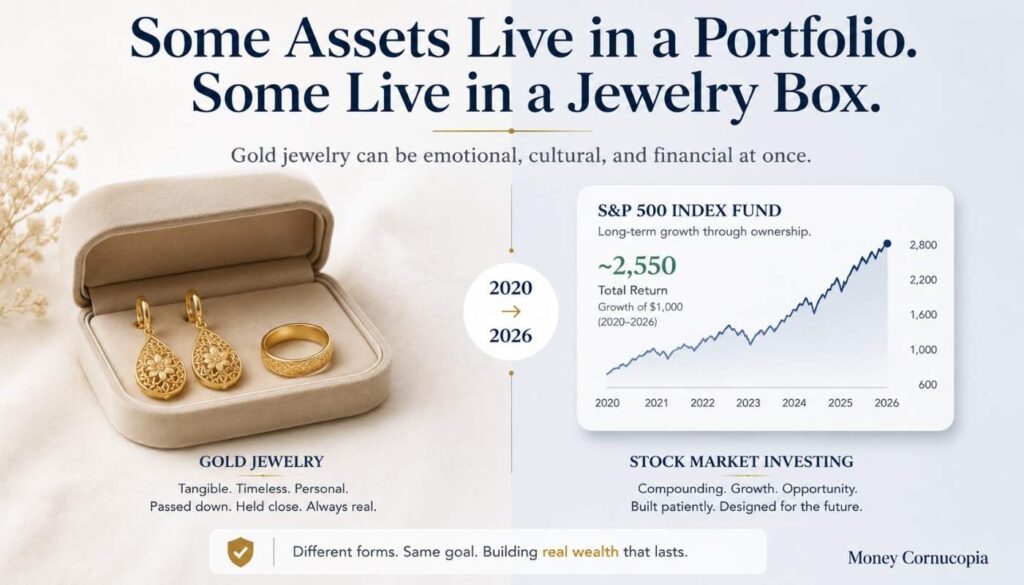

In 2020, I walked into a jewelry shop and bought my wife a pair of gold earrings and a ring. The total came to a little over $1,000.

I was not thinking about portfolio allocation or hedge strategies. I was thinking about two things. First, my wife would love them. Second, my family had always told me that gold is never a bad place to put your money.

Six years later, that $1,000 in gold is worth roughly $2,500.

But here is the part that surprised me. When I ran the numbers on what would have happened if I had put that same $1,000 into the stock market instead, the result was almost identical. Stocks returned nearly the same amount over the same period.

And the savings account? That is where the real story is. The $1,000 I could have left in savings barely grew at all. Once you factor in the inflation that followed 2020, especially the sharp price increases in 2021 and 2022, that money likely buys less today than the original $1,000 bought six years ago.

So I did the full math on all three. Here is what I found.

Table of Contents

The Real Numbers: $1,000 in Gold vs Stocks vs Savings (2020 to 2026)

This is not a hypothetical. These are real returns based on verified market data.

Gold averaged roughly $1,770 per ounce in 2020. As of May 2026, gold is trading at approximately $4,520 per ounce. The S&P 500 started 2020 at roughly 3,258 and sits at approximately 7,470 in May 2026. A standard savings account averaged roughly 2% interest per year over this period.

| Where $1,000 went in 2020 | Approximate value in May 2026 | Total return |

|---|---|---|

| Gold (at 2020 average price) | ~$2,500 to ~$2,550 | ~150% to ~155% |

| S&P 500 (total return with dividends reinvested) | ~$2,550 | ~155% |

| S&P 500 (price return only, no dividends) | ~$2,300 | ~129% |

| Savings account (average 2% interest) | ~$1,125 | ~12.6% |

Read that table carefully. Gold and stocks performed almost identically over this 6-year period. Depending on which exact date you bought and whether you count reinvested dividends, either one could have slightly won. The gap is so small it is essentially a tie.

The massive gap is not between gold and stocks. The massive gap is between investing and not investing.

$1,000 that was invested (in either gold or stocks) became roughly $2,500. $1,000 that was left in a savings account became $1,125. The savings account produced less than one-tenth of the return that gold or stocks produced. And once you factor in the inflation that followed 2020, especially the sharp price increases in 2021 and 2022, that $1,125 likely buys less today than the original $1,000 bought in 2020.

The savings account did not just underperform. It quietly lost purchasing power while looking like it was growing.

That is the finding most people miss.

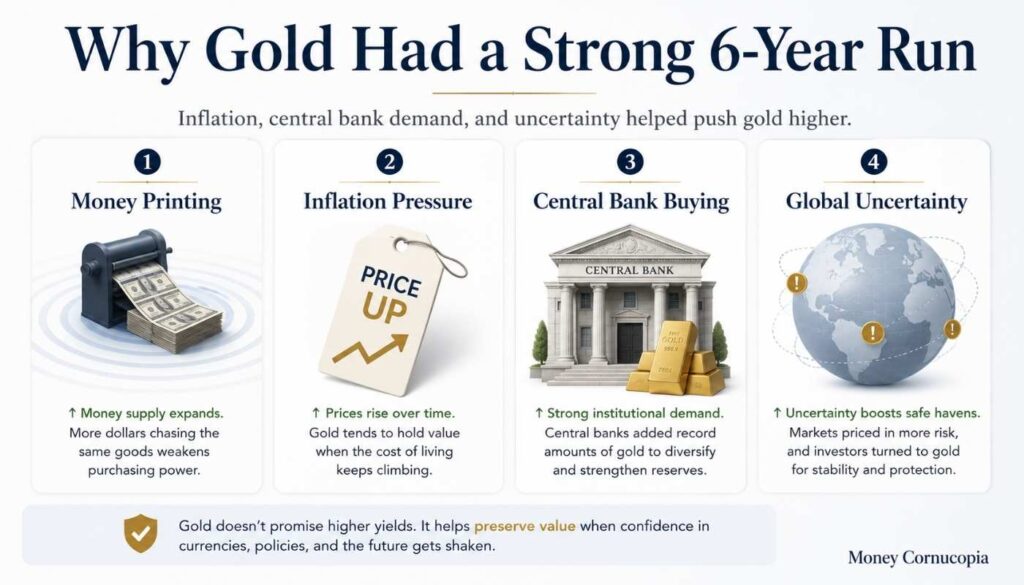

Why Gold Performed So Well From 2020 to 2026

Gold does not always match stocks. But this period was almost perfectly designed for gold to shine.

Several forces aligned at the same time to drive gold prices from roughly $1,770 per ounce in 2020 to over $4,500 per ounce by May 2026.

Massive Money Printing

In 2020, governments around the world printed trillions of dollars to keep economies alive during the pandemic. When more money floods the system, each dollar becomes worth less. Gold, which has a fixed supply that cannot be printed, becomes relatively more valuable. This is the same “melting ice cube” concept I covered in my article on Michael Saylor’s wealth strategy. Cash was melting. Gold was not.

Persistent Inflation

Inflation rose sharply after 2020 and has remained elevated into 2026. When inflation runs higher than the interest rate on your savings account, your cash is quietly losing purchasing power. Gold historically holds value during inflationary periods because its supply cannot be inflated away.

Central Banks Buying Gold at Record Levels

Central banks around the world, particularly in China, Poland, and India, have been buying gold at record levels. According to J.P. Morgan’s gold research, combined central bank and investor demand is expected to average roughly 585 tonnes per quarter in 2026. When the biggest financial institutions in the world are buying, the price tends to rise.

Geopolitical Uncertainty

Wars, trade tensions, and political instability have pushed investors toward safe-haven assets. Gold has been considered a safe haven for centuries, and in times of global uncertainty, demand spikes.

Why Stocks Also Performed Well (And Why They Usually Do)

The S&P 500 returned roughly 129% in price gains and roughly 155% in total return over the same period.

That is a genuinely impressive result. Including reinvested dividends lifts the rough return from about 129% to about 155%, a difference of around 26 percentage points. Over longer periods of 20 to 30 years, stocks have historically returned roughly 7 to 10% per year on average, which tends to outpace gold’s long-term average.

Stocks also have one advantage gold never will: they pay dividends. When you own stocks through an index fund, the companies inside that fund pay you a share of their profits regularly. Over the 2020 to 2026 period, those reinvested dividends were the reason stocks slightly edged ahead of gold in total return.

Gold pays nothing. It just sits there, holding value but not generating cash.

Here is the honest comparison:

| Factor | Gold | Stocks (S&P 500) | Savings account |

|---|---|---|---|

| 2020 to 2026 return | ~150% to ~155% | ~155% (with dividends) | ~12.6% |

| Long term historical average | ~5 to 7% per year | ~7 to 10% per year | ~1 to 3% per year |

| Pays dividends or interest | No | Yes (dividends) | Yes (interest) |

| Protects against inflation | Historically yes | Historically yes (long term) | Often no |

| Volatility | Moderate | High | Very low |

That last row is not entirely a joke. It is genuinely part of why I bought gold as jewelry instead of a gold ETF.

The Honest Downsides of Gold (That Most Articles Will Not Tell You)

Every competing article I read while researching this piece was quietly selling gold. I am not selling anything, so I can be honest about the downsides.

Gold Does Not Generate Income

Stocks pay dividends. Savings accounts pay interest. Bonds pay coupons. Gold just sits there. Over the 2020 to 2026 period, reinvested dividends were the reason stocks slightly edged out gold in total return. If you need your investments to produce cash flow, gold alone will not do that.

Gold Jewelry Has a Hidden Cost

This is important for anyone considering my approach. When you buy gold as jewelry, you pay a “making charge” on top of the gold value. This premium covers the craftsmanship, design, and profit margin for the jeweler. Depending on where you buy, this can add 10 to 25% to the price.

When you sell gold jewelry, you typically get the gold value back, not the making charge. So on day one, your jewelry is worth less than what you paid. Over time, if gold appreciates enough (as it did from 2020 to 2026), the growth more than covers the making charge. But in the short term, you are starting at a small loss.

This is an honest disclosure that most “invest in gold” articles skip because they do not want to discourage you from buying.

Gold Can Drop Sharply

Gold hit an all-time high of roughly $5,600 in January 2026 and then dropped approximately 20% to around $4,500 by May 2026. That is a significant short-term decline. If you had bought at the January peak and needed to sell in May, you would have lost roughly one-fifth of your investment.

Gold is less volatile than stocks on average, but it is not risk-free.

Storage and Security

If you buy physical gold (bars, coins, or jewelry), you need to keep it safe. For jewelry, that usually means wearing it or keeping it in a secure location. For gold bars, you might need a bank safety deposit box or a home safe.

Gold ETFs solve this problem because they are digital, but then you lose the tangible, dual-purpose benefit that jewelry provides.

The Part Nobody Talks About: Why I Bought Gold as Jewelry

Most English-language investing guides treat gold as a ticker symbol. For my family, gold means something different.

I did not buy gold because a YouTube guru told me to. I bought it because my family has always treated gold as a financial tradition. Gifting gold jewelry to your wife is not just an expression of love. It is a way of building family wealth that has worked across generations.

The gold earrings and ring I bought my wife in 2020 serve two purposes that no ETF can match. First, my wife wears them and enjoys them. Second, they have appreciated in value from roughly $1,000 to roughly $2,500.

In many cultures across South Asia, the Middle East, and beyond, gold jewelry is not a “fun accessory.” It is the family’s financial safety net. It is what your grandmother gave your mother. It is the asset your family falls back on in an emergency. It is portable, universally valued, and does not require a bank account or brokerage.

When my family advised me to buy gold, they were not giving me a stock tip. They were sharing generational financial wisdom. The same gold that protected their wealth through economic crises, currency devaluations, and political instability is now protecting mine.

This perspective is almost completely absent from Western financial media. And yet it applies to hundreds of millions of people reading about gold investing in English right now.

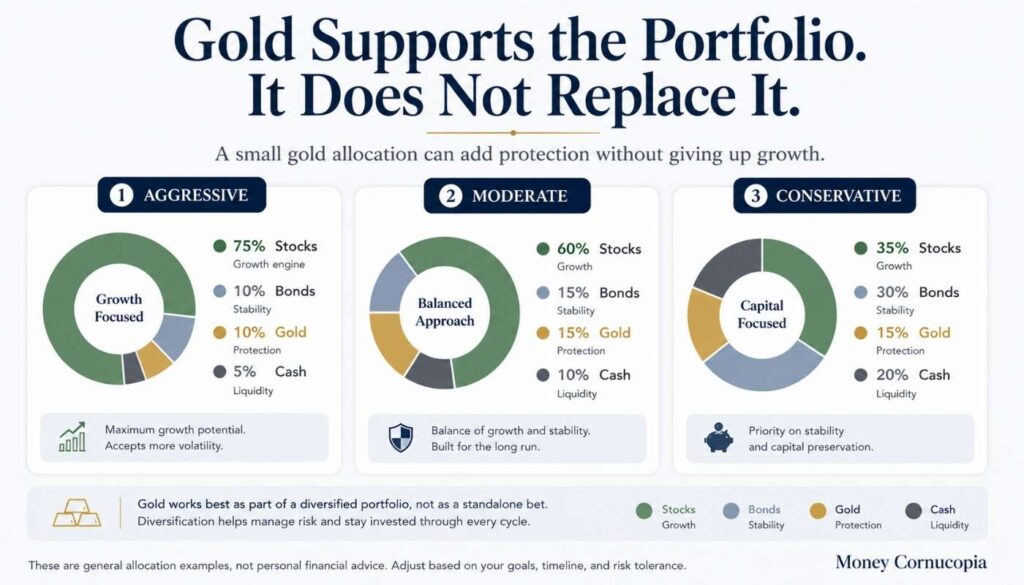

Where Gold Actually Fits in Your Portfolio

Gold is not an entire investment strategy. It is one piece of a larger plan.

In my article on asset allocation and diversification, I explained how spreading your money across different types of investments protects you from any single one failing. Gold is one of those types.

Most financial experts suggest keeping 5 to 15% of your portfolio in gold or precious metals. Not 100%. Not 50%. A slice that provides protection without sacrificing the growth potential of stocks.

Here is a simple framework for a beginner:

| Risk profile | Stocks | Bonds | Gold | Cash |

|---|---|---|---|---|

| Aggressive (20+ year horizon) | 75% | 10% | 10% | 5% |

| Moderate (10 to 20 years) | 60% | 15% | 15% | 10% |

| Conservative (under 10 years) | 35% | 30% | 15% | 20% |

Gold never dominates the portfolio. It supports it. This connects to the risk-return tradeoff that every investor needs to understand. Higher potential returns come with higher risk. Gold sits in the middle, offering moderate returns with moderate volatility.

What I Would Tell a Beginner With $500

If someone asked me, “Should I put my money in gold, stocks, or savings?” here is my honest answer.

Do not put all of it into any one option.

Put $300 into a low-cost stock index fund. This is the growth engine. Over 10 to 20 years, it has the highest expected return and pays dividends along the way. You can start investing with as little as $100.

Put $100 into gold, whatever form makes sense for your situation. Physical gold if you value the tangible asset and the cultural significance. A gold ETF if you want convenience and lower premiums.

Keep $100 in a savings account as an emergency buffer. Not for growth. For peace of mind.

Then keep adding to each category over time. That is asset allocation and diversification in its simplest form.

The 2020 to 2026 data proves the core principle: it barely mattered whether you chose gold or stocks. What mattered was whether you invested at all. The person who put $1,000 into either gold or stocks has roughly $2,500 today. The person who left it in savings has $1,125 and falling purchasing power.

The enemy is not choosing the wrong investment. The enemy is not investing at all.

Different Ways to Invest in Gold

Physical Gold (Jewelry, Coins, Bars)

This is the traditional approach and the one I took. You buy tangible gold that you can hold, wear, or store. The upside is ownership you can see and touch. The downside is the making charge on jewelry and the need for secure storage.

Gold ETFs (Exchange Traded Funds)

A gold ETF tracks the price of gold and trades on the stock market like a stock. You never hold physical gold. The upside is convenience, low fees, and no storage. The downside is that you own a financial product, not a tangible asset.

Gold Coins and Bars (Bullion)

Pure gold in standardized weights. Lower premiums than jewelry (usually 3 to 8% versus 10 to 25% for jewelry). Same storage challenge without the wearable benefit.

Gold Savings Accounts and Digital Gold

Some platforms let you buy gold digitally in small amounts. Easy to start (even $10 at a time). The risk is that you are trusting a company to hold your gold.

Frequently Asked Questions

Is gold a good investment for beginners in 2026?

Gold can be a strong part of a beginner’s portfolio, but it works best alongside stocks, not as a replacement for them. From 2020 to 2026, gold returned roughly 150% to 155%, while the S&P 500 returned roughly 155% with dividends reinvested. Both dramatically outperformed savings accounts. Most experts recommend keeping 5 to 15% of your portfolio in gold.

Did gold beat stocks from 2020 to 2026?

Gold and stocks performed almost identically over this period. Gold returned roughly 150% to 155%, while the S&P 500 returned roughly 129% in price gains and roughly 155% when you include reinvested dividends. The difference is small enough that either one could be called the winner depending on the exact purchase date and method. The real takeaway is that both dramatically outperformed savings accounts.

Is gold jewelry a good investment?

Gold jewelry can be a good investment, but it comes with a making charge (10 to 25% above gold value) that pure gold bars or ETFs do not have. Over time, if gold appreciates significantly, the growth can more than cover this premium. Gold jewelry also has emotional and cultural value that financial products cannot replicate. For many families, it serves as both a wearable asset and a long-term store of wealth.

How much gold should I have in my portfolio?

Most financial experts suggest 5 to 15% of your total portfolio. This provides a meaningful hedge against inflation and market downturns without sacrificing the growth potential of stocks. The exact percentage depends on your risk tolerance, time horizon, and overall goals.

Does gold always beat inflation?

Over long periods, gold has historically kept pace with or outpaced inflation. But there have been shorter periods where gold declined while inflation continued. Gold is a long-term inflation hedge, not a short-term guarantee.

Can I start investing in gold with just $100?

Yes. You can buy a small gold coin, purchase fractional shares of a gold ETF through most brokerage apps, or use digital gold platforms that let you buy in small amounts. In many cultures, families buy small amounts of gold consistently over the years, building a collection gradually.

What happens to gold when interest rates go up?

Higher interest rates generally put downward pressure on gold prices because they make savings accounts and bonds more attractive relative to gold (which pays no interest). However, if inflation remains high even as rates rise, gold can still hold value because its primary appeal is as an inflation hedge. The 2020 to 2026 period showed that gold can perform well even during periods of rising rates if other factors like money printing, central bank buying, and geopolitical tension are strong enough.

Final Thoughts

Six years ago, I bought my wife gold earrings and a ring. It cost me a little over $1,000. That gold is now worth roughly $2,500.

Was gold the best possible investment? Over this specific period, it nearly tied with stocks. Both more than doubled. If I had bought an S&P 500 index fund instead, I would have ended up with roughly the same amount.

But I also would not have seen my wife’s face light up when she opened the box.

The real lesson from this comparison is not “buy gold” or “buy stocks.” The real lesson is that both of them dramatically outperformed the savings account. The $1,000 left in savings barely grew while inflation quietly ate away at its purchasing power.

Long-term cash can become a melting ice cube when inflation stays above the interest you earn. Whether you move it into gold or stocks matters less than whether you move it at all.

Stocks give you growth and dividends. Gold gives you protection and permanence. Savings give you short-term safety. You need all three in the right proportions. But the biggest mistake you can make is leaving everything in the “safe” option and watching it quietly lose value year after year.

That is what the math says. And the math does not care about opinions.

Leave a Reply