If inflation is higher than your interest rate, your money is shrinking—even if your balance keeps going up.

That’s not a small problem. It’s a silent loss happening in the background every single day.

This is called a negative real return—and most people don’t even realize it’s happening to their savings.

In this guide, you’ll learn:

- Why your savings are quietly losing value

- How to calculate your real return in seconds

- And 3 simple moves to stop losing money starting today

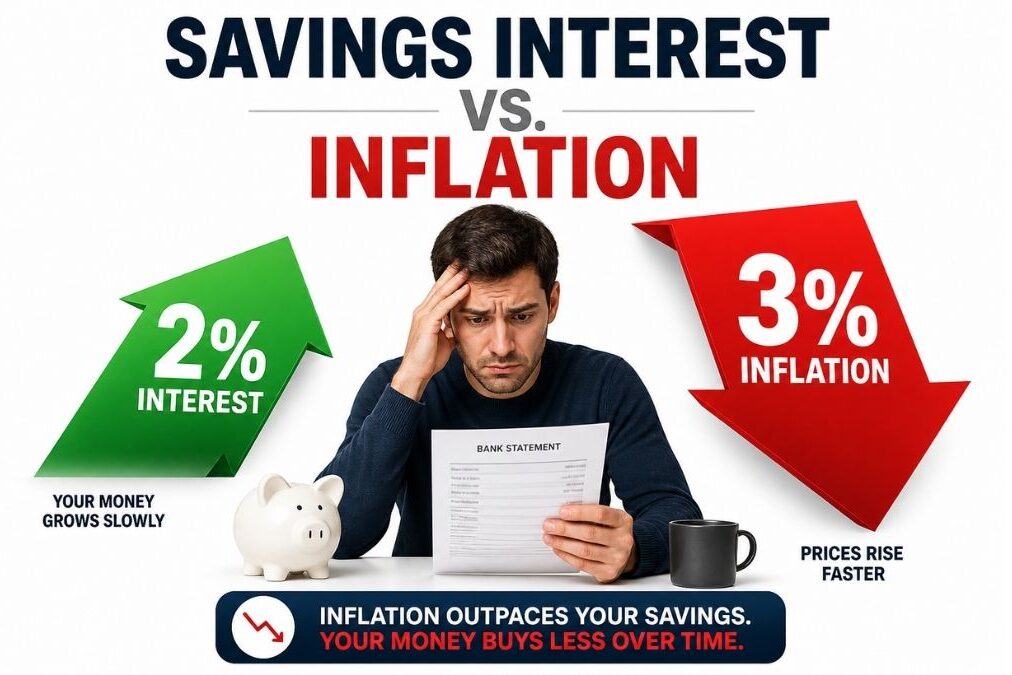

The Math Your Bank Hopes You Never Do

Your bank shows you one number: your interest rate.

Let’s say it’s 2%.

Looks fine… until you look at the number they don’t show you:

Inflation is currently around 3%.

That means everything you buy—groceries, rent, fuel—is getting more expensive every year.

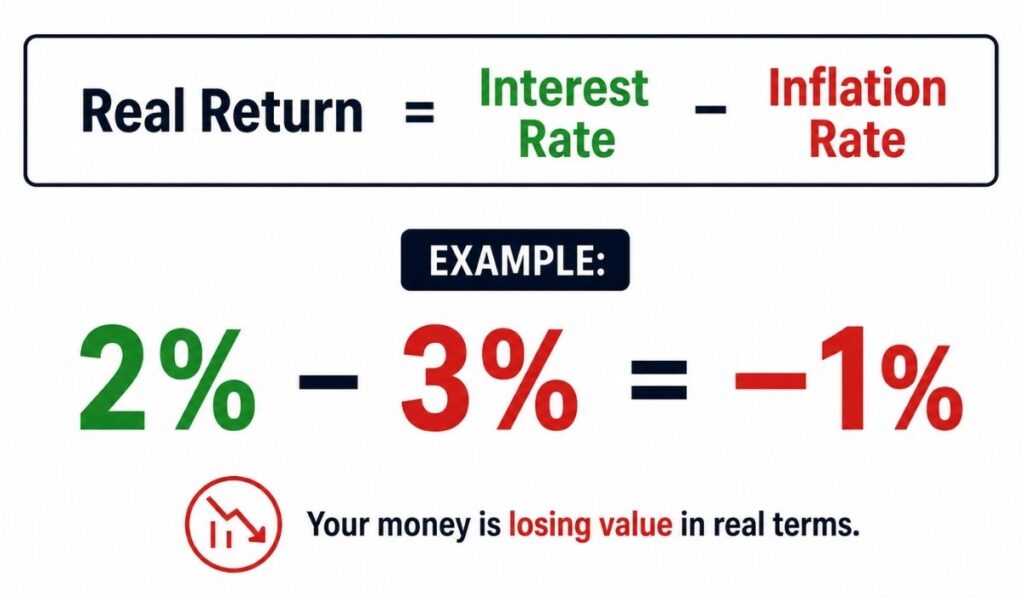

Now here’s the part that changes everything:

Real Return = Interest Rate − Inflation Rate

2% − 3% = −1%

That minus sign? That’s your money losing value.

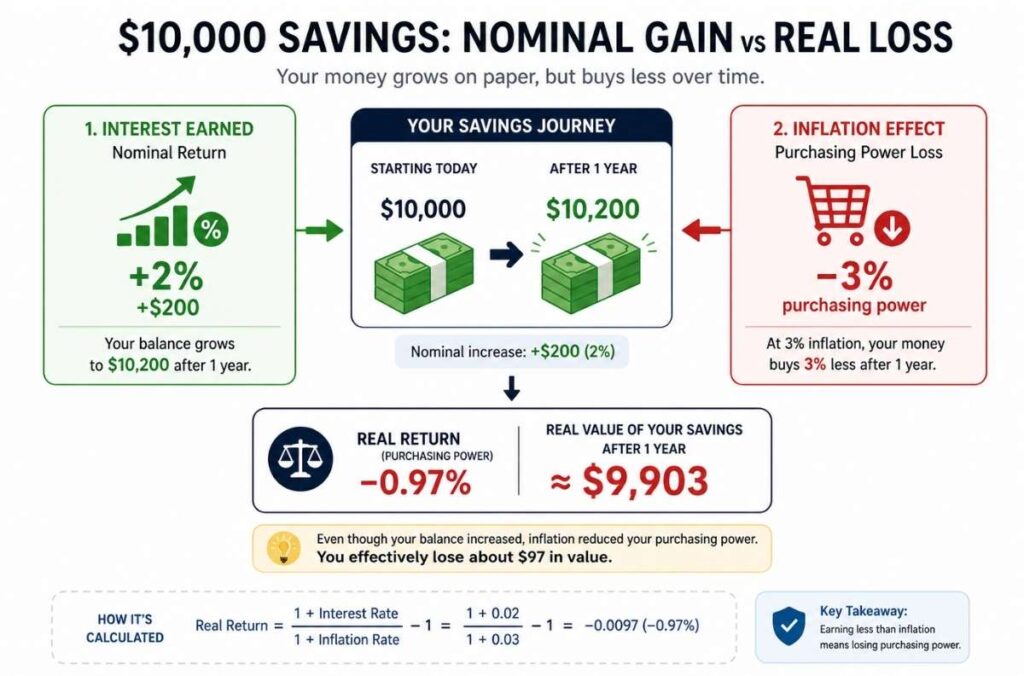

Let’s make it real:

You saved $10,000

You earned $200 in interest

But inflation took $300 in purchasing power

You didn’t gain money. You lost $100.

That’s how wealth slowly disappears without anyone realizing it.

And the worst part?

Your bank still shows a higher balance—so it feels like you’re winning.

Not sure how inflation actually works? We broke it down in plain English in our beginner’s guide: What Is Inflation and Why Does It Make Everything More Expensive?

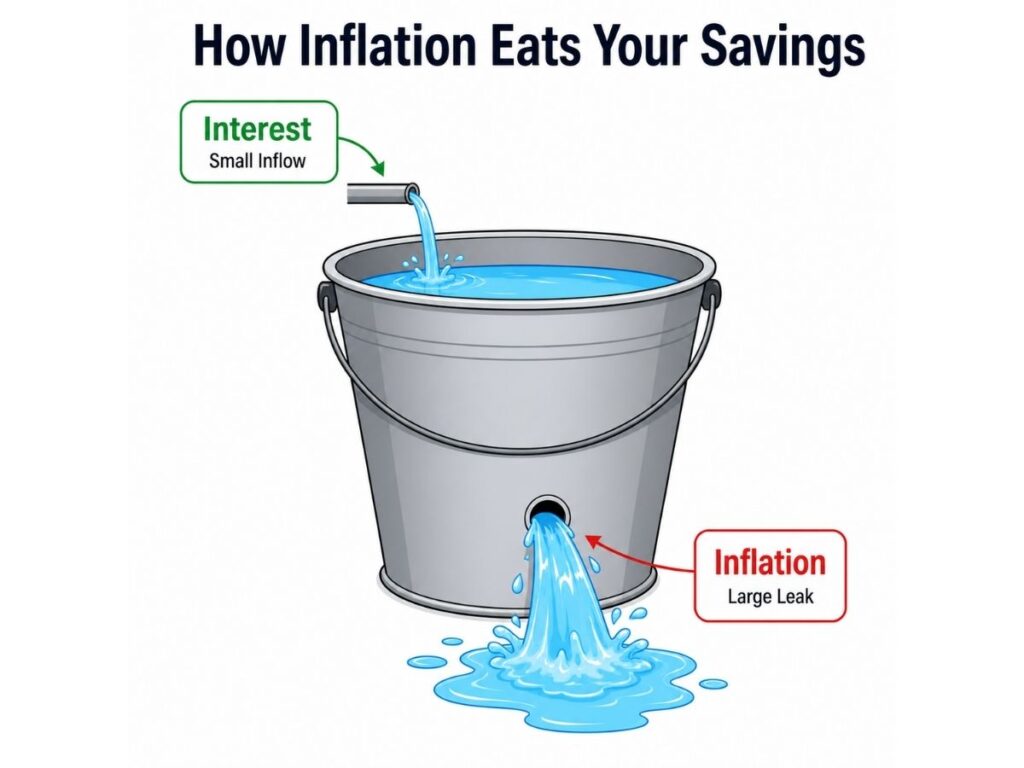

Why This Happens — The One-Minute Explanation

Think of your savings like a bucket of water.

Your bank adds a slow drip from the top.

Inflation is a leak at the bottom.

If the leak is bigger than the drip…

Your bucket empties, no matter how patient you are.

This is where the Time Value of Money comes in:

A dollar today is worth more than a dollar tomorrow.

But when inflation is higher than your interest rate?

Time is no longer helping you—it’s working against you.

A savings account was never designed to grow your wealth.

It was designed to protect your money,not multiply it.

That’s valuable… but only for money you need in the short term. For everything else, a savings account is quietly working against you.

3 Moves to Stop Losing Money Right Now

Here’s the good news:

You don’t need to earn more money to fix this.

You just need to put your money in better places.

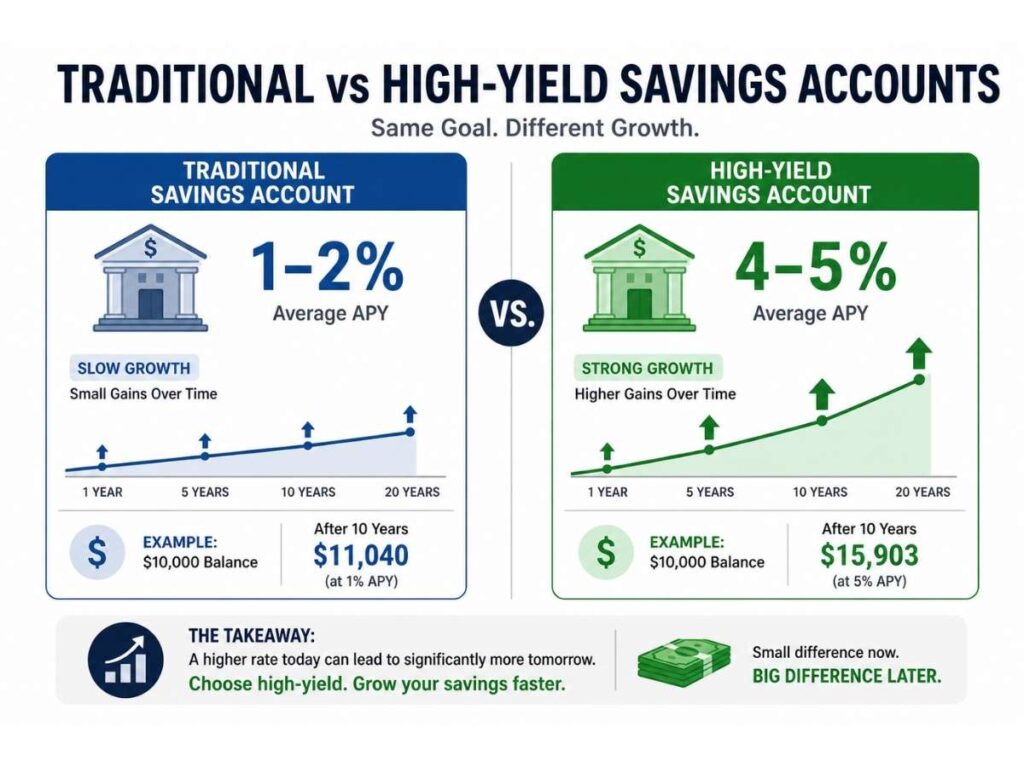

1. Switch to a High-Yield Savings Account (HYSA)

Some online banks are offering 4–5% interest right now—often 2–3x more than traditional banks.

That one move alone can turn your return from negative to positive without taking extra risk.

You can compare current HYSA rates on NerdWallet’s savings rate comparison tool before the end of this week.

2. Look at I-Bonds for Money You Won’t Touch for a Year

I-Bonds are designed specifically for this problem.

Their interest rate adjusts with inflation—so your money keeps up instead of falling behind.

You can buy I-Bonds directly and safely through the U.S. Treasury’s official TreasuryDirect platform. The trade-off is that your money is locked in for a minimum of one year. But for a portion of your savings you don’t need immediately, they’re one of the safest inflation beaters available.

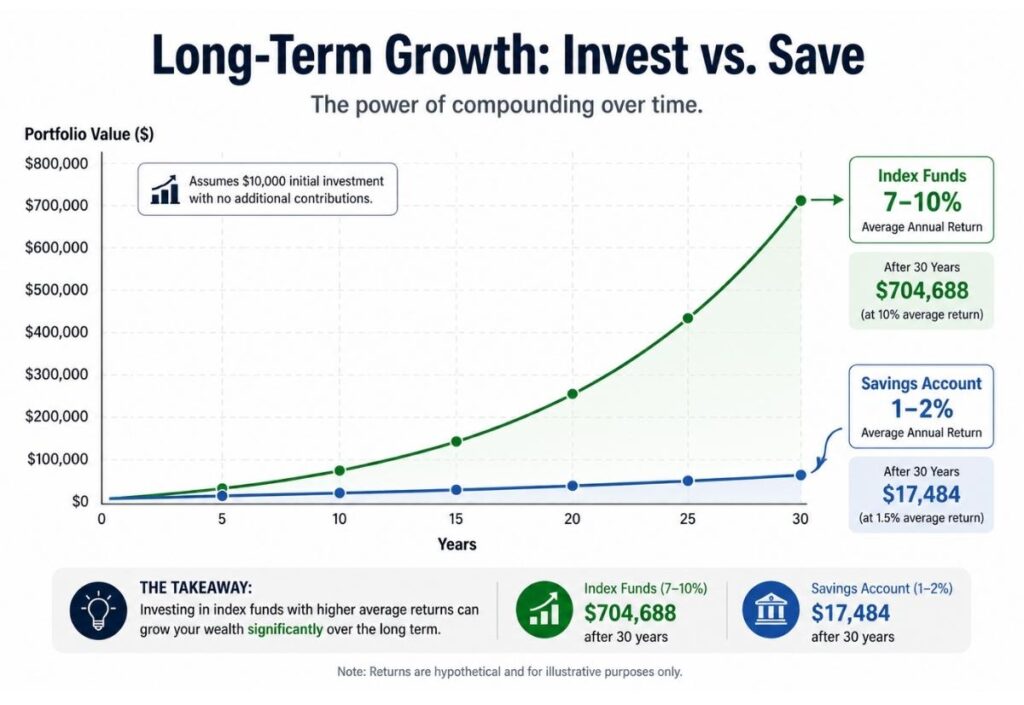

3. Consider Index Funds for Long-Term Money (5+ Years)

Over the long term, index funds have historically returned 7–10% per year.

That’s not just growth—it’s growth that beats inflation.

Short-term, they fluctuate.

Long-term, they’ve consistently outpaced rising prices.

This is where understanding the difference between Stocks and Bonds becomes critical because index funds are built on stocks, and knowing what you own gives you the confidence to stay invested when markets get bumpy.

If you want to understand how your money compounds inside an index fund over time, our post on Compound Interest shows you exactly how the math works with real examples.

If you have money you genuinely won’t need for five or more years, leaving long-term money in a savings account is one of the most expensive financial mistakes you can make.

Your One Action for Today

Do this right now:

Open your savings account.

Find your interest rate.

Then check the current inflation rate.

Subtract one from the other.

If the result is negative…

Your money is losing value every single month.

The difference is:

Now you know it.

And now you can fix it.

Leave a Reply