affect electricity bills?

Indirectly, yes. Oil does not directly power most electricity generation. According to the US Energy Information Administration, natural gas accounts for roughly 41% of US electricity generation. During broader energy market disruptions, oil and natural gas prices can rise at the same time, which is why an oil shock may coincide with higher electricity bills even for households that do not own a car.

Why do oil prices cause inflation?

Oil price increases are generally thought to increase inflation and reduce economic growth. Oil prices directly affect the prices of goods made with petroleum products and indirectly affect costs such as transportation, manufacturing, and heating. Producers typically pass these production cost increases on to consumers. Because oil affects so many sectors simultaneously, its price changes create broad, simultaneous cost increases across the economy, which is what drives generalized inflation (Bitget).

What happens to groceries when oil prices rise?

Grocery prices typically rise one to three months after an oil spike. Fresh produce, meat, and dairy tend to rise first because they are most transport-dependent. Fertilizer-related agricultural costs take longer, sometimes six months or more, to work through to food prices. Americans spend roughly 10% of their disposable income on food, about twice what they spend on gas, and grocery prices topped consumer concern polling for three consecutive years (Bitget).

How can I protect my budget from rising oil prices?

The most practical steps are reviewing your budget before grocery and energy prices fully arrive, checking that your savings account rate is not falling significantly behind inflation, considering whether your longer-term savings are appropriately allocated across different asset types, and adjusting flexible spending categories to absorb fixed cost increases. Understanding the lag between oil price spikes and grocery price rises gives you a practical window to prepare rather than react.

How long does it take for oil prices to affect grocery prices?

The full effect typically takes one to three months for most grocery items. Petrol prices react within days. Shipping and transport costs adjust within weeks. Grocery prices for consumers rise noticeably within one to three months. Fertilizer-related agricultural cost increases can take six months or longer to reach supermarket shelves.

Is the connection between oil prices and everyday costs permanent?

The connection exists as long as oil remains central to transportation, manufacturing, and agriculture. According to the EIA, petroleum products account for about one-third of total world energy consumption. Over time, the electrification of transport and renewable energy could reduce the sensitivity of everyday prices to oil. But for now, oil’s role in fuel, fertilizer, and plastic production means its price touches almost everything in the global economy.

Final Thoughts

When oil prices rise, the impact does not stay at the petrol station. It flows quietly through your grocery bill, your electricity bill, your delivery fees, your savings account, and your broader purchasing power.

The chain is long. The lag is real. And that lag is actually useful for anyone who understands it. You have weeks, sometimes months, between the oil price headline and the full impact on your household budget. That is enough time to prepare, adjust, and make decisions rather than react.

Oil touches almost everything you buy. Now you know why. And knowing why is the first step to making decisions that actually protect your money when prices start climbing.

Most people hear “Federal Reserve meeting” and immediately check out.

Eyes glaze over. Brain goes elsewhere. “That’s for economists and Wall Street guys,” they think.

But here’s the thing: what the Fed decides today will quietly ripple into your savings account, your credit card bill, and your investment portfolio. Whether you pay attention or not.

So let’s make this simple.

What’s Happening Today?

The Federal Reserve is holding its April meeting right now — and almost every analyst on the planet expects them to keep interest rates exactly where they are. No cut. No hike. Hold.

Why? Because the Middle East conflict has sent oil prices surging past $100 a barrel, and the Fed is watching carefully to see how that filters through into everyday prices, your groceries, your petrol, and your utility bills. They’re not ready to move until the picture gets clearer.

Oh, and one more thing: this may actually be Jerome Powell’s last meeting as Fed Chair. His likely successor is already waiting in the wings. A changing of the guard at the world’s most powerful financial institution. No big deal, right?

What Does This Actually Mean for YOU?

Your savings: High-yield savings accounts are still paying solid interest, somewhere between 4–5% annually in many places. That means your emergency fund is actually working right now. If yours is sitting in a regular bank account earning 0.5%, today is a good day to fix that.

Your debt: Rates on hold means your credit card interest isn’t getting worse. But it’s still brutal; most cards charge 20–25% annually. The Fed holding rates is not a reason to relax. It’s a reason to attack that debt while conditions are stable.

Your investments: Markets are near record highs despite all the noise. The S&P 500 closed at a record 7,173 yesterday. That might feel scary — is it too late to invest? It almost never is, if you’re thinking long-term. Volatility isn’t a warning sign. It’s just Tuesday.

The Bottom Line

The Fed doesn’t build your wealth. You do.

But understanding what they’re doing — and more importantly, what it means for your actual life — is the difference between reacting emotionally to financial news and making calm, smart decisions.

I still remember the conversation that changed everything.

It was 2019, and I was sitting in a coffee shop with my friend Sarah, a financial advisor. I’d just told her I wanted to start investing, but I only had about $100 saved up. I expected her to laugh or tell me to come back when I had “real money.”

Instead, she said something that stuck with me: “The best time to plant a tree was 20 years ago. The second best time is today. Even if that tree is just a seedling.”

That $100 I invested in 2019? Thanks to compound interest and consistent additions, it’s grown into something I never imagined back then. And here’s the truth most people don’t realize: you don’t need thousands of dollars to start building wealth. You just need to start.

If you’re reading this with $100 (or even less) and wondering if it’s “enough” to begin investing, this guide is for you.

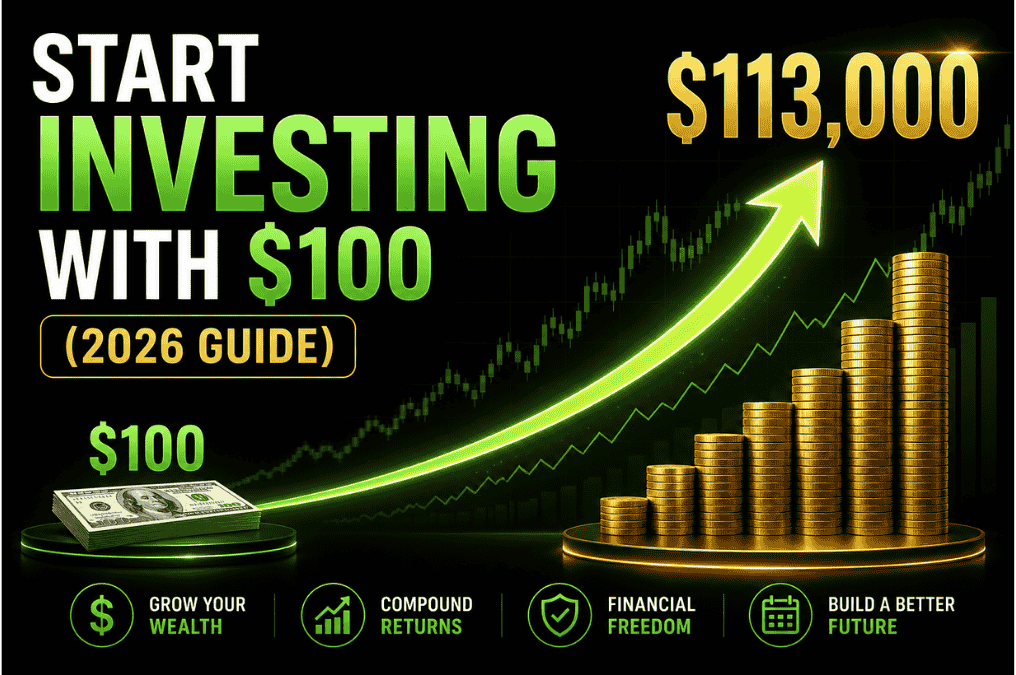

Table of Contents

Why $100 is Actually Enough to Start

Let me be blunt: the finance industry has spent decades convincing you that investing is only for wealthy people. They used to require minimum deposits of $3,000, $5,000, or even $10,000 just to open an account. This kept regular people locked out while the rich got richer.

But in 2026, that wall has completely crumbled.

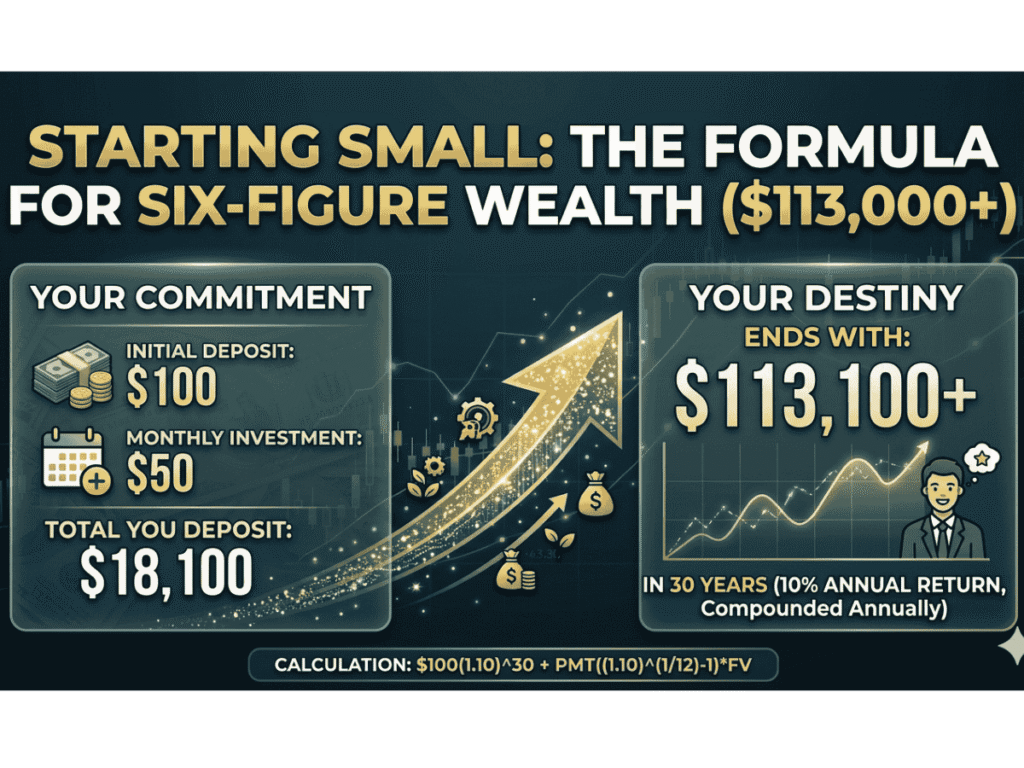

Thanks to technology and fractional shares, you can now invest with as little as $1. Yes, ONE dollar. But let’s talk about why starting with $100 is actually the perfect amount:

The Power of Starting Small

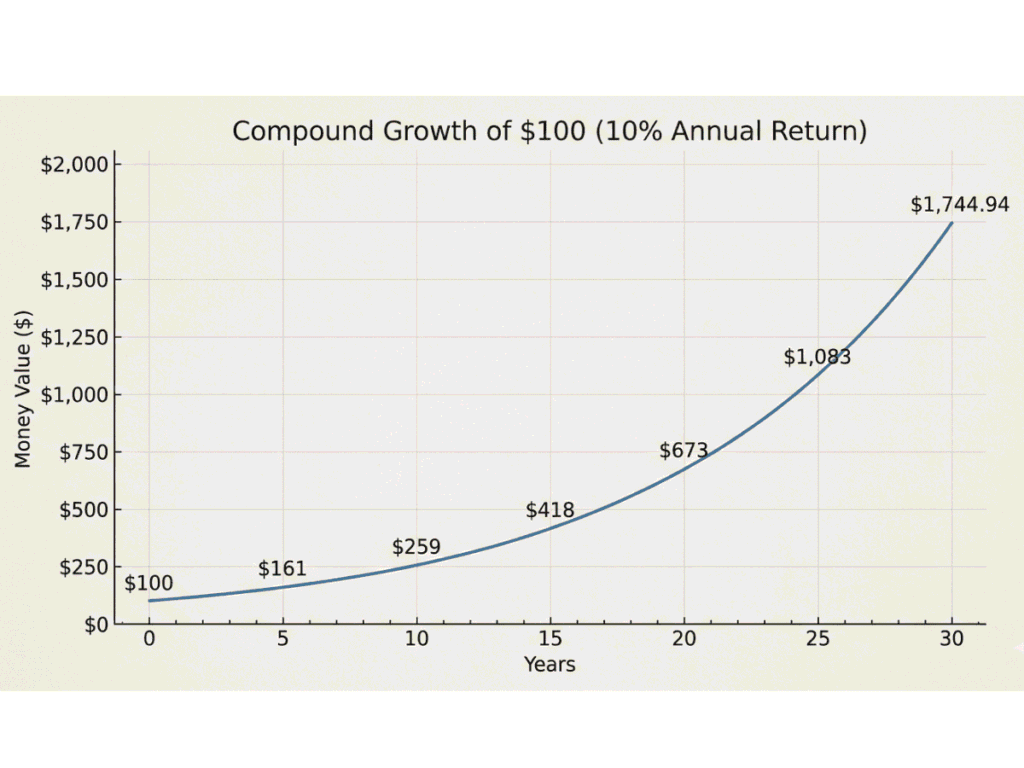

Here’s what happens when you invest $100 today at a 10% average annual return (which is historically what the S&P 500 has delivered):

After 1 year: $110

After 5 years: $161

After 10 years: $259

After 20 years: $673

After 30 years: $1,745

“But that’s not life-changing money!” you might say.

You’re right. But here’s what you’re missing: most people who start with $100 don’t stop there.

Use this free Compound Interest Calculator to see exactly how your $100 could grow depending on your return and timeline.

The Real Value: Building the Habit

When I invested my first $100, the money itself wasn’t the point. What mattered was that I:

Learned how to invest without risking my life savings

Overcame the fear that keeps most people stuck

Built the habit of investing regularly

Saw my money grow (even if slowly), which motivated me to invest more

Within 6 months, I was adding $50 every paycheck. Within a year, I bumped it to $100. That initial $100 wasn’t my fortune—it was my starting line.

The “Wait Until I Have More” Trap

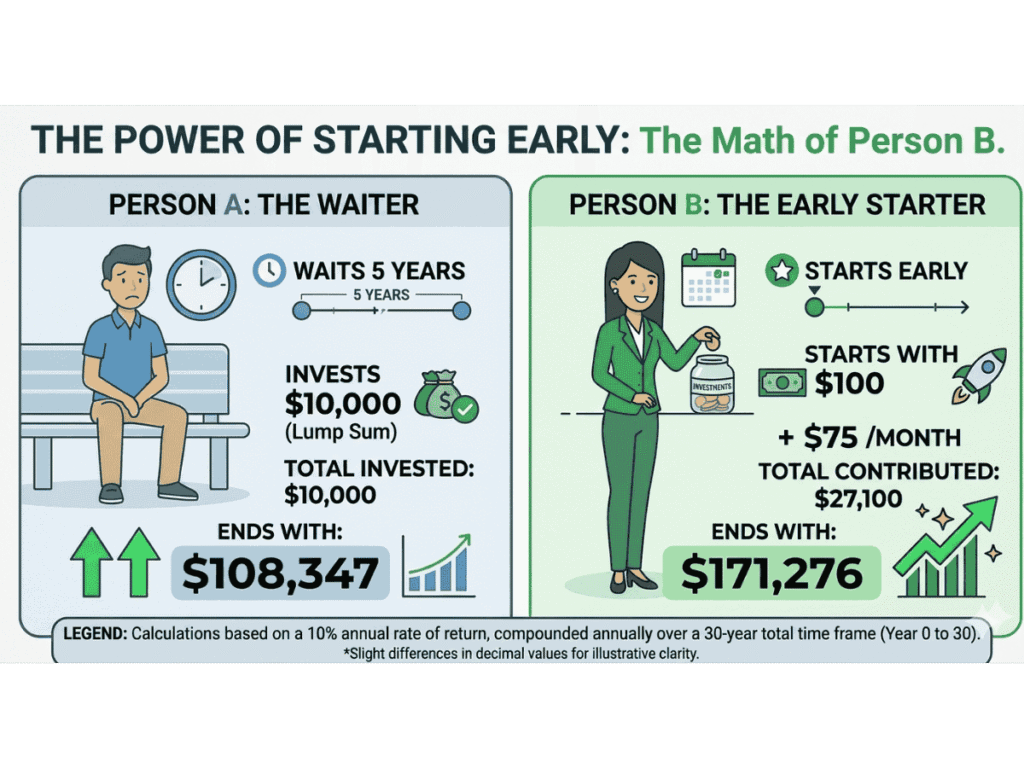

Here’s the math that will shock you:

Person A waits 5 years to save up $10,000, then invests it all at once.

Person B invests $100 today and adds just $75/month for 5 years.